Homework Answers

Add Answer to:

Suppose you are asked to analyze a competitive market with identical firms for the government. You...

Suppose you are asked to analyze a competitive market with identical firms for the government. You...

Suppose you are asked to analyze a competitive market with identical firms for the government. You estimate the following: Inverse market demand is: p 100 0.01Q, = The long-run market supply is: p = 10 Each firm's total cost function is: = 500 +0.05q C(q) What is the marginal cost faced by each firm? МС 3 Assuming the industry is in long-run equilibrium, how many firms are currently in this market? (enter your answer rounded to the nearest whole number)...

Suppose you are asked to analyze a competitive market with identical firms for the government. You estimate the following: Inverse market demand is: p 100 0.01Q, = The long-run market supply is: p = 10 Each firm's total cost function is: = 500 +0.05q C(q) What is the marginal cost faced by each firm? МС 3 Assuming the industry is in long-run equilibrium, how many firms are currently in this market? (enter your answer rounded to the nearest whole number)...

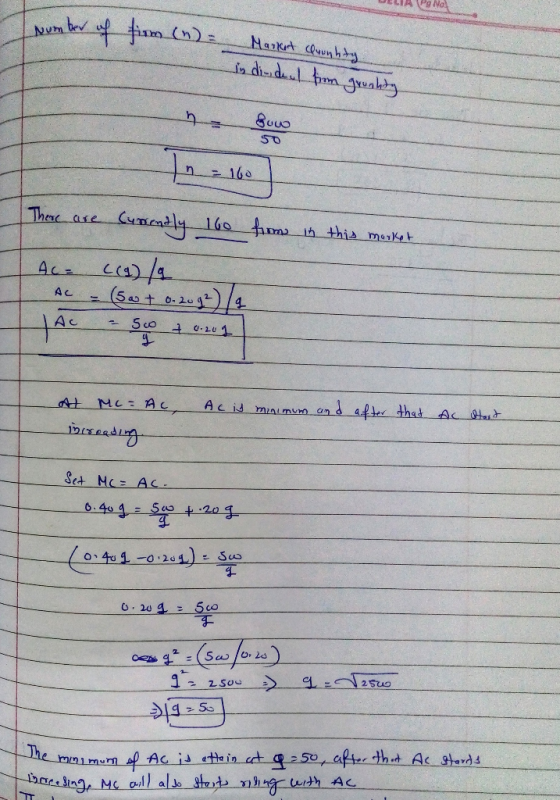

Suppose there is a monopolistically competitive market with n identical firms, such that each firm produces the same quantity, q. Further, the market is in the monopolistically competitive long-run e...

Suppose there is a monopolistically competitive market with n identical firms, such that each firm produces the same quantity, q. Further, the market is in the monopolistically competitive long-run equilibrium. You are given the following: Inverse market demand: P 10-Q Total market output: Qnxq Marginal revenue: MR 10n+ 1)xq Total cost: C(q)-5+q Marginal cost: MC 2xq In long-run equilibrium, each firm earns zero economic profit. In long-run equilibrium, the number of firms, n, is and each firm produces units) of...

Suppose there is a monopolistically competitive market with n identical firms, such that each firm produces the same quantity, q. Further, the market is in the monopolistically competitive long-run equilibrium. You are given the following: Inverse market demand: P 10-Q Total market output: Qnxq Marginal revenue: MR 10n+ 1)xq Total cost: C(q)-5+q Marginal cost: MC 2xq In long-run equilibrium, each firm earns zero economic profit. In long-run equilibrium, the number of firms, n, is and each firm produces units) of...

Consider a perfectly competitive market for titanium. Assume that all firms in the industry are identical and...

Consider a perfectly competitive market for titanium. Assume that all firms in the industry are identical and have the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. Assume also that it does not matter how many firms are in the industry Tool Tip: Place the mouse cursor over orange square points on the MC curve to see coordinates. COST PER UNIT IDollars per pound) 10 MC ATC AVC 0 5...

Consider a perfectly competitive market for titanium. Assume that all firms in the industry are identical and have the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. Assume also that it does not matter how many firms are in the industry Tool Tip: Place the mouse cursor over orange square points on the MC curve to see coordinates. COST PER UNIT IDollars per pound) 10 MC ATC AVC 0 5...

1 poin QUESTION 29 Suppose that a competitive market is initially in equilibrium. Then demand increases....

1 poin QUESTION 29 Suppose that a competitive market is initially in equilibrium. Then demand increases. If entering firms face the same costs as existing firms and sufficient resources are available for entering firms, a in the long run firms will suffer economie losses, leading them to exit the industry. b. the number of firms will decrease, and the market will become a monopoly c. the long run market supply curve will be perfectly elastie. d. the long-run market supply...

1 poin QUESTION 29 Suppose that a competitive market is initially in equilibrium. Then demand increases. If entering firms face the same costs as existing firms and sufficient resources are available for entering firms, a in the long run firms will suffer economie losses, leading them to exit the industry. b. the number of firms will decrease, and the market will become a monopoly c. the long run market supply curve will be perfectly elastie. d. the long-run market supply...

The market for cashews is perfectly competitive and comprised of fifty (50) firms with identical cost...

The market for cashews is perfectly competitive and comprised of fifty (50) firms with identical cost structures and U-shaped ATC curves. The market demand curve for cashews is downward-sloping. The industry is initially in long run equilibrium at the following market price and quantity P* = $4/pound Q* = 50 pounds of cashews In TWO, well-labeled graphs (side by side), depict this long run equilibrium for both the cashew market and for the individual cashew firm. Be sure to calculate...

The market for cashews is perfectly competitive and comprised of fifty (50) firms with identical cost structures and U-shaped ATC curves. The market demand curve for cashews is downward-sloping. The industry is initially in long run equilibrium at the following market price and quantity P* = $4/pound Q* = 50 pounds of cashews In TWO, well-labeled graphs (side by side), depict this long run equilibrium for both the cashew market and for the individual cashew firm. Be sure to calculate...

5 Android Phones - 2 points Suppose the market for Android smart phones is perfectly competitive. All firms are identic...

5 Android Phones - 2 points Suppose the market for Android smart phones is perfectly competitive. All firms are identical with the same cost functions: TC = 9° +800+100, MC = 2q + 80, (q is the quantity produced by a representative firm). The market demand is P = 150 - Q. (Q is market quantity). (a) Given the above information: find the equation for FC, VC, TC, ATC, and AVC. (1/2 point) (b) Determine q, P and the number...

5 Android Phones - 2 points Suppose the market for Android smart phones is perfectly competitive. All firms are identical with the same cost functions: TC = 9° +800+100, MC = 2q + 80, (q is the quantity produced by a representative firm). The market demand is P = 150 - Q. (Q is market quantity). (a) Given the above information: find the equation for FC, VC, TC, ATC, and AVC. (1/2 point) (b) Determine q, P and the number...

Suppose that all existing firms in a long-run competitive market equilibrium are identical and have the...

Suppose that all existing firms in a long-run competitive market equilibrium are identical and have the following cost function C(Q)= 1002 with MC(Q)=2Q. Suppose also that market demand is given by P(Q)=A-0.04Q, where A-40.0. What is the equilibrium market quantity? No units, no rounding. Your Answer: Your Answer

Suppose that all existing firms in a long-run competitive market equilibrium are identical and have the following cost function C(Q)= 1002 with MC(Q)=2Q. Suppose also that market demand is given by P(Q)=A-0.04Q, where A-40.0. What is the equilibrium market quantity? No units, no rounding. Your Answer: Your Answer

What happens in the long run if the government limits entry into a market that was...

What happens in the long run if the government limits entry into a market that was perfectly competitive? The supply curve is flat Cannot be determined from the information The supply curve is upward sloping Firms earn zero profit The supply curve shifts to the right

What happens in the long run if the government limits entry into a market that was perfectly competitive? The supply curve is flat Cannot be determined from the information The supply curve is upward sloping Firms earn zero profit The supply curve shifts to the right

QUESTION 25 Table 14-11 Suppose that a firm in a competitive Price Quantity Total cost Refer...

QUESTION 25 Table 14-11 Suppose that a firm in a competitive Price Quantity Total cost Refer to Table 14-11. The marginal revenue from producing the Sth unit equals (i) $6. (ii) the price. (iii) the marginal cost a. (i) only b.(i) and (ii) only c. (i), (ii), and (iii) d. (iii) only QUESTION 29 Suppose that a competitive market is initially in equilibrium. Then demand increases. If entering firms face the same costs as existing firms and sufficient resources are...

QUESTION 25 Table 14-11 Suppose that a firm in a competitive Price Quantity Total cost Refer to Table 14-11. The marginal revenue from producing the Sth unit equals (i) $6. (ii) the price. (iii) the marginal cost a. (i) only b.(i) and (ii) only c. (i), (ii), and (iii) d. (iii) only QUESTION 29 Suppose that a competitive market is initially in equilibrium. Then demand increases. If entering firms face the same costs as existing firms and sufficient resources are...

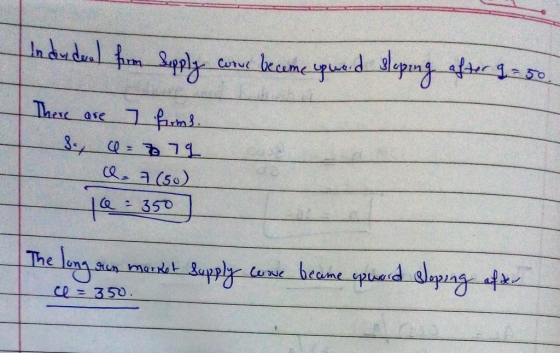

Suppose the market for wheat is perfectly competitive. Suppose further the long-run supply curve in this...

Suppose the market for wheat is perfectly competitive. Suppose further the long-run supply curve in this market is increasing. Explain briefly if and how each of the following varies as market quantity increases: i) The number of firms ii) Input prices iii) Long-run profits Suppose firms in a monopoly competitive market produce their profit-maximizing quantity, and their average total cost equals their marginal revenue. Should firm entry or exit in the long run?

Suppose you are asked to analyze a competitive market with identical firms for the government. You estimate the following: Inverse market demand is: p 100 0.01Q, = The long-run market supply is: p = 10 Each firm's total cost function is: = 500 +0.05q C(q) What is the marginal cost faced by each firm? МС 3 Assuming the industry is in long-run equilibrium, how many firms are currently in this market? (enter your answer rounded to the nearest whole number)...

Suppose you are asked to analyze a competitive market with identical firms for the government. You estimate the following: Inverse market demand is: p 100 0.01Q, = The long-run market supply is: p = 10 Each firm's total cost function is: = 500 +0.05q C(q) What is the marginal cost faced by each firm? МС 3 Assuming the industry is in long-run equilibrium, how many firms are currently in this market? (enter your answer rounded to the nearest whole number)...

Suppose there is a monopolistically competitive market with n identical firms, such that each firm produces the same quantity, q. Further, the market is in the monopolistically competitive long-run equilibrium. You are given the following: Inverse market demand: P 10-Q Total market output: Qnxq Marginal revenue: MR 10n+ 1)xq Total cost: C(q)-5+q Marginal cost: MC 2xq In long-run equilibrium, each firm earns zero economic profit. In long-run equilibrium, the number of firms, n, is and each firm produces units) of...

Suppose there is a monopolistically competitive market with n identical firms, such that each firm produces the same quantity, q. Further, the market is in the monopolistically competitive long-run equilibrium. You are given the following: Inverse market demand: P 10-Q Total market output: Qnxq Marginal revenue: MR 10n+ 1)xq Total cost: C(q)-5+q Marginal cost: MC 2xq In long-run equilibrium, each firm earns zero economic profit. In long-run equilibrium, the number of firms, n, is and each firm produces units) of...

Consider a perfectly competitive market for titanium. Assume that all firms in the industry are identical and have the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. Assume also that it does not matter how many firms are in the industry Tool Tip: Place the mouse cursor over orange square points on the MC curve to see coordinates. COST PER UNIT IDollars per pound) 10 MC ATC AVC 0 5...

Consider a perfectly competitive market for titanium. Assume that all firms in the industry are identical and have the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. Assume also that it does not matter how many firms are in the industry Tool Tip: Place the mouse cursor over orange square points on the MC curve to see coordinates. COST PER UNIT IDollars per pound) 10 MC ATC AVC 0 5...

1 poin QUESTION 29 Suppose that a competitive market is initially in equilibrium. Then demand increases. If entering firms face the same costs as existing firms and sufficient resources are available for entering firms, a in the long run firms will suffer economie losses, leading them to exit the industry. b. the number of firms will decrease, and the market will become a monopoly c. the long run market supply curve will be perfectly elastie. d. the long-run market supply...

1 poin QUESTION 29 Suppose that a competitive market is initially in equilibrium. Then demand increases. If entering firms face the same costs as existing firms and sufficient resources are available for entering firms, a in the long run firms will suffer economie losses, leading them to exit the industry. b. the number of firms will decrease, and the market will become a monopoly c. the long run market supply curve will be perfectly elastie. d. the long-run market supply...

The market for cashews is perfectly competitive and comprised of fifty (50) firms with identical cost structures and U-shaped ATC curves. The market demand curve for cashews is downward-sloping. The industry is initially in long run equilibrium at the following market price and quantity P* = $4/pound Q* = 50 pounds of cashews In TWO, well-labeled graphs (side by side), depict this long run equilibrium for both the cashew market and for the individual cashew firm. Be sure to calculate...

The market for cashews is perfectly competitive and comprised of fifty (50) firms with identical cost structures and U-shaped ATC curves. The market demand curve for cashews is downward-sloping. The industry is initially in long run equilibrium at the following market price and quantity P* = $4/pound Q* = 50 pounds of cashews In TWO, well-labeled graphs (side by side), depict this long run equilibrium for both the cashew market and for the individual cashew firm. Be sure to calculate...

5 Android Phones - 2 points Suppose the market for Android smart phones is perfectly competitive. All firms are identical with the same cost functions: TC = 9° +800+100, MC = 2q + 80, (q is the quantity produced by a representative firm). The market demand is P = 150 - Q. (Q is market quantity). (a) Given the above information: find the equation for FC, VC, TC, ATC, and AVC. (1/2 point) (b) Determine q, P and the number...

5 Android Phones - 2 points Suppose the market for Android smart phones is perfectly competitive. All firms are identical with the same cost functions: TC = 9° +800+100, MC = 2q + 80, (q is the quantity produced by a representative firm). The market demand is P = 150 - Q. (Q is market quantity). (a) Given the above information: find the equation for FC, VC, TC, ATC, and AVC. (1/2 point) (b) Determine q, P and the number...

Suppose that all existing firms in a long-run competitive market equilibrium are identical and have the following cost function C(Q)= 1002 with MC(Q)=2Q. Suppose also that market demand is given by P(Q)=A-0.04Q, where A-40.0. What is the equilibrium market quantity? No units, no rounding. Your Answer: Your Answer

Suppose that all existing firms in a long-run competitive market equilibrium are identical and have the following cost function C(Q)= 1002 with MC(Q)=2Q. Suppose also that market demand is given by P(Q)=A-0.04Q, where A-40.0. What is the equilibrium market quantity? No units, no rounding. Your Answer: Your Answer

What happens in the long run if the government limits entry into a market that was perfectly competitive? The supply curve is flat Cannot be determined from the information The supply curve is upward sloping Firms earn zero profit The supply curve shifts to the right

What happens in the long run if the government limits entry into a market that was perfectly competitive? The supply curve is flat Cannot be determined from the information The supply curve is upward sloping Firms earn zero profit The supply curve shifts to the right

QUESTION 25 Table 14-11 Suppose that a firm in a competitive Price Quantity Total cost Refer to Table 14-11. The marginal revenue from producing the Sth unit equals (i) $6. (ii) the price. (iii) the marginal cost a. (i) only b.(i) and (ii) only c. (i), (ii), and (iii) d. (iii) only QUESTION 29 Suppose that a competitive market is initially in equilibrium. Then demand increases. If entering firms face the same costs as existing firms and sufficient resources are...

QUESTION 25 Table 14-11 Suppose that a firm in a competitive Price Quantity Total cost Refer to Table 14-11. The marginal revenue from producing the Sth unit equals (i) $6. (ii) the price. (iii) the marginal cost a. (i) only b.(i) and (ii) only c. (i), (ii), and (iii) d. (iii) only QUESTION 29 Suppose that a competitive market is initially in equilibrium. Then demand increases. If entering firms face the same costs as existing firms and sufficient resources are...

Most questions answered within 3 hours.

-

Design a class Holiday that represents a

holiday during the year. This class has three

private...

asked 14 minutes ago -

Problem 1 (Logistic Regression and KNN). In this problem, we

predict Direction using the data Weekly.csv....

asked 11 minutes ago -

What is the difference between VNTRs (Variable Number Tandem

Repeats) and STRs (Short Tandem Repeats) used...

asked 18 minutes ago -

Fill in

Isotope: 15 O

1. Element name:

2. Atomic number:

3. Mass number:

4. Number...

asked 18 minutes ago -

These days with the cost of a college education it is important

to be able to...

asked 26 minutes ago -

c++

Implement Radix Sort Most sorting algorithms, like bubble,

insertion, selection and shell follow similar implementations....

asked 33 minutes ago -

Many adult tissues contain terminally differentiated cells that

are incapable of proliferation. How can these tissues...

asked 34 minutes ago -

A survey of tobacco use in high schools tested the saliva of

female and male students...

asked 54 minutes ago -

Assume that the mutation rate for a given gene is

510-6 mutations per gene per generation....

asked 53 minutes ago -

The majority of innovation organizational communication has

been driven by technological advancements in the past thirty...

asked 54 minutes ago -

If one motor has three times as much power as another, then the

smaller power motor:...

asked 52 minutes ago -

Discuss at least four issues that are important to

accountants.

I need 2 pages of explanations

asked 53 minutes ago