Homework Answers

c)

First, I will assume I have dataset of dependent variables Yi, and independent variables X1i, X2i, X3i,... Xki.

Then, I will fit a linear regression model to that dataset: Y=a + bX1 + Z + e, where Z is a linear combination of all the independent variables from X2 onwards: Z=cX2+dX3+... Z is therefore independent of a and b.

After the model is fitted, i.e. the parameters a, b, c, d... are determined, so that the sum of square of the errors s(a,b,c,d...) = Ʃei^2 = Ʃ(Yi-a-bX1i-Zi)^2 is minimized.

For this, I calculate the partial derivatives of s for a,b,c,d.... and set them to equal 0.

I find that ∂s/∂a = -2 Ʃ(Yi-a-bX1i-Zi). Therefore Ʃ(Yi-a-bX1i-Zi) = Ʃei = 0, and E[e]=e~= 0

∂s/∂b = -2 Ʃ X1i (Yi-a-bX1i-Zi). Therefore Ʃ X1i (Yi-a-bX1i-Zi) = Ʃ X1i ei= 0

Then, Ʃ (ei-e~)(X1i-X1~) = Ʃ (eiX1i - eiX1~ - e~X1i + e~X1~) = ƩeiX1i - ƩeiX1~ - Ʃe~X1i + Ʃe~X1~ = 0 - X1~Ʃei -Ʃ0 + Ʃ0 = -X1~0 = 0 Therefore Cov(e,X1) = 0, which is what I wanted to prove.

X1 is replacable with any of the other X:s that are all combined in Z, and repeat the above analysis. Because the regression function is symmetric for all the predictor variables, I would then find that cov(e,Xk)=0 for any k.

Add Answer to:

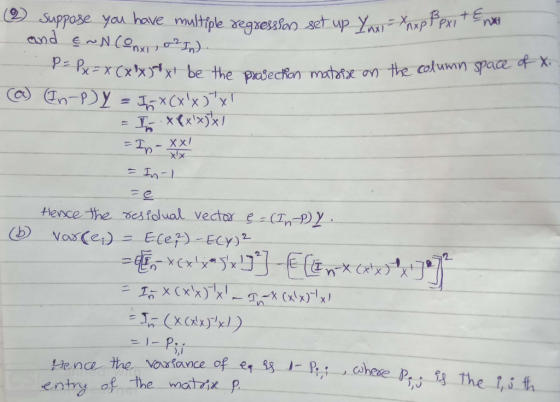

2) Suppose you have multiple regression set up Ynxi XnxpBpxi Sxl and f ~ N(0nx1, σ21.). P Po X(X,...

Considering multiple linear regression models, we compute the regression of Y, an n x 1 vector,...

Considering multiple linear regression models, we compute the regression of Y, an n x 1 vector, on an n x (p+1) full rank matrix X. As usual, H = X(XT X)-1 XT is the hat matrix with elements hij at the ith row and jth column. The residual is e; = yi - Ýi. (a) (7 points) Let Y be an n x 1 vector with 1 as its first element and Os elsewhere. Show that the elements of the...

Considering multiple linear regression models, we compute the regression of Y, an n x 1 vector, on an n x (p+1) full rank matrix X. As usual, H = X(XT X)-1 XT is the hat matrix with elements hij at the ith row and jth column. The residual is e; = yi - Ýi. (a) (7 points) Let Y be an n x 1 vector with 1 as its first element and Os elsewhere. Show that the elements of the...

Considering multiple linear regression models, we compute the regression of Y, an n x 1 vector,...

Considering multiple linear regression models, we compute the regression of Y, an n x 1 vector, on an n x (p+1) full rank matrix X. As usual, H = X(XT X)-1 XT is the hat matrix with elements hij at the ith row and jth column. The residual is e; = yi - Ýi. (a) (7 points) Let Y be an n x 1 vector with 1 as its first element and Os elsewhere. Show that the elements of the...

Considering multiple linear regression models, we compute the regression of Y, an n x 1 vector, on an n x (p+1) full rank matrix X. As usual, H = X(XT X)-1 XT is the hat matrix with elements hij at the ith row and jth column. The residual is e; = yi - Ýi. (a) (7 points) Let Y be an n x 1 vector with 1 as its first element and Os elsewhere. Show that the elements of the...

3. In the usual setup for multiple regression, e, hi, Vo) are the raw residual, leverage, and the...

3. In the usual setup for multiple regression, e, hi, Vo) are the raw residual, leverage, and the i-th leave-one-out fitted response, respectively. The i-th deleted residual sum of square is defined as where yo: (n-1)x1, the response vector with the i-th entry deleted; Xo): (n-1) x p is the design matrix with the i-th row deleted (a) (Stat438 ONLY) Show that SSRestSSRes-_ by using the following results SS Res e2 SSRes (b) Use the result from (a), show that...

3. In the usual setup for multiple regression, e, hi, Vo) are the raw residual, leverage, and the i-th leave-one-out fitted response, respectively. The i-th deleted residual sum of square is defined as where yo: (n-1)x1, the response vector with the i-th entry deleted; Xo): (n-1) x p is the design matrix with the i-th row deleted (a) (Stat438 ONLY) Show that SSRestSSRes-_ by using the following results SS Res e2 SSRes (b) Use the result from (a), show that...

linear stat modeling & regression please , i need the solution for Q3, but i copy Q2 because you need info from Q2 in order to answer Q3. 2) Suppose you have multiple regression set up YxXB...

linear stat modeling & regression

please ,

i need the solution for Q3, but i copy Q2 because you need

info from Q2 in order to answer Q3.

2) Suppose you have multiple regression set up YxXBp The ridge regression estimator is given by Here, llell'-Σ.< where is a vector of Vik. a) Find the expectation and variance-covariance matrix of Bridge, when X'X is a diagonal matrix with each diagonal entry is eqal to. Com pare these variances with the...

linear stat modeling & regression

please ,

i need the solution for Q3, but i copy Q2 because you need

info from Q2 in order to answer Q3.

2) Suppose you have multiple regression set up YxXBp The ridge regression estimator is given by Here, llell'-Σ.< where is a vector of Vik. a) Find the expectation and variance-covariance matrix of Bridge, when X'X is a diagonal matrix with each diagonal entry is eqal to. Com pare these variances with the...

3. In the multiple regression model shown in the previous question, which one of the following st...

3. In the multiple regression model shown in the previous question, which one of the following statements is incorrect: (b) The sum of squared residuals is the square of the length of the vector ü (c) The residual vector is orthogonal to each of the columns of X (d) The square of the length of y is equal to the square of the length of y plus the square of the length of û by the Pythagoras theorem In all...

3. In the multiple regression model shown in the previous question, which one of the following statements is incorrect: (b) The sum of squared residuals is the square of the length of the vector ü (c) The residual vector is orthogonal to each of the columns of X (d) The square of the length of y is equal to the square of the length of y plus the square of the length of û by the Pythagoras theorem In all...

In the context of multiple regression, define the n X n matrix M =- X(X'X)-'X'. (i)...

In the context of multiple regression, define the n X n matrix M =- X(X'X)-'X'. (i) Show that M is symmetric and idempotent. (ii) Prove that m, the diagonals of the matrix M, satisfy 0 sm s 1 for t = 1, 2, ..., n. (iii) Consider the linear model y = XB + u satisfies the Gauss-Markov Assumptions. Let û be the vector of OLS residuals. Show that Eſûù' x) = oʻM (iv) Conclude that while the errors {u:...

In the context of multiple regression, define the n X n matrix M =- X(X'X)-'X'. (i) Show that M is symmetric and idempotent. (ii) Prove that m, the diagonals of the matrix M, satisfy 0 sm s 1 for t = 1, 2, ..., n. (iii) Consider the linear model y = XB + u satisfies the Gauss-Markov Assumptions. Let û be the vector of OLS residuals. Show that Eſûù' x) = oʻM (iv) Conclude that while the errors {u:...

In the context of multiple regression, define the n X n matrix M =- X(X'X)-'X'. (i)...

In the context of multiple regression, define the n X n matrix M =- X(X'X)-'X'. (i) Show that M is symmetric and idempotent. (ii) Prove that m, the diagonals of the matrix M, satisfy 0 sm s 1 for t = 1, 2, ..., n. (iii) Consider the linear model y = XB + u satisfies the Gauss-Markov Assumptions. Let û be the vector of OLS residuals. Show that Eſûù' x) = oʻM (iv) Conclude that while the errors {u:...

In the context of multiple regression, define the n X n matrix M =- X(X'X)-'X'. (i) Show that M is symmetric and idempotent. (ii) Prove that m, the diagonals of the matrix M, satisfy 0 sm s 1 for t = 1, 2, ..., n. (iii) Consider the linear model y = XB + u satisfies the Gauss-Markov Assumptions. Let û be the vector of OLS residuals. Show that Eſûù' x) = oʻM (iv) Conclude that while the errors {u:...

4. We have n statistical units. For unit i, we have (xi; yi), for i-1,2,... ,n. We used the least squares line to obtain the estimated regression line у = bo +biz. (a) Show that the centroid (x, y) i...

4. We have n statistical units. For unit i, we have (xi; yi), for i-1,2,... ,n. We used the least squares line to obtain the estimated regression line у = bo +biz. (a) Show that the centroid (x, y) is a point on the least squares line, where x = (1/n) and у = (1/n) Σ¡ı yi. (Hint: E ) i-1 valuate the line at x = x. (b) In the suggested exercises, we showed that e,-0 and e-0, where...

4. We have n statistical units. For unit i, we have (xi; yi), for i-1,2,... ,n. We used the least squares line to obtain the estimated regression line у = bo +biz. (a) Show that the centroid (x, y) is a point on the least squares line, where x = (1/n) and у = (1/n) Σ¡ı yi. (Hint: E ) i-1 valuate the line at x = x. (b) In the suggested exercises, we showed that e,-0 and e-0, where...

1.Given the Multiple Linear regression model as Y-Po + β.X1 + β2X2 + β3Xs + which in matrix notation is written asy-xß +ε where -έ has a N(0,a21) distribution + + ßpXo +ε A. Show that the OLS estimat...

1.Given the Multiple Linear regression model as Y-Po + β.X1 + β2X2 + β3Xs + which in matrix notation is written asy-xß +ε where -έ has a N(0,a21) distribution + + ßpXo +ε A. Show that the OLS estimator of the parameter vector B is given by B. Show that the OLS in A above is an unbiased estimator of β Hint: E(β)-β C. Show that the variance of the estimator is Var(B)-o(Xx)-1 D. What is the distribution o the...

1.Given the Multiple Linear regression model as Y-Po + β.X1 + β2X2 + β3Xs + which in matrix notation is written asy-xß +ε where -έ has a N(0,a21) distribution + + ßpXo +ε A. Show that the OLS estimator of the parameter vector B is given by B. Show that the OLS in A above is an unbiased estimator of β Hint: E(β)-β C. Show that the variance of the estimator is Var(B)-o(Xx)-1 D. What is the distribution o the...

e. Consider the multiple regression model y X 3+E. with E(e)-0 and var (e) ơ21 Assume that ε ~ N(0 σ21), when we test the hypothesis Ho : βί-0 against Ha : βί 0 we use the t statistic with n-k-1 degr...

e. Consider the multiple regression model y X 3+E. with E(e)-0 and var (e) ơ21 Assume that ε ~ N(0 σ21), when we test the hypothesis Ho : βί-0 against Ha : βί 0 we use the t statistic with n-k-1 degrees of freedom. When Ho is not true find the expected value and variance of the test onsider the genera -~ 0 gains 0 1S not true find the expected value and variance of the test statistic.

e. Consider...

e. Consider the multiple regression model y X 3+E. with E(e)-0 and var (e) ơ21 Assume that ε ~ N(0 σ21), when we test the hypothesis Ho : βί-0 against Ha : βί 0 we use the t statistic with n-k-1 degrees of freedom. When Ho is not true find the expected value and variance of the test onsider the genera -~ 0 gains 0 1S not true find the expected value and variance of the test statistic.

e. Consider...

Considering multiple linear regression models, we compute the regression of Y, an n x 1 vector, on an n x (p+1) full rank matrix X. As usual, H = X(XT X)-1 XT is the hat matrix with elements hij at the ith row and jth column. The residual is e; = yi - Ýi. (a) (7 points) Let Y be an n x 1 vector with 1 as its first element and Os elsewhere. Show that the elements of the...

Considering multiple linear regression models, we compute the regression of Y, an n x 1 vector, on an n x (p+1) full rank matrix X. As usual, H = X(XT X)-1 XT is the hat matrix with elements hij at the ith row and jth column. The residual is e; = yi - Ýi. (a) (7 points) Let Y be an n x 1 vector with 1 as its first element and Os elsewhere. Show that the elements of the...

Considering multiple linear regression models, we compute the regression of Y, an n x 1 vector, on an n x (p+1) full rank matrix X. As usual, H = X(XT X)-1 XT is the hat matrix with elements hij at the ith row and jth column. The residual is e; = yi - Ýi. (a) (7 points) Let Y be an n x 1 vector with 1 as its first element and Os elsewhere. Show that the elements of the...

Considering multiple linear regression models, we compute the regression of Y, an n x 1 vector, on an n x (p+1) full rank matrix X. As usual, H = X(XT X)-1 XT is the hat matrix with elements hij at the ith row and jth column. The residual is e; = yi - Ýi. (a) (7 points) Let Y be an n x 1 vector with 1 as its first element and Os elsewhere. Show that the elements of the...

3. In the usual setup for multiple regression, e, hi, Vo) are the raw residual, leverage, and the i-th leave-one-out fitted response, respectively. The i-th deleted residual sum of square is defined as where yo: (n-1)x1, the response vector with the i-th entry deleted; Xo): (n-1) x p is the design matrix with the i-th row deleted (a) (Stat438 ONLY) Show that SSRestSSRes-_ by using the following results SS Res e2 SSRes (b) Use the result from (a), show that...

3. In the usual setup for multiple regression, e, hi, Vo) are the raw residual, leverage, and the i-th leave-one-out fitted response, respectively. The i-th deleted residual sum of square is defined as where yo: (n-1)x1, the response vector with the i-th entry deleted; Xo): (n-1) x p is the design matrix with the i-th row deleted (a) (Stat438 ONLY) Show that SSRestSSRes-_ by using the following results SS Res e2 SSRes (b) Use the result from (a), show that...

linear stat modeling & regression

please ,

i need the solution for Q3, but i copy Q2 because you need

info from Q2 in order to answer Q3.

2) Suppose you have multiple regression set up YxXBp The ridge regression estimator is given by Here, llell'-Σ.< where is a vector of Vik. a) Find the expectation and variance-covariance matrix of Bridge, when X'X is a diagonal matrix with each diagonal entry is eqal to. Com pare these variances with the...

linear stat modeling & regression

please ,

i need the solution for Q3, but i copy Q2 because you need

info from Q2 in order to answer Q3.

2) Suppose you have multiple regression set up YxXBp The ridge regression estimator is given by Here, llell'-Σ.< where is a vector of Vik. a) Find the expectation and variance-covariance matrix of Bridge, when X'X is a diagonal matrix with each diagonal entry is eqal to. Com pare these variances with the...

3. In the multiple regression model shown in the previous question, which one of the following statements is incorrect: (b) The sum of squared residuals is the square of the length of the vector ü (c) The residual vector is orthogonal to each of the columns of X (d) The square of the length of y is equal to the square of the length of y plus the square of the length of û by the Pythagoras theorem In all...

3. In the multiple regression model shown in the previous question, which one of the following statements is incorrect: (b) The sum of squared residuals is the square of the length of the vector ü (c) The residual vector is orthogonal to each of the columns of X (d) The square of the length of y is equal to the square of the length of y plus the square of the length of û by the Pythagoras theorem In all...

In the context of multiple regression, define the n X n matrix M =- X(X'X)-'X'. (i) Show that M is symmetric and idempotent. (ii) Prove that m, the diagonals of the matrix M, satisfy 0 sm s 1 for t = 1, 2, ..., n. (iii) Consider the linear model y = XB + u satisfies the Gauss-Markov Assumptions. Let û be the vector of OLS residuals. Show that Eſûù' x) = oʻM (iv) Conclude that while the errors {u:...

In the context of multiple regression, define the n X n matrix M =- X(X'X)-'X'. (i) Show that M is symmetric and idempotent. (ii) Prove that m, the diagonals of the matrix M, satisfy 0 sm s 1 for t = 1, 2, ..., n. (iii) Consider the linear model y = XB + u satisfies the Gauss-Markov Assumptions. Let û be the vector of OLS residuals. Show that Eſûù' x) = oʻM (iv) Conclude that while the errors {u:...

In the context of multiple regression, define the n X n matrix M =- X(X'X)-'X'. (i) Show that M is symmetric and idempotent. (ii) Prove that m, the diagonals of the matrix M, satisfy 0 sm s 1 for t = 1, 2, ..., n. (iii) Consider the linear model y = XB + u satisfies the Gauss-Markov Assumptions. Let û be the vector of OLS residuals. Show that Eſûù' x) = oʻM (iv) Conclude that while the errors {u:...

In the context of multiple regression, define the n X n matrix M =- X(X'X)-'X'. (i) Show that M is symmetric and idempotent. (ii) Prove that m, the diagonals of the matrix M, satisfy 0 sm s 1 for t = 1, 2, ..., n. (iii) Consider the linear model y = XB + u satisfies the Gauss-Markov Assumptions. Let û be the vector of OLS residuals. Show that Eſûù' x) = oʻM (iv) Conclude that while the errors {u:...

4. We have n statistical units. For unit i, we have (xi; yi), for i-1,2,... ,n. We used the least squares line to obtain the estimated regression line у = bo +biz. (a) Show that the centroid (x, y) is a point on the least squares line, where x = (1/n) and у = (1/n) Σ¡ı yi. (Hint: E ) i-1 valuate the line at x = x. (b) In the suggested exercises, we showed that e,-0 and e-0, where...

4. We have n statistical units. For unit i, we have (xi; yi), for i-1,2,... ,n. We used the least squares line to obtain the estimated regression line у = bo +biz. (a) Show that the centroid (x, y) is a point on the least squares line, where x = (1/n) and у = (1/n) Σ¡ı yi. (Hint: E ) i-1 valuate the line at x = x. (b) In the suggested exercises, we showed that e,-0 and e-0, where...

1.Given the Multiple Linear regression model as Y-Po + β.X1 + β2X2 + β3Xs + which in matrix notation is written asy-xß +ε where -έ has a N(0,a21) distribution + + ßpXo +ε A. Show that the OLS estimator of the parameter vector B is given by B. Show that the OLS in A above is an unbiased estimator of β Hint: E(β)-β C. Show that the variance of the estimator is Var(B)-o(Xx)-1 D. What is the distribution o the...

1.Given the Multiple Linear regression model as Y-Po + β.X1 + β2X2 + β3Xs + which in matrix notation is written asy-xß +ε where -έ has a N(0,a21) distribution + + ßpXo +ε A. Show that the OLS estimator of the parameter vector B is given by B. Show that the OLS in A above is an unbiased estimator of β Hint: E(β)-β C. Show that the variance of the estimator is Var(B)-o(Xx)-1 D. What is the distribution o the...

e. Consider the multiple regression model y X 3+E. with E(e)-0 and var (e) ơ21 Assume that ε ~ N(0 σ21), when we test the hypothesis Ho : βί-0 against Ha : βί 0 we use the t statistic with n-k-1 degrees of freedom. When Ho is not true find the expected value and variance of the test onsider the genera -~ 0 gains 0 1S not true find the expected value and variance of the test statistic.

e. Consider...

e. Consider the multiple regression model y X 3+E. with E(e)-0 and var (e) ơ21 Assume that ε ~ N(0 σ21), when we test the hypothesis Ho : βί-0 against Ha : βί 0 we use the t statistic with n-k-1 degrees of freedom. When Ho is not true find the expected value and variance of the test onsider the genera -~ 0 gains 0 1S not true find the expected value and variance of the test statistic.

e. Consider...

Most questions answered within 3 hours.

-

Twitter Users and News: A poll conducted in 2013 found that 52%

of U.S. adult Twitter...

asked 10 minutes ago -

How

would I know whether a given amino acid has an ionizable group or

not? please...

asked 18 minutes ago -

True or false?

True False The function of the enzyme acyl CoA

synthetase is the ATP-dependent coupling...

asked 18 minutes ago -

Nadia Corporation adjusts its debt so that its interest coverage

(EBIT/Interest) remains constant at 3. Nadia’s...

asked 20 minutes ago -

In a clinical trial, 20 out of 600 patients taking a

prescription drug complained of flulike...

asked 26 minutes ago -

7. How many types of nuclear processes can produce energy? 8.

How many types of radioactive...

asked 30 minutes ago -

For both the Sn2 and Sn1 reaction

conditions:

Structure | Rxn (Y/N) at room T° Rxn...

asked 30 minutes ago -

11. In cell N2, enter a formula using the IF function and a

structured reference to...

asked 30 minutes ago -

There is X-linked mutations in flies in this example. You need

to determine the inheritence pattern...

asked 32 minutes ago -

1) There is a 5.0 μC charge at each of 3 corners of a square

(each...

asked 43 minutes ago -

A study of 420,095 cell phone users found that

134 of them developed cancer of the...

asked 47 minutes ago -

2.50 g of NH4Cl is added to 12.9 g of water. Calculate the

molality of the...

asked 49 minutes ago