Homework Answers

Add Answer to:

The current price of a stock is $31.50 per share, and six-month European call options on...

You own six call option contracts on WAN stock with a strike price of $30. When...

You own six call option contracts on WAN stock with a strike price of $30. When you purchased the shares the option price was $.45 and the stock price was $30.10. What is the total intrinsic value of these options if the stock is currently selling for $29.70 a share?

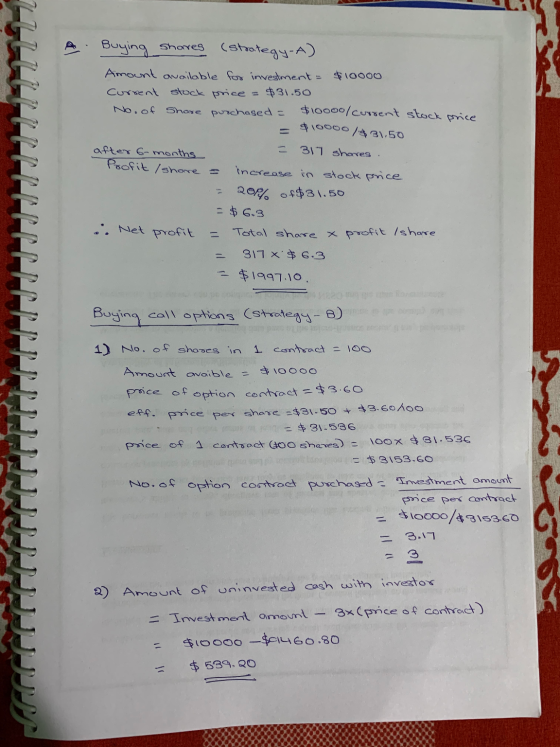

5. Suppose the current price of a stock is $35, and one associated six-month call option...

5. Suppose the current price of a stock is $35, and one associated six-month call option with a strike price of $36 currently sell for $3.5. Rachel Heyhoe-Flint, an amateur investor, feels that the price of the stock will increase and so she comes up with the following two possible strategies: (i) purchase 100 shares and (ii) buying 1,000 call options. Both strategies involve an investment of $3,500. How much the stock has to rise after six months for the...

5. Suppose the current price of a stock is $35, and one associated six-month call option with a strike price of $36 currently sell for $3.5. Rachel Heyhoe-Flint, an amateur investor, feels that the price of the stock will increase and so she comes up with the following two possible strategies: (i) purchase 100 shares and (ii) buying 1,000 call options. Both strategies involve an investment of $3,500. How much the stock has to rise after six months for the...

A trader buys a 1M European call option on a share. The stock price is £108...

A trader buys a 1M European call option on a share. The stock price is £108 and the strike price is £97. 1)What is the intrinsic value of this option? 2)How would the intrinsic value change if this were a 9M option? 3) Will this option be exercised at maturity? Why or why not? 4)What is time value and how does it change the price of an option?

An investor sells a European call on a share for S3 The stock price is $26...

An investor sells a European call on a share for S3 The stock price is $26 and the strike price is $29. Under what circumstanc 4- es does the investor make a profit? Under what circumstances will the option be exercised? Draw a diagram showing the variation of the investor's profit with the stock price at the maturity of the option.

An investor sells a European call on a share for S3 The stock price is $26 and the strike price is $29. Under what circumstanc 4- es does the investor make a profit? Under what circumstances will the option be exercised? Draw a diagram showing the variation of the investor's profit with the stock price at the maturity of the option.

A trader creates a long strangle with put options with a strike price of $160 per...

A trader creates a long strangle with put options with a strike price of $160 per share, and call options with a strike price of $170 per share by trading a total of 20 option contracts (10 put contracts and 10 call contracts). Each contract is written on 100 shares of stock. The put option is worth $18 per share, and the call option is worth $15 per share. What is the value (payoff) of the strangle at maturity as...

A trader creates a long strangle with put options with a strike price of $160 per...

A trader creates a long strangle with put options with a strike price of $160 per share, and call options with a strike price of $170 per share by trading a total of 20 option contracts (10 put contracts and 10 call contracts). Each contract is written on 100 shares of stock. The put option is worth $18 per share, and the call option is worth $15 per share. What is the value (payoff) of the strangle at maturity as...

Open Buying a Call Stock Option Open Buying a Put Stock Option Number Strike Stock Call...

Open Buying a Call Stock Option Open Buying a Put Stock Option Number Strike Stock Call Number Strike Stock Put of Contracts Price Price Premium of Contracts Price Price Premium 1 36 35 1.25 1 36 35 1.45 Intrinsic Value Intrinsic Value Time Value Time Value Cost Cost Close Close Number Strike Stock Call Number Strike Stock Put of Contracts Price Price Premium of Contracts Price Price Premium 1 36 40 4.25 1 36 40 0.05 Intrinsic Value Intrinsic Value...

1. Apple stock is selling for $120 per share. Call options with a $117 exercise price...

1. Apple stock is selling for $120 per share. Call options with a $117 exercise price are priced at $12. What is the intrinsic value of the option, and what is the time value? 2. Twitter is trading at $34.50. Call options with a strike price of $35 are priced at $2.30. What is the intrinsic value of the option, and what is the time value?

An investor sells a European call on a share for $13. The strike price is $36. Under what circumstances does the in...

An investor sells a European call on a share for $13. The strike price is $36. Under what circumstances does the investor make a profit? Under what circumstances will the option be exercised? Draw a diagram showing the variation of the investor's profit with the stock price at the maturity of the option.

An investor sells a European call on a share for $13. The strike price is $36. Under what circumstances does the investor make a profit? Under what circumstances will the option be exercised? Draw a diagram showing the variation of the investor's profit with the stock price at the maturity of the option.

The current price of the Gilead stock is $77 per share. Consider an option strategy, which...

The current price of the Gilead stock is $77 per share. Consider an option strategy, which consists of following positions: Selling one put option on the Gilead stock with the strike price of $75. The price of this put option is $3.44. Buying one put option on the Gilead stock with the strike price of $72. The price of this option is $2.24. Buying one call option on the Gilead stock with the strike price of $81. The price of...

5. Suppose the current price of a stock is $35, and one associated six-month call option with a strike price of $36 currently sell for $3.5. Rachel Heyhoe-Flint, an amateur investor, feels that the price of the stock will increase and so she comes up with the following two possible strategies: (i) purchase 100 shares and (ii) buying 1,000 call options. Both strategies involve an investment of $3,500. How much the stock has to rise after six months for the...

5. Suppose the current price of a stock is $35, and one associated six-month call option with a strike price of $36 currently sell for $3.5. Rachel Heyhoe-Flint, an amateur investor, feels that the price of the stock will increase and so she comes up with the following two possible strategies: (i) purchase 100 shares and (ii) buying 1,000 call options. Both strategies involve an investment of $3,500. How much the stock has to rise after six months for the...

An investor sells a European call on a share for S3 The stock price is $26 and the strike price is $29. Under what circumstanc 4- es does the investor make a profit? Under what circumstances will the option be exercised? Draw a diagram showing the variation of the investor's profit with the stock price at the maturity of the option.

An investor sells a European call on a share for S3 The stock price is $26 and the strike price is $29. Under what circumstanc 4- es does the investor make a profit? Under what circumstances will the option be exercised? Draw a diagram showing the variation of the investor's profit with the stock price at the maturity of the option.

An investor sells a European call on a share for $13. The strike price is $36. Under what circumstances does the investor make a profit? Under what circumstances will the option be exercised? Draw a diagram showing the variation of the investor's profit with the stock price at the maturity of the option.

An investor sells a European call on a share for $13. The strike price is $36. Under what circumstances does the investor make a profit? Under what circumstances will the option be exercised? Draw a diagram showing the variation of the investor's profit with the stock price at the maturity of the option.

Most questions answered within 3 hours.

-

The extent to which assets are financed by borrowed funds and

other liabilities is indicated by:...

asked 34 minutes ago -

Explain in detail

Germany is the fifth largest economy

explain what goods and services Germany specializes...

asked 49 minutes ago -

The density of platinum is 21.45 g/mL. If a cube of platinum

with a mass of...

asked 54 minutes ago -

Accounts Receivable

Sales

A/R Posting

Extended Sales Invoice

Packing Slip

Compare invoice to packing slip 2...

asked 57 minutes ago -

Michaella, age 23, is a full-time law student and is claimed by

her parents as a...

asked 58 minutes ago -

Why are polymers not typically casted into products?

asked 1 hour ago -

When rolling a die 129 times, what is the probability of rolling

a 6 no more...

asked 1 hour ago -

4. A call option currently sells for $7.75. It has a strike

price of $85 and...

asked 1 hour ago -

1.

You need to prepare 10.0 liters of an acid aqueous solution with a

pH of...

asked 1 hour ago -

Along an aggregate supply curve, if the level of output is less

than the natural level...

asked 1 hour ago -

By 2025, annual consumption in emerging markets will total $30

trillion and contribute more than ________...

asked 1 hour ago -

At what point does reformation cease to be a viable option for

those who are oppressed...

asked 1 hour ago