The following information is given about options on the stock of a certain company: ...

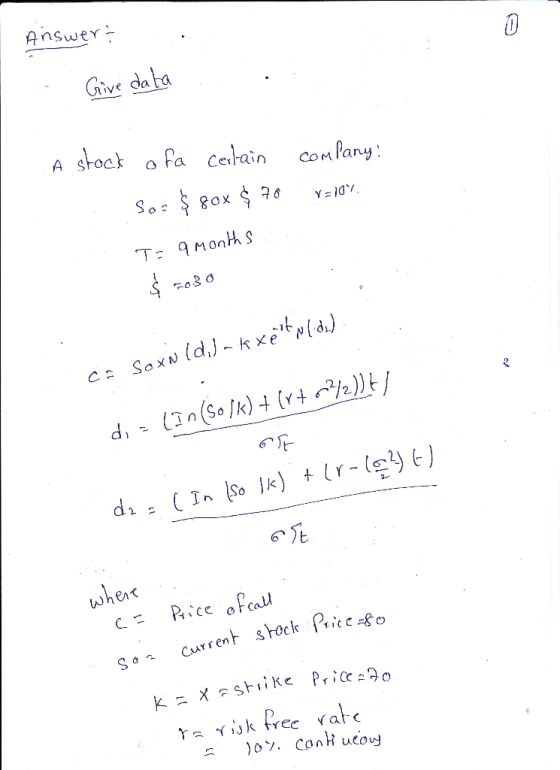

The following information is given about options on the stock of a certain company:

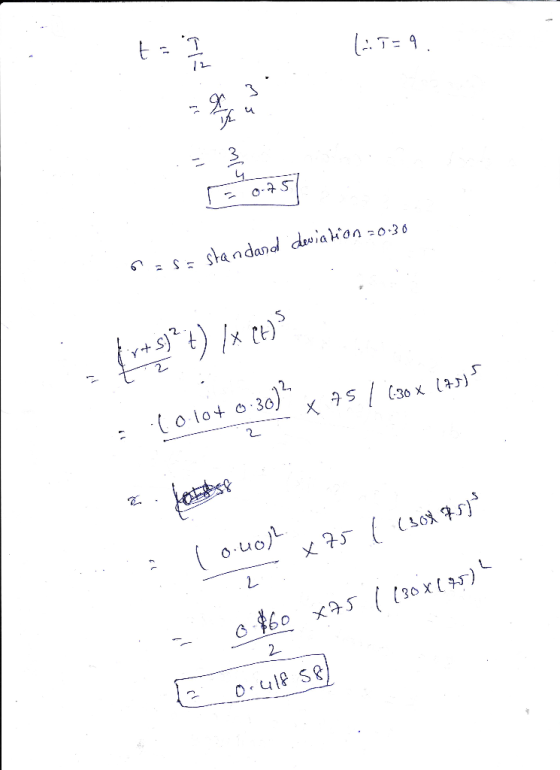

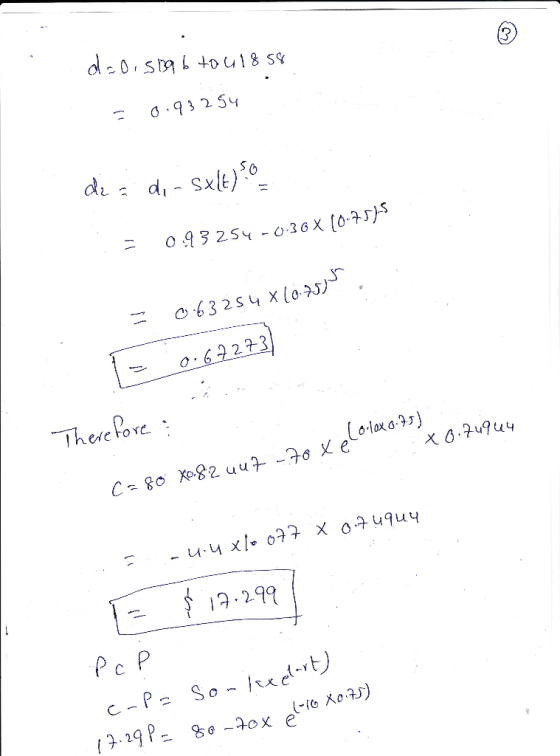

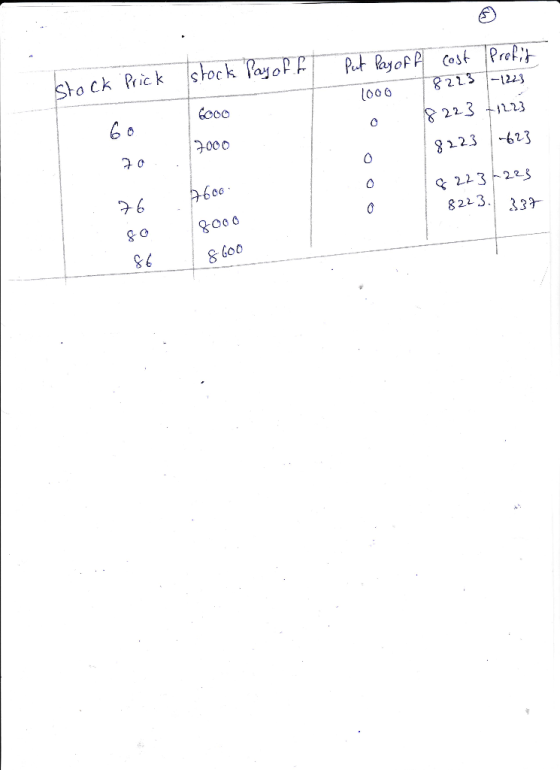

S0 = $80, X =$70, r =10% per year (continuously compounded), T = 9 months, s= 0.30

No dividends are expected. One option contract is for 100 shares of the stock. All notations are used in the same way as in the Black-Scholes-Merton Model.

- What is the European call option price and European put option price, according to the Black-Scholes model?

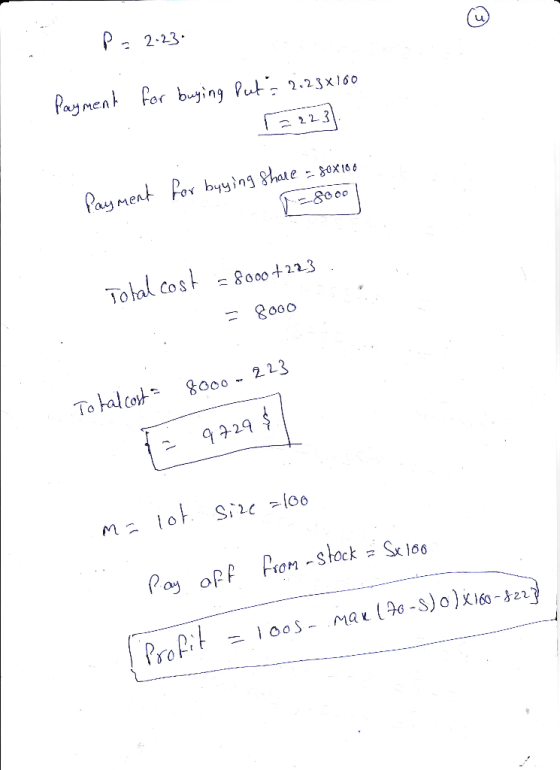

- What is the cost of buying a protective put?

- What is the cost of writing a covered call?

- What will be the payoff and profit of the protective put if the stock price on maturity is $60, $70, $76, $80, $86?

- What will be the payoff and profit of the covered call if the stock price on maturity is $60, $70, $76, $80, $86?

Homework Answers

Add Answer to:

The following information is given about options on the stock of a certain company: ...

Consider an option on a non-dividend-paying stock when the stock price is $30, the exercise price...

Consider an option on a non-dividend-paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5% per annum, the volatility is 25% per annum, and the time to maturity is four months. Use the Black-Scholes-Merton formula. What is the price of the option if it is a European call? What is the price of the option if it is an American call? What is the price of the option if it is...

On October 2, 2018, Tesla stock was trading $305.65. There are options on Tesla stock, Below...

On October 2, 2018, Tesla stock was trading $305.65. There are options on Tesla stock, Below are the yarigble inputs you require. Using the Black-Scholes-Merton model and Solyer, solve for the implied volatility that causes the option to be valued at $44.25. The appropriate risk free rate c.c. is 0.85%. These are European Options. Underlying So Call or Put Strike 306.65 Put 300.00 10/2/18 3/15/19 Today Maturity Time to Expiration Volatility Risk Free Rate 59.52% 0.85% #N/ A #N/A #N/A...

On October 2, 2018, Tesla stock was trading $305.65. There are options on Tesla stock, Below are the yarigble inputs you require. Using the Black-Scholes-Merton model and Solyer, solve for the implied volatility that causes the option to be valued at $44.25. The appropriate risk free rate c.c. is 0.85%. These are European Options. Underlying So Call or Put Strike 306.65 Put 300.00 10/2/18 3/15/19 Today Maturity Time to Expiration Volatility Risk Free Rate 59.52% 0.85% #N/ A #N/A #N/A...

Consider an asset that trades at $100 today. Suppose that the European call and put options...

Consider an asset that trades at $100 today. Suppose that the European call and put options on this asset are available both with a strike price of $100. The options expire in 275 days, and the volatility is 45%. The continuously compounded risk-free rate is 3%. Determine the value of the European call and put options using the Black-Scholes-Merton model. Assume that the continuously compounded yield on the asset is 1,5% and there are 365 days in the year.

Consider a European put option on a non-dividend-paying stock. The current stock price is $69, the...

Consider a European put option on a non-dividend-paying stock. The current stock price is $69, the strike price is $70, the risk-free interest rate is 5% per annum, the volatility is 35% per annum and the time to maturity is 6 months. a. Use the Black-Scholes model to calculate the put price. b. Calculate the corresponding call option using the put-call parity relation. Use the Option Calculator Spreadsheet to verify your result.

Question 1 a. A stock price is currently $30. It is known that at the end...

Question 1 a. A stock price is currently $30. It is known that at the end of two months it will be either $33 or $27. The risk-free interest rate is 10% per annum with continuous compounding. What is the value of a two-month European put option with a strike price of $31? b. What is meant by the delta of a stock option? A stock price is currently $100. Over each of the next two three-month periods it is...

Question 1 a. A stock price is currently $30. It is known that at the end of two months it will be either $33 or $27. The risk-free interest rate is 10% per annum with continuous compounding. What is the value of a two-month European put option with a strike price of $31? b. What is meant by the delta of a stock option? A stock price is currently $100. Over each of the next two three-month periods it is...

6) Consider an option on a non-dividend paying stock when the stock price is $38, the exercise price is $40, the risk-free interest rate is 6% per annum, the volatility is 30% per annum, and the time...

6) Consider an option on a non-dividend paying stock when the stock price is $38, the exercise price is $40, the risk-free interest rate is 6% per annum, the volatility is 30% per annum, and the time to maturity is six months. Using Black-Scholes Model, calculating manually, a. What is the price of the option if it is a European call? b. What is the price of the option if it is a European put? c. Show that the put-call...

You are given the following information concerning options on a particular stock: Stock price = $83...

You are given the following information concerning options on a particular stock: Stock price = $83 Exercise price = $80 Risk-free rate = 6% per year, compounded continuously Maturity = 6 months Standard deviation = 53% per year a). What are the prices of a call option and a put option with the above characteristics? b). What is the intrinsic value of the call option? The put option? c). What is the time value of the call option? The put...

(a) State the Black-Scholes formulas for the prices at time 0 of a European call and put options on a non-dividend-paying stock ABC

2. (a) State the Black-Scholes formulas for the prices at time 0 of a European call and put options on a non-dividend-paying stock ABC.(b) Consider an option on a non-dividend paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5% per annum, the volatility is 20% per annum, and the time to maturity is 5 months. What is the price of the option if it is a European call?

Saved In addition to the five factors, dividends also affect the price of an option. The...

Saved In addition to the five factors, dividends also affect the price of an option. The Black- Scholes Option Pricing Model with dividends is: All of the variables are the same as the Black-Scholes model without dividends except for the variable d, which for the varable d, which continuously compounde is the continuously compounded dividend yield on the stock The put call party condition is also altered when dividends are paid. The dividend- adjusted put-call parity formula is: where dis...

Saved In addition to the five factors, dividends also affect the price of an option. The Black- Scholes Option Pricing Model with dividends is: All of the variables are the same as the Black-Scholes model without dividends except for the variable d, which for the varable d, which continuously compounde is the continuously compounded dividend yield on the stock The put call party condition is also altered when dividends are paid. The dividend- adjusted put-call parity formula is: where dis...

Assume the Black-Scholes framework for options pricing. You are a portfolio manager and already have a...

Assume the Black-Scholes framework for options pricing. You are a portfolio manager and already have a long position in Apple (ticker: AAPL). You want to protect your long position against losses and decide to buy a European put option on AAPL with a strike price of $180.15 and an expiration date of 1-year from today. The continuously compounded risk free interest rate is 8% and the stock pays no dividends. The current stock price for AAPL is $200 and its...

Assume the Black-Scholes framework for options pricing. You are a portfolio manager and already have a long position in Apple (ticker: AAPL). You want to protect your long position against losses and decide to buy a European put option on AAPL with a strike price of $180.15 and an expiration date of 1-year from today. The continuously compounded risk free interest rate is 8% and the stock pays no dividends. The current stock price for AAPL is $200 and its...

On October 2, 2018, Tesla stock was trading $305.65. There are options on Tesla stock, Below are the yarigble inputs you require. Using the Black-Scholes-Merton model and Solyer, solve for the implied volatility that causes the option to be valued at $44.25. The appropriate risk free rate c.c. is 0.85%. These are European Options. Underlying So Call or Put Strike 306.65 Put 300.00 10/2/18 3/15/19 Today Maturity Time to Expiration Volatility Risk Free Rate 59.52% 0.85% #N/ A #N/A #N/A...

On October 2, 2018, Tesla stock was trading $305.65. There are options on Tesla stock, Below are the yarigble inputs you require. Using the Black-Scholes-Merton model and Solyer, solve for the implied volatility that causes the option to be valued at $44.25. The appropriate risk free rate c.c. is 0.85%. These are European Options. Underlying So Call or Put Strike 306.65 Put 300.00 10/2/18 3/15/19 Today Maturity Time to Expiration Volatility Risk Free Rate 59.52% 0.85% #N/ A #N/A #N/A...

Question 1 a. A stock price is currently $30. It is known that at the end of two months it will be either $33 or $27. The risk-free interest rate is 10% per annum with continuous compounding. What is the value of a two-month European put option with a strike price of $31? b. What is meant by the delta of a stock option? A stock price is currently $100. Over each of the next two three-month periods it is...

Question 1 a. A stock price is currently $30. It is known that at the end of two months it will be either $33 or $27. The risk-free interest rate is 10% per annum with continuous compounding. What is the value of a two-month European put option with a strike price of $31? b. What is meant by the delta of a stock option? A stock price is currently $100. Over each of the next two three-month periods it is...

Saved In addition to the five factors, dividends also affect the price of an option. The Black- Scholes Option Pricing Model with dividends is: All of the variables are the same as the Black-Scholes model without dividends except for the variable d, which for the varable d, which continuously compounde is the continuously compounded dividend yield on the stock The put call party condition is also altered when dividends are paid. The dividend- adjusted put-call parity formula is: where dis...

Saved In addition to the five factors, dividends also affect the price of an option. The Black- Scholes Option Pricing Model with dividends is: All of the variables are the same as the Black-Scholes model without dividends except for the variable d, which for the varable d, which continuously compounde is the continuously compounded dividend yield on the stock The put call party condition is also altered when dividends are paid. The dividend- adjusted put-call parity formula is: where dis...

Assume the Black-Scholes framework for options pricing. You are a portfolio manager and already have a long position in Apple (ticker: AAPL). You want to protect your long position against losses and decide to buy a European put option on AAPL with a strike price of $180.15 and an expiration date of 1-year from today. The continuously compounded risk free interest rate is 8% and the stock pays no dividends. The current stock price for AAPL is $200 and its...

Assume the Black-Scholes framework for options pricing. You are a portfolio manager and already have a long position in Apple (ticker: AAPL). You want to protect your long position against losses and decide to buy a European put option on AAPL with a strike price of $180.15 and an expiration date of 1-year from today. The continuously compounded risk free interest rate is 8% and the stock pays no dividends. The current stock price for AAPL is $200 and its...

Most questions answered within 3 hours.

-

An entomologist discovers a dung beetle rolling a ball of dung

along the ground, and decides...

asked 57 minutes ago -

Humans have used horses for transportation for millions of

years. Therefore, they will use horses for...

asked 2 hours ago -

The following are the Jensen Corporation's unit costs of making

and selling an item at a...

asked 3 hours ago -

Does direct Medicare reimbursement of Advanced practice nurses

increase access to their services?

asked 4 hours ago -

List and explain why a company would choose to use a

published

compensation survey vs. creating...

asked 4 hours ago -

A discrete random variable X can take values from 1 to 10. Find

the variance of...

asked 4 hours ago -

The primary financial goal of a corporation is to maximize:

shareholders wealth.

earnings per share.

stock...

asked 4 hours ago -

determine whether the vectors u=(1,2,3,), v=(-2,1,0) and

w=(1,0,1) are linearly dependent or independent.

asked 4 hours ago -

python

Define a function called print_values which takes a dictionary

object as a parameter. The function...

asked 5 hours ago -

In Chapter 1 you created a program named Triangle in

which you displayed a seven-line triangle...

asked 5 hours ago -

Research question: What are the differences between separately

stated and non separately stated transactions in an...

asked 6 hours ago -

By using Arduino write a code that connects two LEDs to two

push-buttons. Each button controls...

asked 7 hours ago