Homework Answers

![= 673 X 200 19 = 366.82] AC = 673 t 9 20 AC= 3.66 Hence Price in the long nen wiu be 3.66 There is zero profit at this capric](http://img.homeworklib.com/questions/b0ada400-2403-11eb-8eed-0f9e8db5dbcb.png?x-oss-process=image/resize,w_560)

Add Answer to:

Suppose you are given the following information about a particular industry: Market demand Market supply QD...

4. The supply and demand in a given industry is defined by QD – 6500 –...

4. The supply and demand in a given industry is defined by QD – 6500 – 100P and QS – 1200P respectively. In this industry, the cost function of an efficient firm is C(q) = 722 + 2/200. You can assume that all firms in the industry are efficient and identical) and the industry is operating under perfect competition. (a) Find the market equilibrium (prices and quantities) (b) Determine how much will each firm produce, and the profits for each...

4. The supply and demand in a given industry is defined by QD – 6500 – 100P and QS – 1200P respectively. In this industry, the cost function of an efficient firm is C(q) = 722 + 2/200. You can assume that all firms in the industry are efficient and identical) and the industry is operating under perfect competition. (a) Find the market equilibrium (prices and quantities) (b) Determine how much will each firm produce, and the profits for each...

Suppose you are given the following information about a particular industry in the short run (perfect...

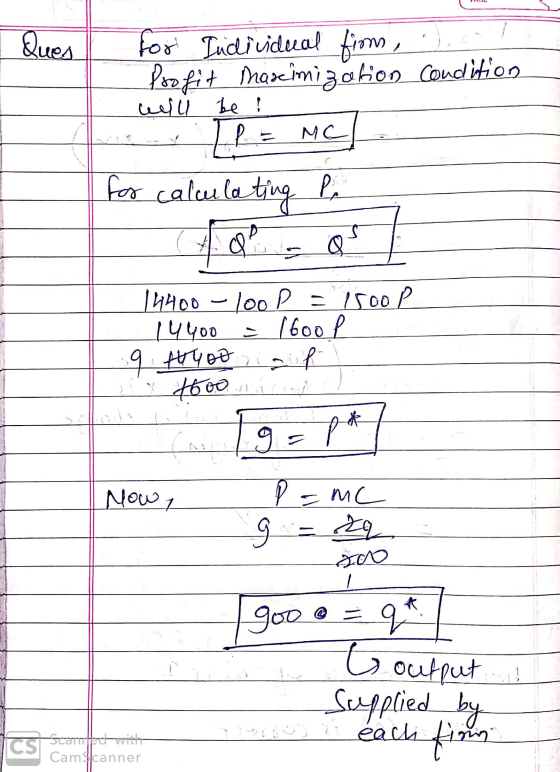

Suppose you are given the following information about a particular industry in the short run (perfect competition): QD = 200 − 2P Market demand QS = −120 + 6P Market supply C(q) = 4 + 30q + q2 Firm total cost function for an individual firm (10 pts) Find the equilibrium price & quantity in the market in the short run. (20 pts) Find the output supplied by the individual firm, and the number of firms in...

Suppose that the only two firms in an industry face the market (inverse) demand curve p=160-q.Each...

Suppose that the only two firms in an industry face the market (inverse) demand curve p=160-q.Each has constant marginal cost equal to 16 and no fixed costs. Initially the two firms compete as Cournot rivals (Chapter 11) and each produces an output of 48.Why might these firms want to merge to form a monopoly? What reason would antitrust authorities have for opposing the merger? (Hint:Calculate price, profits, and total surplus before and after the merger.)Suppose that each firm has fixed...

Suppose that the only two firms in an industry face the market (inverse) demand curve p-...

Suppose that the only two firms in an industry face the market (inverse) demand curve p- 130-Q. Each has constant marginal cost equal to 4 and no fixed costs. Initially the two firms compete as Cournot rivals (Chapter 11) and each produces an output of 42. Why might these firms want to merge to form a monopoly? What reason would antitrust authorities have for opposing the merger? (Hint: Calculate price, profits, and total surplus before and after the merger.) The...

Suppose that the only two firms in an industry face the market (inverse) demand curve p- 130-Q. Each has constant marginal cost equal to 4 and no fixed costs. Initially the two firms compete as Cournot rivals (Chapter 11) and each produces an output of 42. Why might these firms want to merge to form a monopoly? What reason would antitrust authorities have for opposing the merger? (Hint: Calculate price, profits, and total surplus before and after the merger.) The...

4. In a market for dry cleaning, the inverse market demand function is given by P=160-10...

4. In a market for dry cleaning, the inverse market demand function is given by P=160-10 and the (private) marginal cost of production for the aggregation of all dry dleaning firms is given by MC- 10+1Q. Finally, the pollution generated by the dry cleaning process creates external damages given by the marginal external cost curve MEC 1Q Calculate the output and price of dry cleaning if it is produced under competitive cond tions without regulation. The competitive equilbrium quanity is...

4. In a market for dry cleaning, the inverse market demand function is given by P=160-10 and the (private) marginal cost of production for the aggregation of all dry dleaning firms is given by MC- 10+1Q. Finally, the pollution generated by the dry cleaning process creates external damages given by the marginal external cost curve MEC 1Q Calculate the output and price of dry cleaning if it is produced under competitive cond tions without regulation. The competitive equilbrium quanity is...

Section iV: Problems 19. Suppose there is a competitive industry in which, at this market supply...

Section iV: Problems 19. Suppose there is a competitive industry in which, at this market supply is given by P-100 + Q A) What is the market price and quantity for the product in this market? In this industry, each firm faces a cost structure as follows: TC 100q+ q'. Based on this TC structure, Marginal cost 2q+ B) What is the firm's profit maximizing quantity of output? C) What is the firm's total revenue, total cost and profit? D)...

Section iV: Problems 19. Suppose there is a competitive industry in which, at this market supply is given by P-100 + Q A) What is the market price and quantity for the product in this market? In this industry, each firm faces a cost structure as follows: TC 100q+ q'. Based on this TC structure, Marginal cost 2q+ B) What is the firm's profit maximizing quantity of output? C) What is the firm's total revenue, total cost and profit? D)...

Please be descriptive. The market demand curve in a commodity chemical industry is given by Q...

Please be descriptive.

The market demand curve in a commodity chemical industry is given by Q 600 - 3P, where Q is the quantity demanded per month and P is the market price in dollars. Firms in this industry supply quantities every month, and the resulting market price occurs at the point at which the quantity demanded equals the total quantity supplied. Suppose there are two firms in this industry, Firm 1 and Firm 2. Each firm has an identical...

Please be descriptive.

The market demand curve in a commodity chemical industry is given by Q 600 - 3P, where Q is the quantity demanded per month and P is the market price in dollars. Firms in this industry supply quantities every month, and the resulting market price occurs at the point at which the quantity demanded equals the total quantity supplied. Suppose there are two firms in this industry, Firm 1 and Firm 2. Each firm has an identical...

Market Supply and Demand Functions Cost functions for a typical firm in the industry $72 $72...

Market Supply and Demand Functions Cost functions for a typical firm in the industry $72 $72 $68 $64 $60 $56 $52 $68 $64 ATC $40 $36 $28 $24 1800 2100 2400 2700 3000 3300 3600 3900 4200 4500 4800 0 2 4 6 8 10 12 14 16 18 20 Consider the file HW6 - Short Run & Long Run. Currently, the equilibrium price of the product is dollars per unit, the equilibrium quantity is units, and there are firms...

Market Supply and Demand Functions Cost functions for a typical firm in the industry $72 $72 $68 $64 $60 $56 $52 $68 $64 ATC $40 $36 $28 $24 1800 2100 2400 2700 3000 3300 3600 3900 4200 4500 4800 0 2 4 6 8 10 12 14 16 18 20 Consider the file HW6 - Short Run & Long Run. Currently, the equilibrium price of the product is dollars per unit, the equilibrium quantity is units, and there are firms...

Assume the following cost data are for a purely competitive producer: Average Product Fixed Cost Variable...

Assume the following cost data are for a purely competitive producer: Average Product Fixed Cost Variable Cost Total Cost Average Average Marginal Total Cost $60.00 $45.00 $105,00 $45.00 1 72.50 2 30.00 42.50 40.00 3 20.00 40.00 60.00 35.00 30.00 15.00 37.50 52.50 5 12.00 37.00 49.00 35.00 6 10.00 37.50 47.50 40.00 8.57 7 38.57 47.14 45.00 7.50 40.63 48.13 50.00 55.00 9 6.67 43.33 65.00 10 6.00 46.50 52.50 75.00 Answer the following questions (a - c) using...

Assume the following cost data are for a purely competitive producer: Average Product Fixed Cost Variable Cost Total Cost Average Average Marginal Total Cost $60.00 $45.00 $105,00 $45.00 1 72.50 2 30.00 42.50 40.00 3 20.00 40.00 60.00 35.00 30.00 15.00 37.50 52.50 5 12.00 37.00 49.00 35.00 6 10.00 37.50 47.50 40.00 8.57 7 38.57 47.14 45.00 7.50 40.63 48.13 50.00 55.00 9 6.67 43.33 65.00 10 6.00 46.50 52.50 75.00 Answer the following questions (a - c) using...

1. (20p) Suppose that, in a perfectly competitive industry, the technology for making the product (by...

1. (20p) Suppose that, in a perfectly competitive industry, the technology for making the product (by any single firm) has the total cost function c(q) = 200 + 4q+ Barriers to entry and exit the market are low and an unlimited number of firms could enter this industry, all with the same total cost function. (a) Compute the long-run equilibrium price in this industry, as well as the amount of output each firm would produce at this price. Explain the...

1. (20p) Suppose that, in a perfectly competitive industry, the technology for making the product (by any single firm) has the total cost function c(q) = 200 + 4q+ Barriers to entry and exit the market are low and an unlimited number of firms could enter this industry, all with the same total cost function. (a) Compute the long-run equilibrium price in this industry, as well as the amount of output each firm would produce at this price. Explain the...

4. The supply and demand in a given industry is defined by QD – 6500 – 100P and QS – 1200P respectively. In this industry, the cost function of an efficient firm is C(q) = 722 + 2/200. You can assume that all firms in the industry are efficient and identical) and the industry is operating under perfect competition. (a) Find the market equilibrium (prices and quantities) (b) Determine how much will each firm produce, and the profits for each...

4. The supply and demand in a given industry is defined by QD – 6500 – 100P and QS – 1200P respectively. In this industry, the cost function of an efficient firm is C(q) = 722 + 2/200. You can assume that all firms in the industry are efficient and identical) and the industry is operating under perfect competition. (a) Find the market equilibrium (prices and quantities) (b) Determine how much will each firm produce, and the profits for each...

Suppose that the only two firms in an industry face the market (inverse) demand curve p- 130-Q. Each has constant marginal cost equal to 4 and no fixed costs. Initially the two firms compete as Cournot rivals (Chapter 11) and each produces an output of 42. Why might these firms want to merge to form a monopoly? What reason would antitrust authorities have for opposing the merger? (Hint: Calculate price, profits, and total surplus before and after the merger.) The...

Suppose that the only two firms in an industry face the market (inverse) demand curve p- 130-Q. Each has constant marginal cost equal to 4 and no fixed costs. Initially the two firms compete as Cournot rivals (Chapter 11) and each produces an output of 42. Why might these firms want to merge to form a monopoly? What reason would antitrust authorities have for opposing the merger? (Hint: Calculate price, profits, and total surplus before and after the merger.) The...

4. In a market for dry cleaning, the inverse market demand function is given by P=160-10 and the (private) marginal cost of production for the aggregation of all dry dleaning firms is given by MC- 10+1Q. Finally, the pollution generated by the dry cleaning process creates external damages given by the marginal external cost curve MEC 1Q Calculate the output and price of dry cleaning if it is produced under competitive cond tions without regulation. The competitive equilbrium quanity is...

4. In a market for dry cleaning, the inverse market demand function is given by P=160-10 and the (private) marginal cost of production for the aggregation of all dry dleaning firms is given by MC- 10+1Q. Finally, the pollution generated by the dry cleaning process creates external damages given by the marginal external cost curve MEC 1Q Calculate the output and price of dry cleaning if it is produced under competitive cond tions without regulation. The competitive equilbrium quanity is...

Section iV: Problems 19. Suppose there is a competitive industry in which, at this market supply is given by P-100 + Q A) What is the market price and quantity for the product in this market? In this industry, each firm faces a cost structure as follows: TC 100q+ q'. Based on this TC structure, Marginal cost 2q+ B) What is the firm's profit maximizing quantity of output? C) What is the firm's total revenue, total cost and profit? D)...

Section iV: Problems 19. Suppose there is a competitive industry in which, at this market supply is given by P-100 + Q A) What is the market price and quantity for the product in this market? In this industry, each firm faces a cost structure as follows: TC 100q+ q'. Based on this TC structure, Marginal cost 2q+ B) What is the firm's profit maximizing quantity of output? C) What is the firm's total revenue, total cost and profit? D)...

Please be descriptive.

The market demand curve in a commodity chemical industry is given by Q 600 - 3P, where Q is the quantity demanded per month and P is the market price in dollars. Firms in this industry supply quantities every month, and the resulting market price occurs at the point at which the quantity demanded equals the total quantity supplied. Suppose there are two firms in this industry, Firm 1 and Firm 2. Each firm has an identical...

Please be descriptive.

The market demand curve in a commodity chemical industry is given by Q 600 - 3P, where Q is the quantity demanded per month and P is the market price in dollars. Firms in this industry supply quantities every month, and the resulting market price occurs at the point at which the quantity demanded equals the total quantity supplied. Suppose there are two firms in this industry, Firm 1 and Firm 2. Each firm has an identical...

Market Supply and Demand Functions Cost functions for a typical firm in the industry $72 $72 $68 $64 $60 $56 $52 $68 $64 ATC $40 $36 $28 $24 1800 2100 2400 2700 3000 3300 3600 3900 4200 4500 4800 0 2 4 6 8 10 12 14 16 18 20 Consider the file HW6 - Short Run & Long Run. Currently, the equilibrium price of the product is dollars per unit, the equilibrium quantity is units, and there are firms...

Market Supply and Demand Functions Cost functions for a typical firm in the industry $72 $72 $68 $64 $60 $56 $52 $68 $64 ATC $40 $36 $28 $24 1800 2100 2400 2700 3000 3300 3600 3900 4200 4500 4800 0 2 4 6 8 10 12 14 16 18 20 Consider the file HW6 - Short Run & Long Run. Currently, the equilibrium price of the product is dollars per unit, the equilibrium quantity is units, and there are firms...

Assume the following cost data are for a purely competitive producer: Average Product Fixed Cost Variable Cost Total Cost Average Average Marginal Total Cost $60.00 $45.00 $105,00 $45.00 1 72.50 2 30.00 42.50 40.00 3 20.00 40.00 60.00 35.00 30.00 15.00 37.50 52.50 5 12.00 37.00 49.00 35.00 6 10.00 37.50 47.50 40.00 8.57 7 38.57 47.14 45.00 7.50 40.63 48.13 50.00 55.00 9 6.67 43.33 65.00 10 6.00 46.50 52.50 75.00 Answer the following questions (a - c) using...

Assume the following cost data are for a purely competitive producer: Average Product Fixed Cost Variable Cost Total Cost Average Average Marginal Total Cost $60.00 $45.00 $105,00 $45.00 1 72.50 2 30.00 42.50 40.00 3 20.00 40.00 60.00 35.00 30.00 15.00 37.50 52.50 5 12.00 37.00 49.00 35.00 6 10.00 37.50 47.50 40.00 8.57 7 38.57 47.14 45.00 7.50 40.63 48.13 50.00 55.00 9 6.67 43.33 65.00 10 6.00 46.50 52.50 75.00 Answer the following questions (a - c) using...

1. (20p) Suppose that, in a perfectly competitive industry, the technology for making the product (by any single firm) has the total cost function c(q) = 200 + 4q+ Barriers to entry and exit the market are low and an unlimited number of firms could enter this industry, all with the same total cost function. (a) Compute the long-run equilibrium price in this industry, as well as the amount of output each firm would produce at this price. Explain the...

1. (20p) Suppose that, in a perfectly competitive industry, the technology for making the product (by any single firm) has the total cost function c(q) = 200 + 4q+ Barriers to entry and exit the market are low and an unlimited number of firms could enter this industry, all with the same total cost function. (a) Compute the long-run equilibrium price in this industry, as well as the amount of output each firm would produce at this price. Explain the...

Most questions answered within 3 hours.

-

3. Gains from trade

Consider two neighbouring island countries called Euphoria and

Contente. They each have...

asked 54 minutes ago -

A business executive has the option to invest money in two

plans: Plan A guarantees that...

asked 3 hours ago -

Hello, can someone please help me answer this question?

How much heat is absorbed by a...

asked 3 hours ago -

. A marketing researcher conducted a survey of 25 shoppers

randomly selected at the local mall...

asked 3 hours ago -

Create an comprehensive response to the

following:

Antimicrobial agents work on a multitude of microbes (bacteria,...

asked 3 hours ago -

6.13 LAB: Step counter. Section 6.3.

A pedometer treats walking 2,000 steps as walking 1 mile....

asked 3 hours ago -

(14.2) A block of mass m = 10 kg riding on a frictionless

horizontal plane is...

asked 3 hours ago -

Use any search engine to search for articles about Starbucks

partnership with Tata Companies in India...

asked 3 hours ago -

Let’s say that for some reason Bank Excess Reserves suddenly

increase sharply. What effect would this...

asked 3 hours ago -

Given:

Curent Assets: $600,000

Total Assets: $2,600,000

Current Liabilities: $500,000

Total Liabilities: $1,700,000

What is the...

asked 3 hours ago -

1. What is a “Bankster”? What is insider trading? Why is it

illegal?

2. What is...

asked 3 hours ago -

A transverse wave on a cord is given by

D(x,t)=0.18sin(2.7x−61.0t), where Dand x are in m...

asked 3 hours ago