Homework Answers

(a) Given that Total Cost = C(q) = 3q2+100 so we know that Total cost = Variable cost + Fixed cost, so here Total Fixed cost is 100 and Total Variabe cost is 3q2.

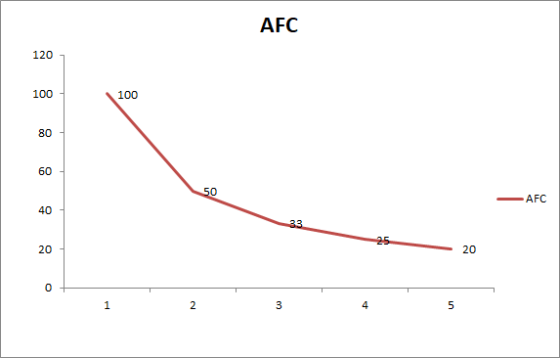

(b) Average Total Cost(ATC) is Total cost divided by quantity so ATC = (3q2+100)/q = 3q + (100/q ) which includes Average Fixed Cost = (100/q) and Average Variable Cost = 3q.

(c) Graph of Average Fixed cost on Vertical axis show AFC and On Horizontal axis show quantity of cars

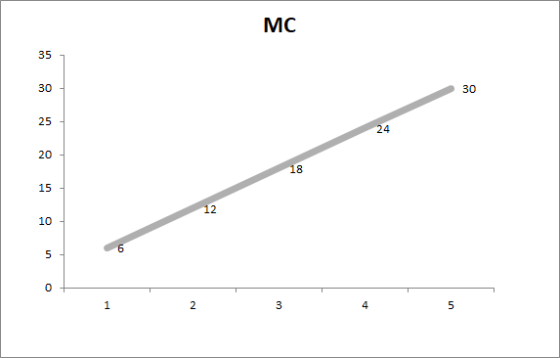

(d) Marginal cost is first order condition of Total Cost Function so given that C(q) = 3q2+100 differentiate with respect to q. so we get Marginal cost = 6q

Above graph on vertical axis show marginal cost and Horizontal axis show quantity of cars

(e) firm unit cost function is C(q) = 3q2+100 when quantity is 1 so C(q) = 103

Firm Average total cost at when quantity is 1 so ATC = 3q + (100/q ) = 103 so here ATC = Firm unit cost its show that firm produces car at constant return to scale.

Add Answer to:

answer only part e

Problem 2 Bueller & Frye Auto sells cars. Their costs are described...

e) Suppose that a competitive firm's marginal cost of producing output q is given by MC(q)...

e) Suppose that a competitive firm's marginal cost of producing output q is given by MC(q) -3+2q. Assume that the market price of the firm's product is $9. i) What level of output will the firm produce? (2p) ii) What is the firm's producer surplus? (4p) ii) Suppose that the average variable cost of the firm is given by AVC(g)-3+q. Suppose that the firm's fixed costs are known to be $3. Will the firm be earning a positive, negative, or...

e) Suppose that a competitive firm's marginal cost of producing output q is given by MC(q) -3+2q. Assume that the market price of the firm's product is $9. i) What level of output will the firm produce? (2p) ii) What is the firm's producer surplus? (4p) ii) Suppose that the average variable cost of the firm is given by AVC(g)-3+q. Suppose that the firm's fixed costs are known to be $3. Will the firm be earning a positive, negative, or...

Short-Run Market Supply. New England Textiles, Inc., is a medium-sized manufacturer of blue denim that sells in a perfectly competitive market. Given $25,000 in fixed costs, the total cost function f...

Short-Run Market Supply. New England Textiles, Inc., is a medium-sized manufacturer of blue denim that sells in a perfectly competitive market. Given $25,000 in fixed costs, the total cost function for this product is described by TC $25,000 $1Q S0.000008 Q Mc= aTCaQ = $1 + $0.00001 6Q where Q is square yards of blue denim produced per month. Assume that MC> AVC at every point along the firm's marginal cost curve, and that total costs include a normal profit....

Short-Run Market Supply. New England Textiles, Inc., is a medium-sized manufacturer of blue denim that sells in a perfectly competitive market. Given $25,000 in fixed costs, the total cost function for this product is described by TC $25,000 $1Q S0.000008 Q Mc= aTCaQ = $1 + $0.00001 6Q where Q is square yards of blue denim produced per month. Assume that MC> AVC at every point along the firm's marginal cost curve, and that total costs include a normal profit....

This homework assignment compares a competitive market with a monopolistic market. The market demand curve is...

This homework assignment compares a competitive market with a monopolistic market. The market demand curve is P 122-¼Q. For each firm, marginal oosts are 20 + qi50 and fixed costs are 1 00. We assume first that the market is competitive. Module 8explains the competitive pricing procedure. Wederive the long-run price from the firms' cost curve competitive firms price at long-run minimum average costs. Question: Why is this relation true? Answer: Decreasing marginal utility implies an upward sloping marginal cost...

This homework assignment compares a competitive market with a monopolistic market. The market demand curve is P 122-¼Q. For each firm, marginal oosts are 20 + qi50 and fixed costs are 1 00. We assume first that the market is competitive. Module 8explains the competitive pricing procedure. Wederive the long-run price from the firms' cost curve competitive firms price at long-run minimum average costs. Question: Why is this relation true? Answer: Decreasing marginal utility implies an upward sloping marginal cost...

NEED ALL ANSWERS PLEASE Problem 3 [24 marks] A competitive firm uses two inputs, capital (k) and labour (), to produce...

NEED ALL ANSWERS PLEASE

Problem 3 [24 marks] A competitive firm uses two inputs, capital (k) and labour (), to produce one output, (y). The price of capital, W, is S1 per unit and the price of labor, wi, is SI per unit. The firm operates in competitive markets for outputs and inputs, so takes the prices as given. The production function is f(k,l) 3k025/025. The maximum amount of output produced for a givern amount of inputs is y(k, l)...

NEED ALL ANSWERS PLEASE

Problem 3 [24 marks] A competitive firm uses two inputs, capital (k) and labour (), to produce one output, (y). The price of capital, W, is S1 per unit and the price of labor, wi, is SI per unit. The firm operates in competitive markets for outputs and inputs, so takes the prices as given. The production function is f(k,l) 3k025/025. The maximum amount of output produced for a givern amount of inputs is y(k, l)...

Can you answer these questions please. all of them 2. A firm's product sells for $2...

Can you answer these questions please. all of them

2. A firm's product sells for $2 per unit in a highly competitive market. The firm pro duces output using capital (which it rents at $75 per hour) and labor (which is paid a wage of S15 per hour under a contract for 20 hours of labor services). Complete the following table and use that information to answer the questions that follow. 20 0 1 20 50 2 20 150 3...

Can you answer these questions please. all of them

2. A firm's product sells for $2 per unit in a highly competitive market. The firm pro duces output using capital (which it rents at $75 per hour) and labor (which is paid a wage of S15 per hour under a contract for 20 hours of labor services). Complete the following table and use that information to answer the questions that follow. 20 0 1 20 50 2 20 150 3...

please help with b and c, thank you! INDTAP Firms in Competitive Markets (Ch 14) ents...

please help with b and c, thank you!

INDTAP Firms in Competitive Markets (Ch 14) ents relevant A A A 11. Suppose that each firm in a competitive industry has the following costs: Total cost: TC = 50+ Marginal cost: MC- where q is an individual firm's quantity produced. The market demand curve for this product is Demand: P = 120-P where P is the price and Q is the total quantity of the good. Currently, there are 9 firms...

please help with b and c, thank you!

INDTAP Firms in Competitive Markets (Ch 14) ents relevant A A A 11. Suppose that each firm in a competitive industry has the following costs: Total cost: TC = 50+ Marginal cost: MC- where q is an individual firm's quantity produced. The market demand curve for this product is Demand: P = 120-P where P is the price and Q is the total quantity of the good. Currently, there are 9 firms...

Part 2: Short answer questions Question 1 (4 points): A sausage firm has a production function...

Part 2: Short answer questions Question 1 (4 points): A sausage firm has a production function of the form: q = 5LK+K+L where q is units per day, L is units of labor input and K is units of capital output. The marginal product of the two inputs are: MPL = 5K+1, MPK = 5L +1. Price per unit of labor: w= $15, price per unit of capital: v= $15. Both labor and capital are variable. a. Write down the...

Part 2: Short answer questions Question 1 (4 points): A sausage firm has a production function of the form: q = 5LK+K+L where q is units per day, L is units of labor input and K is units of capital output. The marginal product of the two inputs are: MPL = 5K+1, MPK = 5L +1. Price per unit of labor: w= $15, price per unit of capital: v= $15. Both labor and capital are variable. a. Write down the...

Costs per unit $22 - - 10 Quantity of output Answer the following questions referring to...

Costs per unit $22 - - 10 Quantity of output Answer the following questions referring to Q = 10 1. Identify the curves in the diagram. (a) Curve A - Curve B Curve C - 2. What is average fixed cost? 3. What is variable cost? 4. What is total cost? 5. On the graph, identify the area that represents the total variable cost and total fixed cost when the quantity of output =10.

Costs per unit $22 - - 10 Quantity of output Answer the following questions referring to Q = 10 1. Identify the curves in the diagram. (a) Curve A - Curve B Curve C - 2. What is average fixed cost? 3. What is variable cost? 4. What is total cost? 5. On the graph, identify the area that represents the total variable cost and total fixed cost when the quantity of output =10.

These two question please Question 8 (1 point) When do constant returns to scale occur? when...

These two question please

Question 8 (1 point) When do constant returns to scale occur? when long-run total costs are constant as output increases when long-run average total costs are constant as output increases when the firm's long-run average-cost curve is falling as output increases when the firm's long-run average-cost curve is rising as output increases Figure 13-4 The curves in this figure reflect information about the average total cost, average fixed cost, average variable cost, and marginal cost for...

These two question please

Question 8 (1 point) When do constant returns to scale occur? when long-run total costs are constant as output increases when long-run average total costs are constant as output increases when the firm's long-run average-cost curve is falling as output increases when the firm's long-run average-cost curve is rising as output increases Figure 13-4 The curves in this figure reflect information about the average total cost, average fixed cost, average variable cost, and marginal cost for...

Matching (15 pts) a.) Average fixed costs b.) Average product c.) Average total cost d.) Average...

Matching (15 pts) a.) Average fixed costs b.) Average product c.) Average total cost d.) Average variable cost e.) Diseconomies of scale f.) Economies of scale 9.) Fixed costs m.) Optimal output rule h.) Law of diminishing marginal productivity n.) Profit i.) Long run 0.) Short run 1.) Marginal cost p.) Total cost k.) Marginal product q.) Total product 1.) Marginal revenue r.) Variable costs 1.) Total revenue minus total cost 2.) The sum of total fixed and total variable...

Matching (15 pts) a.) Average fixed costs b.) Average product c.) Average total cost d.) Average variable cost e.) Diseconomies of scale f.) Economies of scale 9.) Fixed costs m.) Optimal output rule h.) Law of diminishing marginal productivity n.) Profit i.) Long run 0.) Short run 1.) Marginal cost p.) Total cost k.) Marginal product q.) Total product 1.) Marginal revenue r.) Variable costs 1.) Total revenue minus total cost 2.) The sum of total fixed and total variable...

e) Suppose that a competitive firm's marginal cost of producing output q is given by MC(q) -3+2q. Assume that the market price of the firm's product is $9. i) What level of output will the firm produce? (2p) ii) What is the firm's producer surplus? (4p) ii) Suppose that the average variable cost of the firm is given by AVC(g)-3+q. Suppose that the firm's fixed costs are known to be $3. Will the firm be earning a positive, negative, or...

e) Suppose that a competitive firm's marginal cost of producing output q is given by MC(q) -3+2q. Assume that the market price of the firm's product is $9. i) What level of output will the firm produce? (2p) ii) What is the firm's producer surplus? (4p) ii) Suppose that the average variable cost of the firm is given by AVC(g)-3+q. Suppose that the firm's fixed costs are known to be $3. Will the firm be earning a positive, negative, or...

Short-Run Market Supply. New England Textiles, Inc., is a medium-sized manufacturer of blue denim that sells in a perfectly competitive market. Given $25,000 in fixed costs, the total cost function for this product is described by TC $25,000 $1Q S0.000008 Q Mc= aTCaQ = $1 + $0.00001 6Q where Q is square yards of blue denim produced per month. Assume that MC> AVC at every point along the firm's marginal cost curve, and that total costs include a normal profit....

Short-Run Market Supply. New England Textiles, Inc., is a medium-sized manufacturer of blue denim that sells in a perfectly competitive market. Given $25,000 in fixed costs, the total cost function for this product is described by TC $25,000 $1Q S0.000008 Q Mc= aTCaQ = $1 + $0.00001 6Q where Q is square yards of blue denim produced per month. Assume that MC> AVC at every point along the firm's marginal cost curve, and that total costs include a normal profit....

This homework assignment compares a competitive market with a monopolistic market. The market demand curve is P 122-¼Q. For each firm, marginal oosts are 20 + qi50 and fixed costs are 1 00. We assume first that the market is competitive. Module 8explains the competitive pricing procedure. Wederive the long-run price from the firms' cost curve competitive firms price at long-run minimum average costs. Question: Why is this relation true? Answer: Decreasing marginal utility implies an upward sloping marginal cost...

This homework assignment compares a competitive market with a monopolistic market. The market demand curve is P 122-¼Q. For each firm, marginal oosts are 20 + qi50 and fixed costs are 1 00. We assume first that the market is competitive. Module 8explains the competitive pricing procedure. Wederive the long-run price from the firms' cost curve competitive firms price at long-run minimum average costs. Question: Why is this relation true? Answer: Decreasing marginal utility implies an upward sloping marginal cost...

NEED ALL ANSWERS PLEASE

Problem 3 [24 marks] A competitive firm uses two inputs, capital (k) and labour (), to produce one output, (y). The price of capital, W, is S1 per unit and the price of labor, wi, is SI per unit. The firm operates in competitive markets for outputs and inputs, so takes the prices as given. The production function is f(k,l) 3k025/025. The maximum amount of output produced for a givern amount of inputs is y(k, l)...

NEED ALL ANSWERS PLEASE

Problem 3 [24 marks] A competitive firm uses two inputs, capital (k) and labour (), to produce one output, (y). The price of capital, W, is S1 per unit and the price of labor, wi, is SI per unit. The firm operates in competitive markets for outputs and inputs, so takes the prices as given. The production function is f(k,l) 3k025/025. The maximum amount of output produced for a givern amount of inputs is y(k, l)...

Can you answer these questions please. all of them

2. A firm's product sells for $2 per unit in a highly competitive market. The firm pro duces output using capital (which it rents at $75 per hour) and labor (which is paid a wage of S15 per hour under a contract for 20 hours of labor services). Complete the following table and use that information to answer the questions that follow. 20 0 1 20 50 2 20 150 3...

Can you answer these questions please. all of them

2. A firm's product sells for $2 per unit in a highly competitive market. The firm pro duces output using capital (which it rents at $75 per hour) and labor (which is paid a wage of S15 per hour under a contract for 20 hours of labor services). Complete the following table and use that information to answer the questions that follow. 20 0 1 20 50 2 20 150 3...

please help with b and c, thank you!

INDTAP Firms in Competitive Markets (Ch 14) ents relevant A A A 11. Suppose that each firm in a competitive industry has the following costs: Total cost: TC = 50+ Marginal cost: MC- where q is an individual firm's quantity produced. The market demand curve for this product is Demand: P = 120-P where P is the price and Q is the total quantity of the good. Currently, there are 9 firms...

please help with b and c, thank you!

INDTAP Firms in Competitive Markets (Ch 14) ents relevant A A A 11. Suppose that each firm in a competitive industry has the following costs: Total cost: TC = 50+ Marginal cost: MC- where q is an individual firm's quantity produced. The market demand curve for this product is Demand: P = 120-P where P is the price and Q is the total quantity of the good. Currently, there are 9 firms...

Part 2: Short answer questions Question 1 (4 points): A sausage firm has a production function of the form: q = 5LK+K+L where q is units per day, L is units of labor input and K is units of capital output. The marginal product of the two inputs are: MPL = 5K+1, MPK = 5L +1. Price per unit of labor: w= $15, price per unit of capital: v= $15. Both labor and capital are variable. a. Write down the...

Part 2: Short answer questions Question 1 (4 points): A sausage firm has a production function of the form: q = 5LK+K+L where q is units per day, L is units of labor input and K is units of capital output. The marginal product of the two inputs are: MPL = 5K+1, MPK = 5L +1. Price per unit of labor: w= $15, price per unit of capital: v= $15. Both labor and capital are variable. a. Write down the...

Costs per unit $22 - - 10 Quantity of output Answer the following questions referring to Q = 10 1. Identify the curves in the diagram. (a) Curve A - Curve B Curve C - 2. What is average fixed cost? 3. What is variable cost? 4. What is total cost? 5. On the graph, identify the area that represents the total variable cost and total fixed cost when the quantity of output =10.

Costs per unit $22 - - 10 Quantity of output Answer the following questions referring to Q = 10 1. Identify the curves in the diagram. (a) Curve A - Curve B Curve C - 2. What is average fixed cost? 3. What is variable cost? 4. What is total cost? 5. On the graph, identify the area that represents the total variable cost and total fixed cost when the quantity of output =10.

These two question please

Question 8 (1 point) When do constant returns to scale occur? when long-run total costs are constant as output increases when long-run average total costs are constant as output increases when the firm's long-run average-cost curve is falling as output increases when the firm's long-run average-cost curve is rising as output increases Figure 13-4 The curves in this figure reflect information about the average total cost, average fixed cost, average variable cost, and marginal cost for...

These two question please

Question 8 (1 point) When do constant returns to scale occur? when long-run total costs are constant as output increases when long-run average total costs are constant as output increases when the firm's long-run average-cost curve is falling as output increases when the firm's long-run average-cost curve is rising as output increases Figure 13-4 The curves in this figure reflect information about the average total cost, average fixed cost, average variable cost, and marginal cost for...

Matching (15 pts) a.) Average fixed costs b.) Average product c.) Average total cost d.) Average variable cost e.) Diseconomies of scale f.) Economies of scale 9.) Fixed costs m.) Optimal output rule h.) Law of diminishing marginal productivity n.) Profit i.) Long run 0.) Short run 1.) Marginal cost p.) Total cost k.) Marginal product q.) Total product 1.) Marginal revenue r.) Variable costs 1.) Total revenue minus total cost 2.) The sum of total fixed and total variable...

Matching (15 pts) a.) Average fixed costs b.) Average product c.) Average total cost d.) Average variable cost e.) Diseconomies of scale f.) Economies of scale 9.) Fixed costs m.) Optimal output rule h.) Law of diminishing marginal productivity n.) Profit i.) Long run 0.) Short run 1.) Marginal cost p.) Total cost k.) Marginal product q.) Total product 1.) Marginal revenue r.) Variable costs 1.) Total revenue minus total cost 2.) The sum of total fixed and total variable...

Most questions answered within 3 hours.

-

Which of the following quotes from a new-product adopter would

signal the need for a firm...

asked 11 minutes ago -

Why are anthropologists interested in studying exchange across

cultures?

asked 4 minutes ago -

3. You may be aware that Wal-Mart is also using RFID

technologies at their stores. Name...

asked 11 minutes ago -

What are the key benefits and limitations of a relational

DBMS?

asked 15 minutes ago -

A medium-sized carrot weighs 64 g and contains 7.0 g of

carbohydrate.

What percent, by mass,...

asked 17 minutes ago -

Please design 3 different and unique brackets consisting of TOP,

FRONT, RIGHT or LEFT views with...

asked 33 minutes ago -

La Niña conditions are forecasted to result in dry conditions in

the spring. You are trying...

asked 41 minutes ago -

The YTM on a 6-month $20 par value zero-coupon bond is 18%, and

the YTM on...

asked 42 minutes ago -

Write In JAVA:

Part 1

The use of computers in education is referred to as

computer-assisted...

asked 49 minutes ago -

Show all of your work and use the half-reaction method

for acidic redox reactions.

1.

H2O2aq+...

asked 51 minutes ago -

The Harry and Belinda Johnson Family Might Have a Career

Change

Harry has started out fine...

asked 57 minutes ago -

Tyler Company acquired all of Jasmine Company’s outstanding

stock on January 1, 2016, for $244,700 in...

asked 1 hour ago