Dave LaCroix recently received a 10 percent capital and profits interest in Cirque Capital LLC in...

Dave LaCroix recently received a 10 percent capital and profits interest in Cirque Capital LLC in exchange for consulting services he provided. If Cirque Capital had paid an outsider to provide the advice, it would have deducted the payment as compensation expense. Cirque Capital’s balance sheet on the day Dave received his capital interest appears below:

| Basis | Fair Market Value |

||||

| Assets: | |||||

| Cash | $ | 210,000 | $ | 210,000 | |

| Investments | 100,000 | 126,000 | |||

| Land | 290,000 | 420,000 | |||

| Totals | $ | 600,000 | $ | 756,000 | |

| Liabilities and capital: | |||||

| Nonrecourse Debt | $ | 230,000 | $ | 230,000 | |

| Lance* | 185,000 | 263,000 | |||

| Robert* | 185,000 | 263,000 | |||

| Totals | $ | 600,000 | $ | 756,000 | |

*Assume that Lance’s basis and Robert’s basis in their LLC interests equal their tax basis capital accounts plus their respective shares of nonrecourse debt. (Leave no answer blank. Enter zero if applicable.)

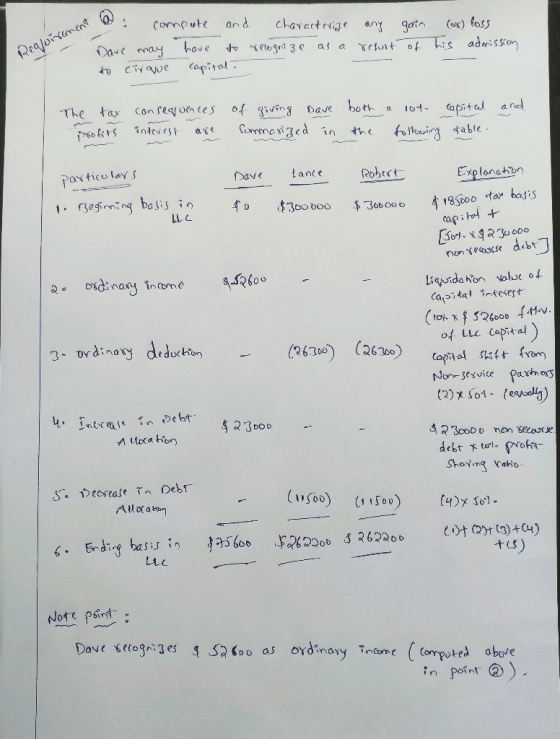

a. Compute and characterize any gain or loss Dave may have to recognize as a result of his admission to Cirque Capital.

Answer is complete but not entirely correct.

|

b. Compute each member’s tax basis in his LLC interest immediately after Dave’s receipt of his interest.

|

c. Prepare a balance sheet for Cirque Capital immediately after Dave’s admission showing the members’ tax capital accounts and their capital accounts stated at fair market value.

|

|||||||||||||||||||||||||||||||||||||||||||

d. Compute and characterize any gain or loss Dave may have to recognize as a result of his admission to Cirque Capital if he receives only a profits interest.

|

e. Compute each member’s tax basis in his LLC interest immediately after Dave’s receipt of his interest if Dave receives only a profits interest.

|

Homework Answers

Refer to the below images for the above asked questions, in a detailed way of solution with calculations and explanations.

Add Answer to:

Dave LaCroix recently received a 10 percent capital and profits

interest in Cirque Capital LLC in...

On January 1, X9, Gerald received his 50% profits and capital interest in High Air, LLC...

On January 1, X9, Gerald received his 50% profits and capital interest in High Air, LLC in exchange for $3,500 in cash and real property with a $4,500 tax basis secured by a $3,500 nonrecourse mortgage. High Air reported a $16,500 loss for its X9 calendar year. How much loss can Gerald deduct, and how much loss must he suspend if he only applies the tax basis loss limitation?

On January 1, X9, Gerald received his 50 percent profits and capital interest in High Air,...

On January 1, X9, Gerald received his 50 percent profits and capital interest in High Air, LLC, in exchange for $2,700 in cash and real property with a $3,700 tax basis secured by a $2,700 nonrecourse mortgage. High Air reported a $15,700 loss for its X9 calendar year. How much loss can Gerald deduct, and how much loss must he suspend if he only applies the tax basis loss limitation?

Kevan, Jerry, and Dave formed Albee LLC. Jerry and Dave each contributed $245,000 in cash. Kevan...

Kevan, Jerry, and Dave formed Albee LLC. Jerry and Dave each contributed $245,000 in cash. Kevan contributed the following assets: Basis Fair Market Value Kevan: Cash $ 15,000 $ 15,000 Land* 120,000 440,000 Totals $ 135,000 $ 455,000 *Nonrecourse debt secured by the land equals $210,000 Each member received a one-third capital and profits interest in the LLC. (Leave no answer blank. Enter zero if applicable. Do not round intermediate calculations.)

Connie recently provided legal services to the Winterhaven LLC and received a 5 percent interest in...

Connie recently provided legal services to the Winterhaven LLC

and received a 5 percent interest in the LLC as compensation.

Winterhaven currently has $35,000 of accounts payable and no other

debt. The current fair market value of Winterhaven’s capital is

$300,000. (Leave no answer blank. Enter zero if

applicable.)

a. If Connie receives a 5 percent capital

interest only, how much income must she report and what is her tax

basis in the LLC interest?

b. If Connie receives a...

Connie recently provided legal services to the Winterhaven LLC

and received a 5 percent interest in the LLC as compensation.

Winterhaven currently has $35,000 of accounts payable and no other

debt. The current fair market value of Winterhaven’s capital is

$300,000. (Leave no answer blank. Enter zero if

applicable.)

a. If Connie receives a 5 percent capital

interest only, how much income must she report and what is her tax

basis in the LLC interest?

b. If Connie receives a...

Connie recently provided legal services to the Winterhaven LLC and received a 5 percent interest in...

Connie recently provided legal services to the Winterhaven LLC and received a 5 percent interest in the LLC as compensation. Winterhaven currently has $52,000 of accounts payable and no other debt. The current fair market value of Winterhaven’s capital is $200,000. If Connie receives a 5 percent capital and profits interest, how much income must she report and what is her tax basis in the LLC interest?

Tom is talking to his friend Bob, who has an interest in Freedom, LLC. about purchasing...

Tom is talking to his friend Bob, who has an interest in Freedom, LLC. about purchasing his LLC interest. Bob's outside basis in Freedom, LLC is $15.000. This includes his $3.500 one-fourth share of the LLC's debt. Bob's 704(6) capital account is $22.000. If Tom bought Bob's LLC interest for $27,000, what would Tom's outside basis be in Freedom, LLC? Multiple Choice $15.000 O $23.500 O $27,000 O $30,500 Erica and Brett decide to form their new motorcycle business as...

Tom is talking to his friend Bob, who has an interest in Freedom, LLC. about purchasing his LLC interest. Bob's outside basis in Freedom, LLC is $15.000. This includes his $3.500 one-fourth share of the LLC's debt. Bob's 704(6) capital account is $22.000. If Tom bought Bob's LLC interest for $27,000, what would Tom's outside basis be in Freedom, LLC? Multiple Choice $15.000 O $23.500 O $27,000 O $30,500 Erica and Brett decide to form their new motorcycle business as...

Kim received a 1/3 profits and capital interest in Bright Line, LLC in exchange for legal...

Kim received a 1/3 profits and capital interest in Bright Line, LLC in exchange for legal services she provided. In addition to her share of partnership profits or losses, she receives a $30,000 guaranteed payment each year for ongoing services she provides to the LLC. For X4, Bright Line reported the following revenues and expenses: Sales $150,000, Cost of Goods Sold $90,000, Depreciation Expense $12,000, Long-Term Capital Gains $15,000, Qualified Dividends $6,000, and Municipal Bond Interest $3,000. How much ordinary...

Kim received a 1/3 profits and capital interest in Bright Line, LLC in exchange for legal services she provided. In addition to her share of partnership profits or losses, she receives a $30,000 guaranteed payment each year for ongoing services she provides to the LLC. For X4, Bright Line reported the following revenues and expenses: Sales $150,000, Cost of Goods Sold $90,000, Depreciation Expense $12,000, Long-Term Capital Gains $15,000, Qualified Dividends $6,000, and Municipal Bond Interest $3,000. How much ordinary...

Kim received a 1/3 profits and capital interest in Bright Line. LLC in exchange for legal...

Kim received a 1/3 profits and capital interest in Bright Line. LLC in exchange for legal services she provided. In addition to her share of partnership profits or losses, she receives a $35.000 guaranteed payment each year for ongoing services she provides to the LLC. For X4. Bright Line reported the following revenues and expenses: Sales - $155,000. Cost of Goods Sold - $95.000. Depreciation Expense - $52.000. Long-Term Capital Gains - $20.000. Qualified Dividends - $6.500, and Municipal Bond...

Kim received a 1/3 profits and capital interest in Bright Line. LLC in exchange for legal services she provided. In addition to her share of partnership profits or losses, she receives a $35.000 guaranteed payment each year for ongoing services she provides to the LLC. For X4. Bright Line reported the following revenues and expenses: Sales - $155,000. Cost of Goods Sold - $95.000. Depreciation Expense - $52.000. Long-Term Capital Gains - $20.000. Qualified Dividends - $6.500, and Municipal Bond...

In a proportionate current (nonliquidating) distribution of his 30% interest in the MNO LLC, Neil received cash ($60,000), land (basis of $40,000 and value of $75,000), and unrealized receivables (ba...

In a proportionate current (nonliquidating) distribution of his 30% interest in the MNO LLC, Neil received cash ($60,000), land (basis of $40,000 and value of $75,000), and unrealized receivables (basis of $0 and value of $22,000). In addition, Neil is relieved of his $40,000 share of the LLC’s liabilities. Neil’s basis in MNO (including his share of LLC liabilities) was $80,000 immediately prior to this distribution. a. How much gain or loss does Neil recognize on this distribution? b. What...

Styling Shoes, LLC filed its 20X8 Form 1065 on March 15, 20X9. Styling had three members...

Styling Shoes, LLC filed its 20X8 Form 1065 on March 15, 20X9. Styling had three members with the following ownership interests and tax basis at the beginning of the 20X8: (1) Jane, a member with a 25% profits and capital interest and a $11.500 outside basis. (2) Joe, a member with a 45% profits and capital interest and a $16,500 outside basis, and (3) Jack, a member with a 30% profits and capital interest and a $8.500 outside basis. The...

Styling Shoes, LLC filed its 20X8 Form 1065 on March 15, 20X9. Styling had three members with the following ownership interests and tax basis at the beginning of the 20X8: (1) Jane, a member with a 25% profits and capital interest and a $11.500 outside basis. (2) Joe, a member with a 45% profits and capital interest and a $16,500 outside basis, and (3) Jack, a member with a 30% profits and capital interest and a $8.500 outside basis. The...

Connie recently provided legal services to the Winterhaven LLC

and received a 5 percent interest in the LLC as compensation.

Winterhaven currently has $35,000 of accounts payable and no other

debt. The current fair market value of Winterhaven’s capital is

$300,000. (Leave no answer blank. Enter zero if

applicable.)

a. If Connie receives a 5 percent capital

interest only, how much income must she report and what is her tax

basis in the LLC interest?

b. If Connie receives a...

Connie recently provided legal services to the Winterhaven LLC

and received a 5 percent interest in the LLC as compensation.

Winterhaven currently has $35,000 of accounts payable and no other

debt. The current fair market value of Winterhaven’s capital is

$300,000. (Leave no answer blank. Enter zero if

applicable.)

a. If Connie receives a 5 percent capital

interest only, how much income must she report and what is her tax

basis in the LLC interest?

b. If Connie receives a...

Tom is talking to his friend Bob, who has an interest in Freedom, LLC. about purchasing his LLC interest. Bob's outside basis in Freedom, LLC is $15.000. This includes his $3.500 one-fourth share of the LLC's debt. Bob's 704(6) capital account is $22.000. If Tom bought Bob's LLC interest for $27,000, what would Tom's outside basis be in Freedom, LLC? Multiple Choice $15.000 O $23.500 O $27,000 O $30,500 Erica and Brett decide to form their new motorcycle business as...

Tom is talking to his friend Bob, who has an interest in Freedom, LLC. about purchasing his LLC interest. Bob's outside basis in Freedom, LLC is $15.000. This includes his $3.500 one-fourth share of the LLC's debt. Bob's 704(6) capital account is $22.000. If Tom bought Bob's LLC interest for $27,000, what would Tom's outside basis be in Freedom, LLC? Multiple Choice $15.000 O $23.500 O $27,000 O $30,500 Erica and Brett decide to form their new motorcycle business as...

Kim received a 1/3 profits and capital interest in Bright Line, LLC in exchange for legal services she provided. In addition to her share of partnership profits or losses, she receives a $30,000 guaranteed payment each year for ongoing services she provides to the LLC. For X4, Bright Line reported the following revenues and expenses: Sales $150,000, Cost of Goods Sold $90,000, Depreciation Expense $12,000, Long-Term Capital Gains $15,000, Qualified Dividends $6,000, and Municipal Bond Interest $3,000. How much ordinary...

Kim received a 1/3 profits and capital interest in Bright Line, LLC in exchange for legal services she provided. In addition to her share of partnership profits or losses, she receives a $30,000 guaranteed payment each year for ongoing services she provides to the LLC. For X4, Bright Line reported the following revenues and expenses: Sales $150,000, Cost of Goods Sold $90,000, Depreciation Expense $12,000, Long-Term Capital Gains $15,000, Qualified Dividends $6,000, and Municipal Bond Interest $3,000. How much ordinary...

Kim received a 1/3 profits and capital interest in Bright Line. LLC in exchange for legal services she provided. In addition to her share of partnership profits or losses, she receives a $35.000 guaranteed payment each year for ongoing services she provides to the LLC. For X4. Bright Line reported the following revenues and expenses: Sales - $155,000. Cost of Goods Sold - $95.000. Depreciation Expense - $52.000. Long-Term Capital Gains - $20.000. Qualified Dividends - $6.500, and Municipal Bond...

Kim received a 1/3 profits and capital interest in Bright Line. LLC in exchange for legal services she provided. In addition to her share of partnership profits or losses, she receives a $35.000 guaranteed payment each year for ongoing services she provides to the LLC. For X4. Bright Line reported the following revenues and expenses: Sales - $155,000. Cost of Goods Sold - $95.000. Depreciation Expense - $52.000. Long-Term Capital Gains - $20.000. Qualified Dividends - $6.500, and Municipal Bond...

Styling Shoes, LLC filed its 20X8 Form 1065 on March 15, 20X9. Styling had three members with the following ownership interests and tax basis at the beginning of the 20X8: (1) Jane, a member with a 25% profits and capital interest and a $11.500 outside basis. (2) Joe, a member with a 45% profits and capital interest and a $16,500 outside basis, and (3) Jack, a member with a 30% profits and capital interest and a $8.500 outside basis. The...

Styling Shoes, LLC filed its 20X8 Form 1065 on March 15, 20X9. Styling had three members with the following ownership interests and tax basis at the beginning of the 20X8: (1) Jane, a member with a 25% profits and capital interest and a $11.500 outside basis. (2) Joe, a member with a 45% profits and capital interest and a $16,500 outside basis, and (3) Jack, a member with a 30% profits and capital interest and a $8.500 outside basis. The...

Most questions answered within 3 hours.

-

Need help with 1 and 2.

My brains fried for studying for midterm. It would be...

asked 12 seconds ago -

The P-value for a hypothesis test is given. Determine whether

the strength of the evidence against...

asked 6 minutes ago -

Q 1) what is the Oman vision 2020?

(Most important plan, improvement, diversification)

Q 2) Discuss...

asked 28 minutes ago -

Brooklyn has been contributing to a traditional IRA for seven

years (all deductible contributions) and has...

asked 26 minutes ago -

4. Consider the lowest three energy levels of hydrogen?

a. What emission transitions are possible?

b....

asked 42 minutes ago -

Describe an example for one of the "Four Steps to Persuade a

Workplace" to embrace and...

asked 43 minutes ago -

If you were to use war as a metaphor to think about the immune

response and...

asked 1 hour ago -

presentation on computers and stresses

i need data how computers create stress. how the are

combined...

asked 1 hour ago -

Genetic Variation

Explain three cellular and /or molecular mechanisms

that introduce variation into the gene pool...

asked 1 hour ago -

Carmelita Inc., has the following information available:

Costs from Beginning Inventory

Costs from current Period

Direct...

asked 1 hour ago -

There are four steps to algorithm methodology.

1. Design: Identify the problem and thoroughly

understand it....

asked 1 hour ago -

It is known that The New York Times’ circulation is 731,500

print copies. You publish three...

asked 1 hour ago