Homework Answers

2. To calculate the 2-year interest rate and 3-year interest rate, we will use the below formula -

[ {1 + r (n+1)}^(n+1) / (1 + rn)^n] - 1

Plugging in the values, 2-year interest rate =

{(1+2%)^2 / (1+3%)^1} - 1

= {(1 + 0.02)^2 / (1 + 0.03)^1} - 1

= (1.02^2 / 1.03) - 1

= 1.0404 / 1.03 - 1

= 1.01 - 1

= 0.01

= 1%

Similarly, 3-year interest rate =

{(1 + 4%)^3 / (1 + 2%)^2} - 1

= (1.04^3 / 1.02^2) - 1

= (1.124864 / 1.0404) - 1

= 1.0811 - 1

= 0.0811

= 8%

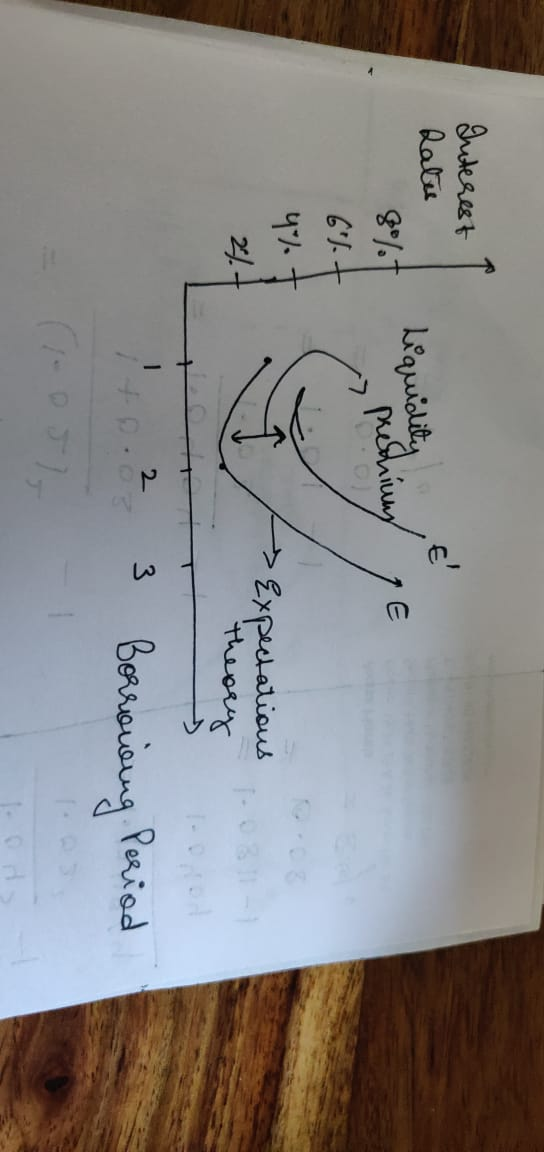

b. Yield curve -

c) Liquidity Premium

d) In the next two years, the interest rate is falling to 1% according to expectations theory. In general, a fall in interest rates would mean that borrowing is cheap and people will borrow more and have more money. Thus, they will spend more on goods and services, consumption would go up, and it would lead to an increase in inflation.

In the next three years, the interest rate is rising to 8% according to expectations theory. In general, a rise in interest rates would mean that borrowing is expensive and people will borrow less. Thus, consumption will fall and it would lead to a fall in inflation. But, because of higher interest rates, savings would increase.

Add Answer to:

3. Assume that the current 1-year interest rate is 3%, the expected 1-year rate next year...

5. Assume the following interest rates Current Rate on a 1-year bond due in 2019: 4% Expected Rate on a 1-year bond due in 2020: 5% Expected Rate on a 1-year bond due in 2021: 6% Expected Rate on a 1-...

5. Assume the following interest rates Current Rate on a 1-year bond due in 2019: 4% Expected Rate on a 1-year bond due in 2020: 5% Expected Rate on a 1-year bond due in 2021: 6% Expected Rate on a 1-year bond due in 2022: 4% Expected Rate on a 1-year bond due in 2023: 2% a. According to the expectations theory for the yield curve, what would be the current rate on a 3-year bond due in 2021? Show...

5a. Assume that the one-year interest rate is 1%, the two-year interest rate is 2% and...

5a. Assume that the one-year interest rate is 1%, the two-year interest rate is 2% and the three-year interest rate is 2%. What is the expected one-year interest rate a year from now, and two years from, according to the expectations theory? b. Assume that the one-year interest rate is 1%, the two-year interest rate is 2%, the three-year interest rate is 2%, the liquidity premium for two-year interest rates is 0.3%. and the liquidity premium for three-year interest rates...

2. EXPECTED INTEREST RATE The real risk-free rate is 3%. Inflation is expected to be 2% this year and 4% during the next 2 years. Assume that the maturity risk premium is zero. What is the yield o...

2. EXPECTED INTEREST RATE The real risk-free rate is 3 %. Inflation is expected to be 2 % this year and 4 % during the next 2 years. Assume that the maturity risk premium is zero. What is the yield on 2-year Treasury securities? What is the yield on 3 -year Treasury securities?3. MATURITY RISK PREMIUM The real risk-free rate is 3 %, and inflation is expected to be 3 % for the next 2 years. A 2-year Treasury security...

The real risk-free rate of interest is expected to remain constant at 3% for the foreseeable...

The real risk-free rate of interest is expected to remain constant at 3% for the foreseeable future. However, inflation is expected to increase steadily over the next 30 years, so the Treasury yield curve has an upward slope. Assume that the pure expectations theory holds. You are also considering two corporate bonds, one with a 3-year maturity and one with a 5-year maturity. Both have the same default and liquidity risks. Given these assumptions, which of these statements is CORRECT?...

Suppose interest rates on 1 year bonds are expected to be 0.6%, 0.7%,0.7% 0.8% and 0.8%...

Suppose interest rates on 1 year bonds are expected to be 0.6%, 0.7%,0.7% 0.8% and 0.8% over the next five years. Suppose the liquidity premium on five year bonds is 0.2% a. Using the expectations theory, what would be the interest rate on a five year bond? b. Using the liquidity premium theory, what would be the interest rate on a five year bond? Print Layout view Sec 1 Pages: 3 of 3

Suppose interest rates on 1 year bonds are expected to be 0.6%, 0.7%,0.7% 0.8% and 0.8% over the next five years. Suppose the liquidity premium on five year bonds is 0.2% a. Using the expectations theory, what would be the interest rate on a five year bond? b. Using the liquidity premium theory, what would be the interest rate on a five year bond? Print Layout view Sec 1 Pages: 3 of 3

b. Assume that the one-year interest rate is 1%, the two-year interest rate is 2%, the...

b. Assume that the one-year interest rate is 1%, the two-year interest rate is 2%, the three-year interest rate is 2%, the liquidity premium for two-year interest rates is 0.3%. and the liquidity premium for three-year interest rates is 0.4%. What is the expected one-year interest rate a year from now according to the liquidity premium theory?

The real risk-free rate, r*, is expected to remain constant at 3% per year. Inflation is expected...

The real risk-free rate, r*, is expected to remain constant at 3% per year. Inflation is expected to be 2% per year forever. Assume that the expectations theory holds; that is, there is no maturity risk premium. Treasury securities do not require any default risk or liquidity premiums. Which of the following is most correct? The Treasury yield curve is flat and all Treasury securities yield 5%. The Treasury yield curve is upward sloping for the first 10 years, and then downward sloping....

Assume that the real interest rate is 2%, the default risk premium is 3%, the liquidity...

Assume that the real interest rate is 2%, the default risk premium is 3%, the liquidity premium is 1%, and the maturity risk premium is 1% per year. Additional, the expected inflation rate is 3% next year, 1% the year after, and 10% from then on. What are the nominal interest rates for: a) 1-year note? b) 5-year note? c) does this produce an inverted yield curve? Why or why not? Please show all work!

The real risk-free rate of interest is expected to remain constant at 2.5% for the foreseeable...

The real risk-free rate of interest is expected to remain constant at 2.5% for the foreseeable future. However, inflation is expected to increase steadily over the next 30 years, so the Treasury yield curve has an upward slope. Assume that the pure expectations theory holds. You are also considering two corporate bonds, one with a 3-year maturity and one with a 5-year maturity. Both have the same default and liquidity risks. Given these assumptions, which of these statements is CORRECT?...

QUESTION 13 Assume that 1-year T-bills currently yield 5.00% and the future inflation rate is expected...

QUESTION 13 Assume that 1-year T-bills currently yield 5.00% and the future inflation rate is expected to be constant at 2.0% per year. What is the real risk-free rate of return, r"? 6.50% 5.00% 4 50% 4004 3.00% QUESTION 14 Suppose 10-year T-bonds have a yield of 4.00% and 10-year corporate bonds yield 6.50%. Also, corporate bonds have a 0.50% liquidity premium versus a zero iquidity premium for T-bonds, and the maturity risk premium on both Treasury and corporate 10-year...

QUESTION 13 Assume that 1-year T-bills currently yield 5.00% and the future inflation rate is expected to be constant at 2.0% per year. What is the real risk-free rate of return, r"? 6.50% 5.00% 4 50% 4004 3.00% QUESTION 14 Suppose 10-year T-bonds have a yield of 4.00% and 10-year corporate bonds yield 6.50%. Also, corporate bonds have a 0.50% liquidity premium versus a zero iquidity premium for T-bonds, and the maturity risk premium on both Treasury and corporate 10-year...

Suppose interest rates on 1 year bonds are expected to be 0.6%, 0.7%,0.7% 0.8% and 0.8% over the next five years. Suppose the liquidity premium on five year bonds is 0.2% a. Using the expectations theory, what would be the interest rate on a five year bond? b. Using the liquidity premium theory, what would be the interest rate on a five year bond? Print Layout view Sec 1 Pages: 3 of 3

Suppose interest rates on 1 year bonds are expected to be 0.6%, 0.7%,0.7% 0.8% and 0.8% over the next five years. Suppose the liquidity premium on five year bonds is 0.2% a. Using the expectations theory, what would be the interest rate on a five year bond? b. Using the liquidity premium theory, what would be the interest rate on a five year bond? Print Layout view Sec 1 Pages: 3 of 3

QUESTION 13 Assume that 1-year T-bills currently yield 5.00% and the future inflation rate is expected to be constant at 2.0% per year. What is the real risk-free rate of return, r"? 6.50% 5.00% 4 50% 4004 3.00% QUESTION 14 Suppose 10-year T-bonds have a yield of 4.00% and 10-year corporate bonds yield 6.50%. Also, corporate bonds have a 0.50% liquidity premium versus a zero iquidity premium for T-bonds, and the maturity risk premium on both Treasury and corporate 10-year...

QUESTION 13 Assume that 1-year T-bills currently yield 5.00% and the future inflation rate is expected to be constant at 2.0% per year. What is the real risk-free rate of return, r"? 6.50% 5.00% 4 50% 4004 3.00% QUESTION 14 Suppose 10-year T-bonds have a yield of 4.00% and 10-year corporate bonds yield 6.50%. Also, corporate bonds have a 0.50% liquidity premium versus a zero iquidity premium for T-bonds, and the maturity risk premium on both Treasury and corporate 10-year...

Most questions answered within 3 hours.

-

What are the negative effects of abruptly stopping the use of

all fossil fuels? Give at...

asked 4 minutes ago -

Given that many conflict are the result of different parties having

different interests, is it possible...

asked 9 minutes ago -

A 750 g block can slide uniformly along the horizontal track

when a string attached to...

asked 12 minutes ago -

In 2017, Juan entered into a contract to write a book. The

publisher advanced Juan $50,000,...

asked 25 minutes ago -

Determine the number of kinds of protons in each molecule (w/

respect to NMR spectroscopy). Drawing...

asked 35 minutes ago -

A jeweler whose near point is 68 cm from his eye uses a

magnifying glass as...

asked 33 minutes ago -

A company wants to determine how many units of each of two

products, A and B,...

asked 37 minutes ago -

The blood pressure of a person changes throughout the day.

Suppose the systolic blood pressure of...

asked 46 minutes ago -

A chemistry student desired to study sulfur. Sulfur exhibited

the following characteristics with oxygen:

(a) It...

asked 42 minutes ago -

An Atwood machine is constructed of a solid-disk frictionless

pulley of mass m3 and radius R....

asked 44 minutes ago -

what are the advantages of lanthanum hexaboride over tungsten

filament for electron emission

what is the...

asked 45 minutes ago -

Question 5

Your uncle offers to sell you his vintage Rolls Royce. He

suggests a payment...

asked 50 minutes ago