![Question Two [Total 50 marks] Suppose the market of carpets is competitive. The demand for and the supply of carpets in the m](http://img.homeworklib.com/questions/9f942ad0-9637-11ea-8900-ebeb24466560.png?x-oss-process=image/resize,w_560)

Homework Answers

Add Answer to:

Question Two [Total 50 marks] Suppose the market of carpets is competitive. The demand for and...

Suppose the market of carpets is competitive. The demand for and the supply of tables have...

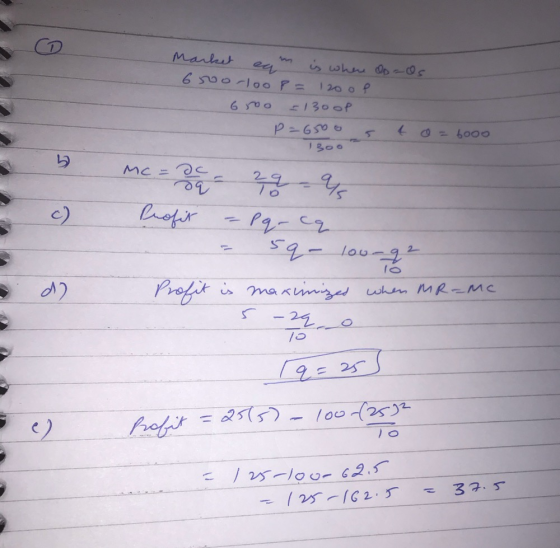

Suppose the market of carpets is competitive. The demand for and the supply of tables have been estimated as follows: Q = 370 – 10P Q = 80P +10 A typical firm producing tables has a total cost function of C = 64 +?2/4 a. Find the equilibrium market price and quantity. (2 marks) b. Derive MC and AC functions of a typical firm. Then find the efficient scale of output of the firm. Show your steps clearly. (5 marks)...

Question 3 (32 marks) a The market of popcom is perfectly competitive. The market demand curve...

Question 3 (32 marks) a The market of popcom is perfectly competitive. The market demand curve and supply curve are as follows: Demand: Qp = 2000-P Supply: 2 = 1400 +2P Firm K is one of the many firms producing popcorn in the market. The total cost function and marginal cost function are as follows: TC(q) =1250 +30 +29 MC(q) - 30 +49 i At what output level (g) would the average total cost be minimized? (6 marks) ii What...

Question 3 (32 marks) a The market of popcom is perfectly competitive. The market demand curve and supply curve are as follows: Demand: Qp = 2000-P Supply: 2 = 1400 +2P Firm K is one of the many firms producing popcorn in the market. The total cost function and marginal cost function are as follows: TC(q) =1250 +30 +29 MC(q) - 30 +49 i At what output level (g) would the average total cost be minimized? (6 marks) ii What...

(20 marks) Suppose the market for disposable gloves is competitive and it is originally operating at...

(20 marks) Suppose the market for disposable gloves is competitive and it is originally operating at the long run equilibrium. An important raw material of producing disposable gloves is natural rubber. Suppose there is a drastic increase in the price of natural rubber. With the aid of side-by-side diagrams, explain the impacts of the above change on the equilibrium price and equilibrium quantity in the market for disposable gloves, as well as the profit maximizing output level of a typical...

(20 marks) Suppose the market for disposable gloves is competitive and it is originally operating at the long run equilibrium. An important raw material of producing disposable gloves is natural rubber. Suppose there is a drastic increase in the price of natural rubber. With the aid of side-by-side diagrams, explain the impacts of the above change on the equilibrium price and equilibrium quantity in the market for disposable gloves, as well as the profit maximizing output level of a typical...

1. Suppose there is a decrease in the price of gasoline. With the aid of a...

1. Suppose there is a decrease in the price of gasoline. With the aid of a demandand-supply diagram, explain how this will affect the equilibrium price and quantity in the market of gasoline cars. (6 marks) 2. Suppose the market for Japanese grapes is represented by: Supply: Q = 400 + P2 Demand: Q = 1000 – 5P2 i) Find the market equilibrium price and quantity. ii) Calculate the price elasticity of demand when the market is at the equilibrium....

[1] A perfectly competitive aluminum producer is currently producing a quantity where the market price is...

[1] A perfectly competitive aluminum producer is currently producing a quantity where the market price is $0.67 per pound (i.e., 67 cents per pound), average total cost is $0.70, and average variable cost of $0.60 (which corresponds to the minimum point on the average variable cost curve). Would you recommend this firm expand output, contract output, or shut down in the short-run? Provide a graph to illustrate your answer. [2] Suppose the local crawfish market is perfectly competitive, with the...

Question 5 (15 marks) Market demand is given as QD = 120 - P. Market supply...

Question 5 (15 marks) Market demand is given as QD = 120 - P. Market supply is given as QS = 4P. Each identical firm has MC = 6Q and ATC = 3Q. Showing your calculations, answer the following questions: A) What quantity of output will a typical firm produce? (5 marks) B) What is a typical firm's average total cost? (5 marks) C) What is a a typical firm's profit? (5 marks)

Question 5 (15 marks) Market demand is given as QD = 120 - P. Market supply is given as QS = 4P. Each identical firm has MC = 6Q and ATC = 3Q. Showing your calculations, answer the following questions: A) What quantity of output will a typical firm produce? (5 marks) B) What is a typical firm's average total cost? (5 marks) C) What is a a typical firm's profit? (5 marks)

Suppose the market for canola oil is perfectly competitive. There are 1,000 firms in the market,...

Suppose the market for canola oil is perfectly competitive. There are 1,000 firms in the market, each of which have a fixed cost of FC=2 and a marginal cost of MC= 1+Q, where q is quantity produced by an individual firm. Let QS denote the total quantity supplied in the market. The market demand is QD= 15,250-250P A) Find the market supply equation, that is write QS as a function of price P B)What is the equilibrium price? What is...

1. Suppose the market for canola oil is perfectly competitive. There are 1.000 firms in the...

1. Suppose the market for canola oil is perfectly competitive. There are 1.000 firms in the market, each of which have a fixed cost of FC = 2 and a marginal cost of MC = 1 + q, where q is the quantity produced by an individual firm. Let Q. denote the total quantity supplied in the market. The market demand for canola oil is given by Qd = 15, 250 - 250P. a) Find the market supply equation, that...

1. Suppose the market for canola oil is perfectly competitive. There are 1.000 firms in the market, each of which have a fixed cost of FC = 2 and a marginal cost of MC = 1 + q, where q is the quantity produced by an individual firm. Let Q. denote the total quantity supplied in the market. The market demand for canola oil is given by Qd = 15, 250 - 250P. a) Find the market supply equation, that...

1. Assume the market for tortillas is perfectly competitive. The market supply and demand curves for...

1. Assume the market for tortillas is perfectly competitive. The market supply and demand curves for tortillas are given as follows: Supply curve: P = 0.20 Demand curve: P = 1100 – 20 The short-run total cost curve for a typical tortilla factory, ABC, is: TC = 500 + 10 + 4.522 a) Determine the market equilibrium price and quantity. b) Determine the profit-maximizing level of output for factory ABC. c) Assuming that all of the factories are identical, how...

1. Assume the market for tortillas is perfectly competitive. The market supply and demand curves for tortillas are given as follows: Supply curve: P = 0.20 Demand curve: P = 1100 – 20 The short-run total cost curve for a typical tortilla factory, ABC, is: TC = 500 + 10 + 4.522 a) Determine the market equilibrium price and quantity. b) Determine the profit-maximizing level of output for factory ABC. c) Assuming that all of the factories are identical, how...

Suppose you are given the following information about a particular industry: Market demand Market supply QD...

Suppose you are given the following information about a particular industry: Market demand Market supply QD = 14400 - 100P QS = 1500P C(a)=673 + 20 MC(q) = 200 Firm total cost function Firm marginal cost function. Assume that all firms are identical and that the market is characterized by perfect competition. Find the equilibrium price, the equilibrium quantity, the output supplied by the firm, and the profit of each firm. The equilibrium price is $ 9. (Enter your response...

Suppose you are given the following information about a particular industry: Market demand Market supply QD = 14400 - 100P QS = 1500P C(a)=673 + 20 MC(q) = 200 Firm total cost function Firm marginal cost function. Assume that all firms are identical and that the market is characterized by perfect competition. Find the equilibrium price, the equilibrium quantity, the output supplied by the firm, and the profit of each firm. The equilibrium price is $ 9. (Enter your response...

Question 3 (32 marks) a The market of popcom is perfectly competitive. The market demand curve and supply curve are as follows: Demand: Qp = 2000-P Supply: 2 = 1400 +2P Firm K is one of the many firms producing popcorn in the market. The total cost function and marginal cost function are as follows: TC(q) =1250 +30 +29 MC(q) - 30 +49 i At what output level (g) would the average total cost be minimized? (6 marks) ii What...

Question 3 (32 marks) a The market of popcom is perfectly competitive. The market demand curve and supply curve are as follows: Demand: Qp = 2000-P Supply: 2 = 1400 +2P Firm K is one of the many firms producing popcorn in the market. The total cost function and marginal cost function are as follows: TC(q) =1250 +30 +29 MC(q) - 30 +49 i At what output level (g) would the average total cost be minimized? (6 marks) ii What...

(20 marks) Suppose the market for disposable gloves is competitive and it is originally operating at the long run equilibrium. An important raw material of producing disposable gloves is natural rubber. Suppose there is a drastic increase in the price of natural rubber. With the aid of side-by-side diagrams, explain the impacts of the above change on the equilibrium price and equilibrium quantity in the market for disposable gloves, as well as the profit maximizing output level of a typical...

(20 marks) Suppose the market for disposable gloves is competitive and it is originally operating at the long run equilibrium. An important raw material of producing disposable gloves is natural rubber. Suppose there is a drastic increase in the price of natural rubber. With the aid of side-by-side diagrams, explain the impacts of the above change on the equilibrium price and equilibrium quantity in the market for disposable gloves, as well as the profit maximizing output level of a typical...

Question 5 (15 marks) Market demand is given as QD = 120 - P. Market supply is given as QS = 4P. Each identical firm has MC = 6Q and ATC = 3Q. Showing your calculations, answer the following questions: A) What quantity of output will a typical firm produce? (5 marks) B) What is a typical firm's average total cost? (5 marks) C) What is a a typical firm's profit? (5 marks)

Question 5 (15 marks) Market demand is given as QD = 120 - P. Market supply is given as QS = 4P. Each identical firm has MC = 6Q and ATC = 3Q. Showing your calculations, answer the following questions: A) What quantity of output will a typical firm produce? (5 marks) B) What is a typical firm's average total cost? (5 marks) C) What is a a typical firm's profit? (5 marks)

1. Suppose the market for canola oil is perfectly competitive. There are 1.000 firms in the market, each of which have a fixed cost of FC = 2 and a marginal cost of MC = 1 + q, where q is the quantity produced by an individual firm. Let Q. denote the total quantity supplied in the market. The market demand for canola oil is given by Qd = 15, 250 - 250P. a) Find the market supply equation, that...

1. Suppose the market for canola oil is perfectly competitive. There are 1.000 firms in the market, each of which have a fixed cost of FC = 2 and a marginal cost of MC = 1 + q, where q is the quantity produced by an individual firm. Let Q. denote the total quantity supplied in the market. The market demand for canola oil is given by Qd = 15, 250 - 250P. a) Find the market supply equation, that...

1. Assume the market for tortillas is perfectly competitive. The market supply and demand curves for tortillas are given as follows: Supply curve: P = 0.20 Demand curve: P = 1100 – 20 The short-run total cost curve for a typical tortilla factory, ABC, is: TC = 500 + 10 + 4.522 a) Determine the market equilibrium price and quantity. b) Determine the profit-maximizing level of output for factory ABC. c) Assuming that all of the factories are identical, how...

1. Assume the market for tortillas is perfectly competitive. The market supply and demand curves for tortillas are given as follows: Supply curve: P = 0.20 Demand curve: P = 1100 – 20 The short-run total cost curve for a typical tortilla factory, ABC, is: TC = 500 + 10 + 4.522 a) Determine the market equilibrium price and quantity. b) Determine the profit-maximizing level of output for factory ABC. c) Assuming that all of the factories are identical, how...

Suppose you are given the following information about a particular industry: Market demand Market supply QD = 14400 - 100P QS = 1500P C(a)=673 + 20 MC(q) = 200 Firm total cost function Firm marginal cost function. Assume that all firms are identical and that the market is characterized by perfect competition. Find the equilibrium price, the equilibrium quantity, the output supplied by the firm, and the profit of each firm. The equilibrium price is $ 9. (Enter your response...

Suppose you are given the following information about a particular industry: Market demand Market supply QD = 14400 - 100P QS = 1500P C(a)=673 + 20 MC(q) = 200 Firm total cost function Firm marginal cost function. Assume that all firms are identical and that the market is characterized by perfect competition. Find the equilibrium price, the equilibrium quantity, the output supplied by the firm, and the profit of each firm. The equilibrium price is $ 9. (Enter your response...

Most questions answered within 3 hours.

-

For the following reaction, 0.128 moles of

potassium hydrogen sulfateare mixed with

0.504 moles of potassium...

asked 2 hours ago -

1. What is the present value of $400, three years in the future

if the interest...

asked 2 hours ago -

The labor force minus the number of employed equals the number

of unemployed.

a. True

b....

asked 4 hours ago -

Determine the mass in units of grams [g] of 0.49 moles [mol]

of a new fictitious...

asked 5 hours ago -

A horizontal mass of M=5kg is on a spring and stretched to

x=0.5m when released from...

asked 6 hours ago -

26 of 50

"I have worked at the Arizona Humane Society for ten years, and

have...

asked 6 hours ago -

Compare and contrast zero based budgeting and incremental (or

base year) budgeting.

asked 6 hours ago -

4 pts 10. Which of the following hypothesis would be MOST

difficult to test experimentally? Group...

asked 6 hours ago -

A business owner makes 1,000 items a day. Each day he or she

contributes eight hours...

asked 6 hours ago -

A

circular loop in the plane of a paper lies inca0.65 T magnetic

field pointing into...

asked 7 hours ago -

A business owner is trying to decide whether to buy, rent, or

lease office space and...

asked 7 hours ago -

Thermal Storage Solar heating of a house is much more efficient

if there is a way...

asked 7 hours ago