Capital Rationing Decision for a Service Company Involving Four Proposals Renaissance Capital Group is considering allocating...

Capital Rationing Decision for a Service Company Involving Four Proposals

Renaissance Capital Group is considering allocating a limited amount of capital investment funds among four proposals. The amount of proposed investment, estimated income from operations, and net cash flow for each proposal are as follows:

| Investment | Year | Income from Operations | Net Cash Flow | |||

| Proposal A: | $680,000 | 1 | $ 64,000 | $ 200,000 | ||

| 2 | 64,000 | 200,000 | ||||

| 3 | 64,000 | 200,000 | ||||

| 4 | 24,000 | 160,000 | ||||

| 5 | 24,000 | 160,000 | ||||

| $240,000 | $ 920,000 | |||||

| Proposal B: | $320,000 | 1 | $ 26,000 | $ 90,000 | ||

| 2 | 26,000 | 90,000 | ||||

| 3 | 6,000 | 70,000 | ||||

| 4 | 6,000 | 70,000 | ||||

| 5 | (44,000) | 20,000 | ||||

| $ 20,000 | $340,000 | |||||

| Proposal C: | $108,000 | 1 | $ 33,400 | $ 55,000 | ||

| 2 | 31,400 | 53,000 | ||||

| 3 | 28,400 | 50,000 | ||||

| 4 | 25,400 | 47,000 | ||||

| 5 | 23,400 | 45,000 | ||||

| $142,000 | $ 250,000 | |||||

| Proposal D: | $400,000 | 1 | $100,000 | $ 180,000 | ||

| 2 | 100,000 | 180,000 | ||||

| 3 | 80,000 | 160,000 | ||||

| 4 | 20,000 | 100,000 | ||||

| 5 | 0 | 80,000 | ||||

| $300,000 | $700,000 |

The company's capital rationing policy requires a maximum cash payback period of three years. In addition, a minimum average rate of return of 12% is required on all projects. If the preceding standards are met, the net present value method and present value indexes are used to rank the remaining proposals.

| Present Value of $1 at Compound Interest | |||||

| Year | 6% | 10% | 12% | 15% | 20% |

| 1 | 0.943 | 0.909 | 0.893 | 0.870 | 0.833 |

| 2 | 0.890 | 0.826 | 0.797 | 0.756 | 0.694 |

| 3 | 0.840 | 0.751 | 0.712 | 0.658 | 0.579 |

| 4 | 0.792 | 0.683 | 0.636 | 0.572 | 0.482 |

| 5 | 0.747 | 0.621 | 0.567 | 0.497 | 0.402 |

| 6 | 0.705 | 0.564 | 0.507 | 0.432 | 0.335 |

| 7 | 0.665 | 0.513 | 0.452 | 0.376 | 0.279 |

| 8 | 0.627 | 0.467 | 0.404 | 0.327 | 0.233 |

| 9 | 0.592 | 0.424 | 0.361 | 0.284 | 0.194 |

| 10 | 0.558 | 0.386 | 0.322 | 0.247 | 0.162 |

Required:

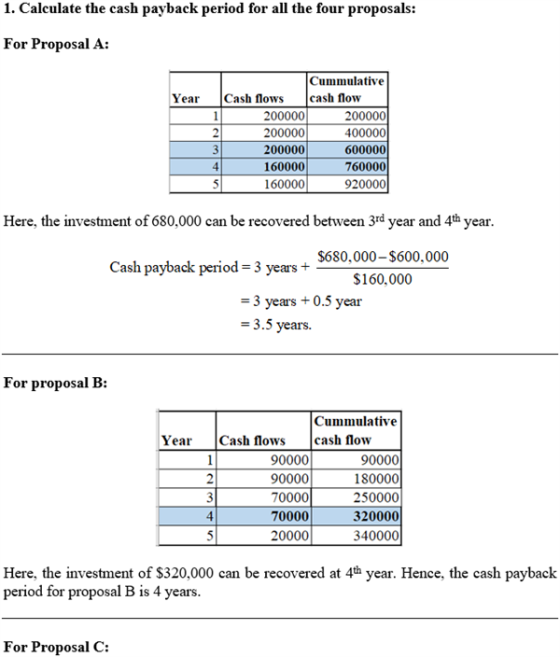

1. Compute the cash payback period for each of the four proposals.

| Cash Payback Period | |

| Proposal A | 3 years 6 months |

| Proposal B | 4 years |

| Proposal C | 2 years |

| Proposal D | 2 years 3 months |

2. Giving effect to straight-line depreciation on the investments and assuming no estimated residual value, compute the average rate of return for each of the four proposals. If required, round your answers to one decimal place.

| Average Rate of Return | |

| Proposal A | % |

| Proposal B | % |

| Proposal C | % |

| Proposal D | % |

3. Using the following format, summarize the results of your computations in parts (1) and (2) by placing the calculated amounts in the first two columns on the left and indicate which proposals should be accepted for further analysis and which should be rejected. If required, round your answers to one decimal place.

| Proposal | Cash Payback Period | Average Rate of Return | Accept or Reject | |

| A | 3 years, 6 months | % | Reject | |

| B | 4 years | % | Reject | |

| C | 2 years | % | Accept | |

| D | 2 years, 3 months | % | Accept | |

4. For the proposals accepted for further analysis in part (3), compute the net present value. Use a rate of 15% and the present value of $1 table above. Round to the nearest dollar.

| Select the proposal accepted for further analysis. | Proposal C | Proposal D |

| Present value of net cash flow total | $ | $ |

| Less amount to be invested | $ | $ |

| Net present value | $ | $ |

5. Compute the present value index for each of the proposals in part (4). If required, round your answers to two decimal places.

| Select proposal to compute Present value index. | Proposal C | Proposal D |

| Present value index (rounded) |

6. Rank the proposals from most attractive to least attractive, based on the present values of net cash flows computed in part (4).

| Rank 1st | Proposal D |

| Rank 2nd | Proposal C |

7. Rank the proposals from most attractive to least attractive, based on the present value indexes computed in part (5).

| Rank 1st | Proposal C |

| Rank 2nd | Proposal D |

8. The present value indexes indicate that although Proposal D has the larger net present value, it is not as attractive as Proposal C in terms of the amount of present value per dollar invested. Proposal D requires the larger investment. Thus, management should use investment resources for Proposal C before investing in Proposal D , absent any other qualitative considerations that may impact the decision.

Homework Answers

Add Answer to:

Capital Rationing Decision for a Service Company Involving Four

Proposals

Renaissance Capital Group is considering allocating...

Capital Rationing Decision for a Service Company Involving Four Proposals Renaissance Capital Group is considering allocating...

Capital Rationing Decision for a Service Company Involving Four Proposals Renaissance Capital Group is considering allocating a limited amount of capital investment funds among four proposals. The amount of proposed investment, estimated operating income, and net cash flow for each proposal are as follows: Investment Year Operating Income Net Cash Flow Proposal A: $680,000 1 $ 64,000 $ 200,000 2 64,000 200,000 3 64,000 200,000 4 24,000 160,000 5 24,000 160,000 $240,000 $ 920,000 Proposal B: $320,000 1 $ 26,000...

Capital Rationing Decision for a Service Company Involving Four Proposals Renaissance Capital Group is considering allocating...

Capital Rationing Decision for a Service Company Involving Four Proposals Renaissance Capital Group is considering allocating a limited amount of capital investment funds among four proposals. The amount of proposed investment, estimated income from operations, and net cash flow for each proposal are as follows: Investment Year Income from Operations Net Cash Flow Proposal A: $680,000 1 $ 64,000 $ 200,000 2 64,000 200,000 3 64,000 200,000 4 24,000 160,000 5 24,000 160,000 $240,000 $ 920,000 Proposal B: $320,000 1...

Capital Rationing Decision for a Service Company Involving Four Proposals Renaissance Capital Group is considering alloc...

Capital Rationing Decision for a Service Company Involving Four Proposals Renaissance Capital Group is considering allocating a limited amount of capital investment funds among four proposals. The amount of proposed investment, estimated operating income, and net cash flow for each proposal are as follows: Investment Year Operating Income Net Cash Flow Proposal A: $680,000 1 $ 64,000 $ 200,000 2 64,000 200,000 3 64,000 200,000 4 24,000 160,000 5 24,000 160,000 $240,000 $ 920,000 Proposal B: $320,000 1 $ 26,000...

Capital Rationing Decision for a Service Company Involving Four Proposals Renaissance Capital Gro...

Capital Rationing Decision for a Service Company Involving Four Proposals Renaissance Capital Group is considering allocating a limited amount of capital investment funds among four proposals. The amount of proposed investment, estimated income from operations, and net cash flow for each proposal are as follows: Investment Year Income from Operations Net Cash Flow Proposal A: $680,000 1 $ 64,000 $ 200,000 2 64,000 200,000 3 64,000 200,000 4 24,000 160,000 5 24,000 160,000 $240,000 $ 920,000 Proposal B: $320,000 1...

Capital Rationing Decision for a Service Company Involving Four Proposals Clearcast Communications Inc. is considering allocating...

Capital Rationing Decision for a Service Company Involving Four Proposals Clearcast Communications Inc. is considering allocating a limited amount of capital investment funds among four proposals. The amount of proposed investment, estimated Operating income, and net cash flow for each proposal are as follows: Investment Year Operating Income Net Cash Flow Proposal A: $450,000 1 $30,000 $120,000 2 30,000 120,000 3 20,000 110,000 4 10,000 100,000 5 (30,000) 60,000 $60,000 $510,000 Proposal B: $200,000 1 $60,000 $100,000 2 40,000 80,000...

-NM PR 11-6B Capital rationing decision for a service company involving Obj. 2, 3,5 four proposals...

-NM PR 11-6B Capital rationing decision for a service company involving Obj. 2, 3,5 four proposals Clearcast Communications Inc. is considering allocating a limited amount of capital investment funds among four proposals. The amount of proposed investment, estimated income from operations, and net cash flow for each proposal are as follows: Income from Net Cash Investment Year Operations Flow Proposal A: $450,000 $ 30,000 $120,000 30,000 120,000 20,000 110,000 10,000 100,000 (30,000) 60,000 $ 60,000 $510,000 Proposal B: $200,000 $...

-NM PR 11-6B Capital rationing decision for a service company involving Obj. 2, 3,5 four proposals Clearcast Communications Inc. is considering allocating a limited amount of capital investment funds among four proposals. The amount of proposed investment, estimated income from operations, and net cash flow for each proposal are as follows: Income from Net Cash Investment Year Operations Flow Proposal A: $450,000 $ 30,000 $120,000 30,000 120,000 20,000 110,000 10,000 100,000 (30,000) 60,000 $ 60,000 $510,000 Proposal B: $200,000 $...

Renaissance Capital Group is considering allocating a limited amount of capital investment funds among four proposals....

Renaissance Capital Group is considering allocating a limited amount of capital investment funds among four proposals. The amount of proposed investment, estimated operating income, and net cash flow for each proposal are as follows: Investment Year Operating Income Net Cash Flow Proposal A: $680,000 1 $ 64,000 $ 200,000 2 64,000 200,000 3 64,000 200,000 4 24,000 160,000 5 24,000 160,000 $240,000 $ 920,000 Proposal B: $320,000 1 $ 26,000 $ 90,000 2 26,000 90,000 3 6,000 70,000 4 6,000...

Information on four investment proposals is given below: Investment required Present value of cash inflows Investment...

Information on four investment proposals is given below: Investment required Present value of cash inflows Investment Proposal A B C D $ (720,000) $ (160,000) $(130,000) $(1,560,000) 1,013,000 221,800 198,900 2,081,400 $ 293,000 $ 61,800 $ 68,900 $ 521,400 5 years 7 years 6 years 6 years Net present value Life of the project Required: 1. Compute the project profitability index for each investment proposal. (Round your answers to 2 decimal places.) 2. Rank the proposals in terms of preference....

Information on four investment proposals is given below: Investment required Present value of cash inflows Investment Proposal A B C D $ (720,000) $ (160,000) $(130,000) $(1,560,000) 1,013,000 221,800 198,900 2,081,400 $ 293,000 $ 61,800 $ 68,900 $ 521,400 5 years 7 years 6 years 6 years Net present value Life of the project Required: 1. Compute the project profitability index for each investment proposal. (Round your answers to 2 decimal places.) 2. Rank the proposals in terms of preference....

Information on four investment proposals is given below: Investment required Present value of cash inflows Investment...

Information on four investment proposals is given below: Investment required Present value of cash inflows Investment Proposal Α D $(90,000) $ (100,000) $ ( 70,000) $ (120,000) 126,000 138,000 105,000 160,000 $ 36,000 $ 38,000 $ 35,000 $ 40,000 5 years 7 years 6 years 6 years Net present value Life of the project Required: 1. Compute the project profitability index for each investment proposal. (Round your answers to 2 decimal places.) 2. Rank the proposals in terms of preference....

Information on four investment proposals is given below: Investment required Present value of cash inflows Investment Proposal Α D $(90,000) $ (100,000) $ ( 70,000) $ (120,000) 126,000 138,000 105,000 160,000 $ 36,000 $ 38,000 $ 35,000 $ 40,000 5 years 7 years 6 years 6 years Net present value Life of the project Required: 1. Compute the project profitability index for each investment proposal. (Round your answers to 2 decimal places.) 2. Rank the proposals in terms of preference....

Exercise 12-5 Preference Ranking [LO12-5] Information on four investment proposals is given below: Investment Proposal A...

Exercise 12-5 Preference Ranking [LO12-5] Information on four investment proposals is given below: Investment Proposal A B C D Investment required $ (720,000 ) $ (160,000 ) $ (130,000 ) $ (1,560,000 ) Present value of cash inflows 1,013,000 221,800 198,900 2,081,400 Net present value $ 293,000 $ 61,800 $ 68,900 $ 521,400 Life of the project 5 years 7 years 6 years 6 years Required: 1. Compute the project profitability index for each investment proposal. (Round your answers to...

-NM PR 11-6B Capital rationing decision for a service company involving Obj. 2, 3,5 four proposals Clearcast Communications Inc. is considering allocating a limited amount of capital investment funds among four proposals. The amount of proposed investment, estimated income from operations, and net cash flow for each proposal are as follows: Income from Net Cash Investment Year Operations Flow Proposal A: $450,000 $ 30,000 $120,000 30,000 120,000 20,000 110,000 10,000 100,000 (30,000) 60,000 $ 60,000 $510,000 Proposal B: $200,000 $...

-NM PR 11-6B Capital rationing decision for a service company involving Obj. 2, 3,5 four proposals Clearcast Communications Inc. is considering allocating a limited amount of capital investment funds among four proposals. The amount of proposed investment, estimated income from operations, and net cash flow for each proposal are as follows: Income from Net Cash Investment Year Operations Flow Proposal A: $450,000 $ 30,000 $120,000 30,000 120,000 20,000 110,000 10,000 100,000 (30,000) 60,000 $ 60,000 $510,000 Proposal B: $200,000 $...

Information on four investment proposals is given below: Investment required Present value of cash inflows Investment Proposal A B C D $ (720,000) $ (160,000) $(130,000) $(1,560,000) 1,013,000 221,800 198,900 2,081,400 $ 293,000 $ 61,800 $ 68,900 $ 521,400 5 years 7 years 6 years 6 years Net present value Life of the project Required: 1. Compute the project profitability index for each investment proposal. (Round your answers to 2 decimal places.) 2. Rank the proposals in terms of preference....

Information on four investment proposals is given below: Investment required Present value of cash inflows Investment Proposal A B C D $ (720,000) $ (160,000) $(130,000) $(1,560,000) 1,013,000 221,800 198,900 2,081,400 $ 293,000 $ 61,800 $ 68,900 $ 521,400 5 years 7 years 6 years 6 years Net present value Life of the project Required: 1. Compute the project profitability index for each investment proposal. (Round your answers to 2 decimal places.) 2. Rank the proposals in terms of preference....

Information on four investment proposals is given below: Investment required Present value of cash inflows Investment Proposal Α D $(90,000) $ (100,000) $ ( 70,000) $ (120,000) 126,000 138,000 105,000 160,000 $ 36,000 $ 38,000 $ 35,000 $ 40,000 5 years 7 years 6 years 6 years Net present value Life of the project Required: 1. Compute the project profitability index for each investment proposal. (Round your answers to 2 decimal places.) 2. Rank the proposals in terms of preference....

Information on four investment proposals is given below: Investment required Present value of cash inflows Investment Proposal Α D $(90,000) $ (100,000) $ ( 70,000) $ (120,000) 126,000 138,000 105,000 160,000 $ 36,000 $ 38,000 $ 35,000 $ 40,000 5 years 7 years 6 years 6 years Net present value Life of the project Required: 1. Compute the project profitability index for each investment proposal. (Round your answers to 2 decimal places.) 2. Rank the proposals in terms of preference....

Most questions answered within 3 hours.

-

Cruz Video Center accumulates the following cost and net

realizable data at December 31.

Cameras $14,700...

asked 1 minute from now -

Direct Labor Variances

The following data relate to labor cost for production of 4,600

cellular telephones:...

asked 3 minutes ago -

1. Describe the differences between management in the nonprofit

sector and management in other sectors. How...

asked 4 minutes ago -

Identify the location of the following corresponding operand if

the address field in an instruction contains...

asked 6 minutes ago -

A new battery's voltage may be acceptable (A) or unacceptable

(U). A certain flashlight requires two...

asked 8 minutes ago -

Water has significant IMF, which result in many of its unique

properties—high boiling point relative to...

asked 27 minutes ago -

I need help with an executive summary for Adidas Items to be

included are a discription...

asked 20 minutes ago -

19. Most progressive reform activists were white

and a. upper class. b. lower class. c. wokring...

asked 23 minutes ago -

If X is a binomial random variable with n = 8

and p = 0.2, the...

asked 33 minutes ago -

Seasonal or cyclical variation in a time-series model…

---exhibits irregular

variation that can be accounted for...

asked 34 minutes ago -

Please use Barney's VRIO framework of analysis to evaluate a

firm's competencies. Please choose a specific...

asked 47 minutes ago -

Where would you expect to have diabetes contributing to the most

DALYs in 2035, according to...

asked 48 minutes ago