![Consolidation Journal Description Debit Credit ADJ] [E] Common Stock APIC A PPE, net Patent Patent](http://img.homeworklib.com/images/918e8426-8e8c-4f64-8745-8fbb95d7a6cb.png?x-oss-process=image/resize,w_560)

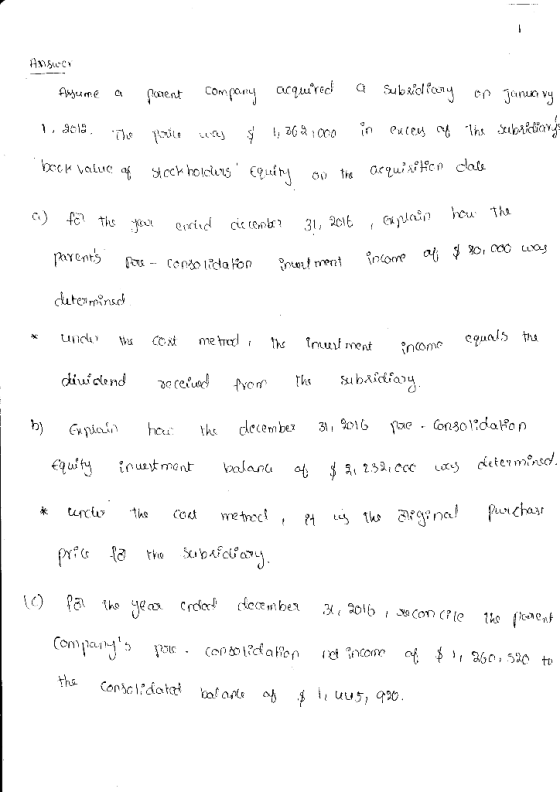

Balance sheet Assets Cash Accounts receivable Inventory Equity investment Property, plant & equipment Patent list Goodwill 1,709,760 551,200 2,260,960 2,686,800 459,6003,146,400 3,520,200 589,8004,110,000 2,232,000 12,752,640 1,091,400 14,069,040 252,000 630,000 $22,901,400 $2,692,000 $24,468,400 Liabilities and stockholders' equity Accounts payable Accrued liabilities Long-term liabilities Common stock APIC Retained earnings 1,517,400 1,825,680 ,550,000 660,000 6,210,000 845,520 6,335,880 165,000 6,335,880 7,262,520 1,299,4007,733,920 $22,901,400 $2,692,000 $24,468,400 1,328,640 188,760 1,578,840 246,840 845,520 132,000 a. For the year ended December 31, 2016, explain how the parent's pre-consolidation investment income of $80,800 was determined

b. Explain how the parent's December 31, 2016 pre-consolidation Equity Investment balance of $2,232,000 was determined.

c. For the year ended December 31, 2016, reconcile the parent company's pre-consolidation net income of $1,260,520 to the consolidated balance of $1,445,920 Do not use negative signs with your answers

d. What was the subsidiary's retained earnings balance on the acquisition date? (Hint: You will need to use an account that does not change after the acquisition date.)

e. Why aren't the Stockholders' Equity accounts of the subsidiary reflected in the consolidated balance sheet?

f. Provide the consolidation entries for the year ending December 31, 2016.

Consolidation Journal Description Debit Credit ADJ] [E] Common Stock APIC A PPE, net Patent Patent

Homework Answers

Add Answer to:

Inferring consolidation entries from consolidated financial statements-Cost method Assume a paren...

Inferring consolidation entries from consolidated financial statements—Cost method Assume a parent company acquired a subsidiary on...

Inferring consolidation entries from consolidated financial statements—Cost method Assume a parent company acquired a subsidiary on January 1, 2012. The purchase price was $1,312,000 in excess of the subsidiary’s book value of Stockholders’ Equity on the acquisition date, and that excess was assigned to the following [A] assets: [A] Asset Original Amount Original Useful Life Property, plant and equipment (PPE), net $300,000 20 years Patent 432,000 12 years Goodwill 580,000 Indefinite $1,312,000 The parent company uses the cost method of...

Prepare consolidation spreadsheet for intercompany sale of land - Equity method Assume that a parent company acquired i...

Prepare consolidation spreadsheet for intercompany sale of land - Equity method Assume that a parent company acquired its subsidiary on January 1, 2014, at a purchase price that was $300,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition date. Of that excess, $200,000 was assigned to an unrecorded Patent owned by the subsidiary that is being amortized over a 10-year period. The [A] Patent asset has been amortized as part of the parent's equity...

Prepare consolidation spreadsheet for intercompany sale of land - Equity method Assume that a parent company acquired its subsidiary on January 1, 2014, at a purchase price that was $300,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition date. Of that excess, $200,000 was assigned to an unrecorded Patent owned by the subsidiary that is being amortized over a 10-year period. The [A] Patent asset has been amortized as part of the parent's equity...

Consolidation on date of acquisition - Equity method with noncontrolling interest and AAP Assume a parent...

Consolidation on date of acquisition - Equity method with noncontrolling interest and AAP Assume a parent company acquires a 75% interest in its subsidiary for a purchase price of $924,000. The excess of the total fair value of the controlling and noncontrolling Interests over the book value of the subsidiary's Stockholders' Equity is assigned to a building in PPE, net) that is worth $88,000 more than its book value, an unrecorded patent with a fair value of $144,000, and Goodwill...

Consolidation on date of acquisition - Equity method with noncontrolling interest and AAP Assume a parent company acquires a 75% interest in its subsidiary for a purchase price of $924,000. The excess of the total fair value of the controlling and noncontrolling Interests over the book value of the subsidiary's Stockholders' Equity is assigned to a building in PPE, net) that is worth $88,000 more than its book value, an unrecorded patent with a fair value of $144,000, and Goodwill...

Consolidation on date of acquisition - Equity method with noncontrolling interest and AAP Assume ...

Consolidation on date of acquisition - Equity method with noncontrolling interest and AAP Assume that a parent company acquires an 80% interest in its subsidiary for a purchase price of $620,800. The excess of the total fair value of the controlling and noncontrolling interests over the book value of the subsidiary's Stockholders' Equity is assigned to a building (in PPE, net) that the parent believes is worth $50,000 more than its book value, an: unrecorded Patent that the parent valued...

Consolidation on date of acquisition - Equity method with noncontrolling interest and AAP Assume that a parent company acquires an 80% interest in its subsidiary for a purchase price of $620,800. The excess of the total fair value of the controlling and noncontrolling interests over the book value of the subsidiary's Stockholders' Equity is assigned to a building (in PPE, net) that the parent believes is worth $50,000 more than its book value, an: unrecorded Patent that the parent valued...

Consolidation spreadsheet for continuous sale of inventory - Equity method Assume that a parent c...

Consolidation spreadsheet for continuous sale of inventory - Equity method Assume that a parent company acquired a subsidiary on January 1, 2010. The purchase price was 500,000 million in excess of the subsidiary's book value of Stockholders' Equity on the acquisition date and that excess was assigned to the following AAP assets Original Original Useful Amount Life (years) AAP Asset Property, plant and equipment (PPE), net Customer list Royalty agreement Goodwill $100,000 185,000 115,000 100,000 $500,000 20 indefinite The AAP...

Consolidation spreadsheet for continuous sale of inventory - Equity method Assume that a parent company acquired a subsidiary on January 1, 2010. The purchase price was 500,000 million in excess of the subsidiary's book value of Stockholders' Equity on the acquisition date and that excess was assigned to the following AAP assets Original Original Useful Amount Life (years) AAP Asset Property, plant and equipment (PPE), net Customer list Royalty agreement Goodwill $100,000 185,000 115,000 100,000 $500,000 20 indefinite The AAP...

Prepare consolidation spreadsheet for intercompany sale of land - Equity Method Assume a parent company acquired...

Prepare consolidation spreadsheet for intercompany sale of land - Equity Method Assume a parent company acquired its subsidiary on January 1, 2017, at a purchase price that was $270,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition date. Of that excess, $180,000 was assigned to an unrecorded patent owned by the subsidiary that is being amortized over a 10 year period. The [A] Patent asset has been amortized as part of the parent's equity...

Consolidation subsequent to date of acquisition - Equity method with noncontrolling interest and ...

Consolidation subsequent to date of acquisition - Equity method with noncontrolling interest and AAP Assume that, on January 1, 2009, a parent company acquired an 80% interest in its subsidiary. The total fair value of the controlling and noncontrolling interests was $500,000 over the book value of the subsidiary’s Stockholders’ Equity on the acquisition date. The parent assigned the excess to the following [A] assets: [A] Asset Initial Fair Value Useful Life (years) [A] Asset Initial Fair Value Useful Life...

Subsidiary 46. Prepare consolidation spreadsheet for intercompany sale of land-Equity method LOS Assume a parent company...

Subsidiary 46. Prepare consolidation spreadsheet for intercompany sale of land-Equity method LOS Assume a parent company acquired its subsidiary on January 1, 2017, at a purchase price that was $270,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition date. X of that excess, $180,000 was assigned to an unrecorded Patent owned by the subsidiary that is being amortized over a 10-year period. The [A] Patent asset has been amortized as part of the parent's...

Subsidiary 46. Prepare consolidation spreadsheet for intercompany sale of land-Equity method LOS Assume a parent company acquired its subsidiary on January 1, 2017, at a purchase price that was $270,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition date. X of that excess, $180,000 was assigned to an unrecorded Patent owned by the subsidiary that is being amortized over a 10-year period. The [A] Patent asset has been amortized as part of the parent's...

200 Chapter 41 Consolidated PROBLEMS base price was date, and that was LO 19. Consolidation spreadsheet...

200 Chapter 41 Consolidated PROBLEMS base price was date, and that was LO 19. Consolidation spreadsheet for continuous cale of inventory-Equity method Assume a parent company acquired a subsidiary on January 1, 2016. The purchas i n excess of the subsidiary's book value of Stockholders' Equity on the acquisition was assigned to the following AAP assets: X Original Amount Original Use Line . $120.000 210.000 150.000 120,000 $600,000 AAP Asset Property, plant and equipment (PPE), net . Customer list... Royalty...

200 Chapter 41 Consolidated PROBLEMS base price was date, and that was LO 19. Consolidation spreadsheet for continuous cale of inventory-Equity method Assume a parent company acquired a subsidiary on January 1, 2016. The purchas i n excess of the subsidiary's book value of Stockholders' Equity on the acquisition was assigned to the following AAP assets: X Original Amount Original Use Line . $120.000 210.000 150.000 120,000 $600,000 AAP Asset Property, plant and equipment (PPE), net . Customer list... Royalty...

Consolidation at date of acquisition (purchase price greater than book value, acquisition journal entries Assume that...

Consolidation at date of acquisition (purchase price greater than book value, acquisition journal entries Assume that the parent company acquires its subsidiary by exchanging 84,000 shares of its $2 par value Common Stock, with a fair value on the acquisition date of $41 per share, for all of the outstanding voting shares of the investee. In its analysis of the investee company, the parent values all of the subsidiary’s assets and liabilities at an amount equaling their book values except...

Prepare consolidation spreadsheet for intercompany sale of land - Equity method Assume that a parent company acquired its subsidiary on January 1, 2014, at a purchase price that was $300,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition date. Of that excess, $200,000 was assigned to an unrecorded Patent owned by the subsidiary that is being amortized over a 10-year period. The [A] Patent asset has been amortized as part of the parent's equity...

Prepare consolidation spreadsheet for intercompany sale of land - Equity method Assume that a parent company acquired its subsidiary on January 1, 2014, at a purchase price that was $300,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition date. Of that excess, $200,000 was assigned to an unrecorded Patent owned by the subsidiary that is being amortized over a 10-year period. The [A] Patent asset has been amortized as part of the parent's equity...

Consolidation on date of acquisition - Equity method with noncontrolling interest and AAP Assume a parent company acquires a 75% interest in its subsidiary for a purchase price of $924,000. The excess of the total fair value of the controlling and noncontrolling Interests over the book value of the subsidiary's Stockholders' Equity is assigned to a building in PPE, net) that is worth $88,000 more than its book value, an unrecorded patent with a fair value of $144,000, and Goodwill...

Consolidation on date of acquisition - Equity method with noncontrolling interest and AAP Assume a parent company acquires a 75% interest in its subsidiary for a purchase price of $924,000. The excess of the total fair value of the controlling and noncontrolling Interests over the book value of the subsidiary's Stockholders' Equity is assigned to a building in PPE, net) that is worth $88,000 more than its book value, an unrecorded patent with a fair value of $144,000, and Goodwill...

Consolidation on date of acquisition - Equity method with noncontrolling interest and AAP Assume that a parent company acquires an 80% interest in its subsidiary for a purchase price of $620,800. The excess of the total fair value of the controlling and noncontrolling interests over the book value of the subsidiary's Stockholders' Equity is assigned to a building (in PPE, net) that the parent believes is worth $50,000 more than its book value, an: unrecorded Patent that the parent valued...

Consolidation on date of acquisition - Equity method with noncontrolling interest and AAP Assume that a parent company acquires an 80% interest in its subsidiary for a purchase price of $620,800. The excess of the total fair value of the controlling and noncontrolling interests over the book value of the subsidiary's Stockholders' Equity is assigned to a building (in PPE, net) that the parent believes is worth $50,000 more than its book value, an: unrecorded Patent that the parent valued...

Consolidation spreadsheet for continuous sale of inventory - Equity method Assume that a parent company acquired a subsidiary on January 1, 2010. The purchase price was 500,000 million in excess of the subsidiary's book value of Stockholders' Equity on the acquisition date and that excess was assigned to the following AAP assets Original Original Useful Amount Life (years) AAP Asset Property, plant and equipment (PPE), net Customer list Royalty agreement Goodwill $100,000 185,000 115,000 100,000 $500,000 20 indefinite The AAP...

Consolidation spreadsheet for continuous sale of inventory - Equity method Assume that a parent company acquired a subsidiary on January 1, 2010. The purchase price was 500,000 million in excess of the subsidiary's book value of Stockholders' Equity on the acquisition date and that excess was assigned to the following AAP assets Original Original Useful Amount Life (years) AAP Asset Property, plant and equipment (PPE), net Customer list Royalty agreement Goodwill $100,000 185,000 115,000 100,000 $500,000 20 indefinite The AAP...

Subsidiary 46. Prepare consolidation spreadsheet for intercompany sale of land-Equity method LOS Assume a parent company acquired its subsidiary on January 1, 2017, at a purchase price that was $270,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition date. X of that excess, $180,000 was assigned to an unrecorded Patent owned by the subsidiary that is being amortized over a 10-year period. The [A] Patent asset has been amortized as part of the parent's...

Subsidiary 46. Prepare consolidation spreadsheet for intercompany sale of land-Equity method LOS Assume a parent company acquired its subsidiary on January 1, 2017, at a purchase price that was $270,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition date. X of that excess, $180,000 was assigned to an unrecorded Patent owned by the subsidiary that is being amortized over a 10-year period. The [A] Patent asset has been amortized as part of the parent's...

200 Chapter 41 Consolidated PROBLEMS base price was date, and that was LO 19. Consolidation spreadsheet for continuous cale of inventory-Equity method Assume a parent company acquired a subsidiary on January 1, 2016. The purchas i n excess of the subsidiary's book value of Stockholders' Equity on the acquisition was assigned to the following AAP assets: X Original Amount Original Use Line . $120.000 210.000 150.000 120,000 $600,000 AAP Asset Property, plant and equipment (PPE), net . Customer list... Royalty...

200 Chapter 41 Consolidated PROBLEMS base price was date, and that was LO 19. Consolidation spreadsheet for continuous cale of inventory-Equity method Assume a parent company acquired a subsidiary on January 1, 2016. The purchas i n excess of the subsidiary's book value of Stockholders' Equity on the acquisition was assigned to the following AAP assets: X Original Amount Original Use Line . $120.000 210.000 150.000 120,000 $600,000 AAP Asset Property, plant and equipment (PPE), net . Customer list... Royalty...

Most questions answered within 3 hours.

-

Buckminsterfullerence is a recently allotrope of carbon in which

carbon atoms form molecules of formula C_60,...

asked 19 seconds from now -

Lower Equitorial and Upper Equitorial are the same except Lower

Equitorial has a larger capital stock....

asked 4 minutes ago -

how do you think that pH of a jar where you have added a certain

amount...

asked 14 minutes ago -

If the Federal Reserve increases the reserve requirement, what

will happen to the Money Supply in...

asked 9 minutes ago -

Suppose that market demand for a good is given by Q = 9 - 0.3 P...

asked 15 minutes ago -

two thin lenses are separated by a distance x. The first lens

has a focal length...

asked 17 minutes ago -

The computer that controls a bank's automatic teller machine

crashes a mean of 0.6 times per...

asked 20 minutes ago -

`1) How is -9 (base 10) represented in 8-bit two's complement

notation?

a) 00001001

b)11110111

c)11110110...

asked 30 minutes ago -

A 10.000 g sample of water contains 11.19% H by mass. what

should be the %H...

asked 48 minutes ago -

Consider an investment game among 2 players. Each player can

either invest,

i, or not invest,-i....

asked 45 minutes ago -

The time taken to complete a particular task is normally

distributed with a standard deviation of...

asked 55 minutes ago -

we have heteroskedasticity in a regression when:

When the variance of error terms changes when an...

asked 1 hour ago