Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $349,800 of manufacturing overhead for an estimated allocation base of 1,060 direct labor-hours. The following transactions took place during the year:

Raw materials purchased on account, $230,000.

Raw materials used in production (all direct materials), $215,000.

Utility bills incurred on account, $65,000 (85% related to factory operations, and the remainder related to selling and administrative activities).

Accrued salary and wage costs:

| Direct labor (1,135 hours) | $ | 260,000 |

| Indirect labor | $ | 96,000 |

| Selling and administrative salaries | $ | 140,000 |

Maintenance costs incurred on account in the factory, $60,000

Advertising costs incurred on account, $142,000.

Depreciation was recorded for the year, $90,000 (75% related to factory equipment, and the remainder related to selling and administrative equipment).

Rental cost incurred on account, $115,000 (80% related to factory facilities, and the remainder related to selling and administrative facilities).

Manufacturing overhead cost was applied to jobs, $ ? .

Cost of goods manufactured for the year, $830,000.

Sales for the year (all on account) totaled $1,500,000. These goods cost $860,000 according to their job cost sheets.

The balances in the inventory accounts at the beginning of the year were:

| Raw Materials | $ | 36,000 |

| Work in Process | $ | 27,000 |

| Finished Goods | $ | 66,000 |

Required:

1. Prepare journal entries to record the preceding transactions.

2. Post your entries to T-accounts. (Don’t forget to enter the beginning inventory balances above.)

3. Prepare a schedule of cost of goods manufactured.

4A. Prepare a journal entry to close any balance in the Manufacturing Overhead account to Cost of Goods Sold.

4B. Prepare a schedule of cost of goods sold.

5. Prepare an income statement for the year.

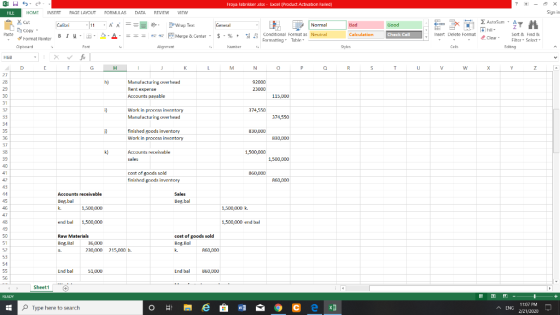

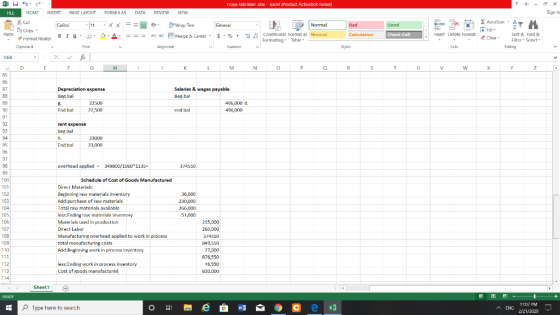

Froya Fabrikker A/S Schedule of Cost of Goods Manufactured Direct materials: Total raw materials available Materials used in production Total manufacturing costs Cost of goods manufactured

Homework Answers

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $336,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The following transactions took place during the year:

Raw materials purchased on account, $245,000.

Raw materials used in production (all direct materials), $230,000.

Utility bills incurred on account, $68,000 (85% related to factory operations, and the remainder related to selling and administrative activities).

Accrued salary and wage costs:

| Direct labor (1,125 hours) | $ | 275,000 |

| Indirect labor | $ | 99,000 |

| Selling and administrative salaries | $ | 155,000 |

Maintenance costs incurred on account in the factory, $63,000

Advertising costs incurred on account, $145,000.

Depreciation was recorded for the year, $81,000 (70% related to factory equipment, and the remainder related to selling and administrative equipment).

Rental cost incurred on account, $106,000 (75% related to factory facilities, and the remainder related to selling and administrative facilities).

Manufacturing overhead cost was applied to jobs, $ ? .

Cost of goods manufactured for the year, $860,000.

Sales for the year (all on account) totaled $1,650,000. These goods cost $890,000 according to their job cost sheets.

The balances in the inventory accounts at the beginning of the year were:

| Raw Materials | $ | 39,000 |

| Work in Process | $ | 30,000 |

| Finished Goods | $ | 69,000 |

Required:

1. Prepare journal entries to record the preceding transactions.

2. Post your entries to T-accounts. (Don’t forget to enter the beginning inventory balances above.)

3. Prepare a schedule of cost of goods manufactured.

4A. Prepare a journal entry to close any balance in the Manufacturing Overhead account to Cost of Goods Sold.

4B. Prepare a schedule of cost of goods sold.

5. Prepare an income statement for the year.

Add Answer to:

Froya Fabrikker A/S of Bergen, Norway, is a small company thatmanufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil Telds. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing overhead for an estimated allocation base of 1,000 direct labor-hours. The following transactions took place during the year a Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil Telds. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing overhead for an estimated allocation base of 1,000 direct labor-hours. The following transactions took place during the year a Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $349,800 of manufacturing overhead for an

estimated allocation base of 1,060 direct labor-hours. The

following transactions took place during the year:

Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $349,800 of manufacturing overhead for an

estimated allocation base of 1,060 direct labor-hours. The

following transactions took place during the year:

Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $350,000 of manufacturing overhead for an

estimated allocation base of 1,000 direct labor-hours. The

following transactions took place during the year:

Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $350,000 of manufacturing overhead for an

estimated allocation base of 1,000 direct labor-hours. The

following transactions took place during the year:

Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing overhead for an estimated allocation base of 1,000 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $399,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The following transactions took place during the year a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The following transactions took place during the year a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $372,000 of manufacturing overhead for an estimated allocation base of 1,200 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $380,000 of manufacturing overhead for an estimated allocation base of 1,000 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $372,000 of manufacturing overhead for an estimated allocation base of 1,200 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $374,000 of manufacturing overhead for an estimated allocation base of 1,100 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil Telds. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing overhead for an estimated allocation base of 1,000 direct labor-hours. The following transactions took place during the year a Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil Telds. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing overhead for an estimated allocation base of 1,000 direct labor-hours. The following transactions took place during the year a Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $349,800 of manufacturing overhead for an

estimated allocation base of 1,060 direct labor-hours. The

following transactions took place during the year:

Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $349,800 of manufacturing overhead for an

estimated allocation base of 1,060 direct labor-hours. The

following transactions took place during the year:

Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $350,000 of manufacturing overhead for an

estimated allocation base of 1,000 direct labor-hours. The

following transactions took place during the year:

Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $350,000 of manufacturing overhead for an

estimated allocation base of 1,000 direct labor-hours. The

following transactions took place during the year:

Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The following transactions took place during the year a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The following transactions took place during the year a. Raw materials purchased...

Most questions answered within 3 hours.

-

Two particles each have a rest mass energy of 30 MeV and are

traveling with a...

asked 25 minutes ago -

why

is vectorization a faster alternative to loops?

asked 1 hour ago -

General Matter’s outstanding bond issue has a coupon rate of

11.8%, and it sells at a...

asked 1 hour ago -

Write a one page essay on how important is it to know your basic

accounting knowledge...

asked 1 hour ago -

You are a Senior Civil Engineer posted at the Contracts and

Procurement Division of the Ministry...

asked 1 hour ago -

When using the percentage of completion method, the

company

- recognizes revenues and gross profit each...

asked 1 hour ago -

Is a level production strategy suitable for a pure service

industry, such as professional accounting and...

asked 1 hour ago -

Baker Industries’ net income is $23000, its interest expense is

$4000, and its tax rate is...

asked 2 hours ago -

a) A proton moves at 500 m/s in a 2 T magnetic field. What is

the...

asked 2 hours ago -

Anderson Systems is considering a project that has the following

cash flow and WACC data. What...

asked 2 hours ago -

MARIE Assembly Code Problem

For the following problem, please create new MARIE instructions

by providing the...

asked 2 hours ago -

Which ligands are similar to each other in how they bind to

metals?

A) methyl, amine,...

asked 2 hours ago