You have been provided the following data about the securities of three firms, the market portfolio, and the risk-free asset:

| a. |

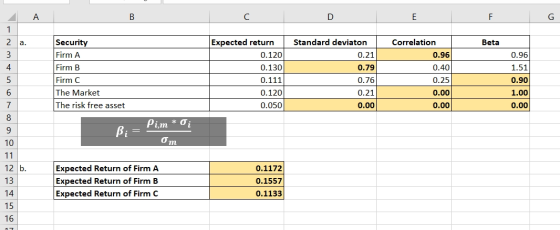

Fill in the missing values in the table. |

|

* With the market portfolio |

| b-1. | What is the expected return of Firm A? |

| b-2. | What is the expected return of Firm B? |

| b-3. | What is the expected return of Firm C? |

Homework Answers

Please refer to below spreadsheet for calculation and answer. Cell reference also provided.

Cell reference -

Hope this will help, please do comment if you need any further explanation. Your feedback would be highly appreciated.

Add Answer to:

You have been provided the following data about the securities of three firms, the market portfolio, and the risk-free a...

You have been provided the following data about the securities of three firms, the market portfolio, and the risk-free...

You have been provided the following data about the securities of three firms, the market portfolio, and the risk-free asset: a. Fill in the missing values in the table. (Leave no cells blank - be certain to enter o wherever required. Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Expected Return Standard Deviation Security Correlation* Beta Firm A 0.120 0.21 0.96 Firm B 0.40 0.130 1.51 Firm C The market portfolio 0.111 0.76...

You have been provided the following data about the securities of three firms, the market portfolio, and the risk-free asset: a. Fill in the missing values in the table. (Leave no cells blank - be certain to enter o wherever required. Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Expected Return Standard Deviation Security Correlation* Beta Firm A 0.120 0.21 0.96 Firm B 0.40 0.130 1.51 Firm C The market portfolio 0.111 0.76...

You have been provided the following data about the securities of three firms, the market portfolio, and the risk-fr...

You have been provided the following data about the securities of three firms, the market portfolio, and the risk-free asset: a. Fill in the missing values in the table. (Leave no cells blank - be certain to enter 0 wherever required. Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Security Expected Return Standard Deviation Correlations Beta Firm A 0.101 0.40 0.76 Firm B 0.149 0.59 1.31 Firm C 0.169 0.56 0.44 The...

You have been provided the following data about the securities of three firms, the market portfolio,...

You have been provided the following data about the securities

of three firms, the market portfolio, and the risk-free asset:

a. Fill in the missing values in the table. (Leave no cells

blank - be certain to enter 0 wherever required. Do not round

intermediate calculations and round your answers to 2 decimal

places, e.g., 32.16.)

b-1. What is the expected return of Firm A? (Do not round

intermediate calculations and enter your answer as a percent

rounded to 2...

You have been provided the following data about the securities

of three firms, the market portfolio, and the risk-free asset:

a. Fill in the missing values in the table. (Leave no cells

blank - be certain to enter 0 wherever required. Do not round

intermediate calculations and round your answers to 2 decimal

places, e.g., 32.16.)

b-1. What is the expected return of Firm A? (Do not round

intermediate calculations and enter your answer as a percent

rounded to 2...

You have been provided the following data about the securities of three firms, the market portfolio,...

You have been provided the following data about the securities of three firms, the market portfolio, and the risk-free asset a. Fill in the missing values in the table. (Leave no cells blank.be certain to enter 0 wherever required. Do not round Intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Correlation Security FA Expected Return Standard Deviation 0.102 033 0.1421 0.162 0.63 0.12 .191 0.08 0.37 Firm The market portfolio The risk tree ass * With...

You have been provided the following data about the securities of three firms, the market portfolio, and the risk-free asset a. Fill in the missing values in the table. (Leave no cells blank.be certain to enter 0 wherever required. Do not round Intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Correlation Security FA Expected Return Standard Deviation 0.102 033 0.1421 0.162 0.63 0.12 .191 0.08 0.37 Firm The market portfolio The risk tree ass * With...

You have been provided the following data on the securities of three firms, the market portfolio,...

You have been provided the following data on the securities of three firms, the market portfolio, and the risk-free asset: a. Fill in the missing values in the table. (Leave no cells blank - be certain to enter 0 wherever required. Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Security Expected Return Standard Deviation Correlation* Beta Firm A .101 .40 .76 Firm B .149 .59 1.31 Firm C .169 .56 .44 The market...

6. You have been provided the following data on the securities of three firms and the...

6. You have been provided the following data on the securities of three firms and the market: Et Security BI P/m Firm A 0.13 0.12 0.9 Firm B 0.16 0.40 1.10 Firm C 0.25 0.24 0.75 ? Market Risk-free 0.15 0.10 0.05 Assume the CAPM holds true. Fill in the missing values in the table. a. What is your investment recommendation on each asset? Buy or sell? b. Suppose that you are currently holding a portfolio consisting of Firm B...

6. You have been provided the following data on the securities of three firms and the market: Et Security BI P/m Firm A 0.13 0.12 0.9 Firm B 0.16 0.40 1.10 Firm C 0.25 0.24 0.75 ? Market Risk-free 0.15 0.10 0.05 Assume the CAPM holds true. Fill in the missing values in the table. a. What is your investment recommendation on each asset? Buy or sell? b. Suppose that you are currently holding a portfolio consisting of Firm B...

ci. You have been provided the following data on three securities and the market portfolio. Beta...

ci. You have been provided the following data on three securities and the market portfolio. Beta 1.5 Observed (Realized) Return 15.0% 12.0% 10.0% 10.0% 5.0% Security/Portfolio Security 1 Security 2 Security 3 Market portfolio Riskfree security Standard Deviation 01 18.0% 2.0% 4.0% 0.0% Correlation 1.0 0.4 P3, m B2 0.5 Pin, m Bm Pem BE Note that the return in the above table is the average realized return on security j. Assume the CAPM is correct and that the market...

ci. You have been provided the following data on three securities and the market portfolio. Beta 1.5 Observed (Realized) Return 15.0% 12.0% 10.0% 10.0% 5.0% Security/Portfolio Security 1 Security 2 Security 3 Market portfolio Riskfree security Standard Deviation 01 18.0% 2.0% 4.0% 0.0% Correlation 1.0 0.4 P3, m B2 0.5 Pin, m Bm Pem BE Note that the return in the above table is the average realized return on security j. Assume the CAPM is correct and that the market...

6. You have been provided with the following data on three firms and the market: Security...

6. You have been provided with the following data on three firms and the market: Security σι Pi.M 0.90 1.10 0.12 Firm A ii] 0.24 0.4 Firm B iii] 0.75 Firm C [iv] 0 0.10 The Market The risk-free asset vi] 0.01 Fill in the missing values (i-vi) in the table.

6. You have been provided with the following data on three firms and the market: Security σι Pi.M 0.90 1.10 0.12 Firm A ii] 0.24 0.4 Firm B iii] 0.75 Firm C [iv] 0 0.10 The Market The risk-free asset vi] 0.01 Fill in the missing values (i-vi) in the table.

Capital Asset Pricing model

a. Fill in the missing values in the table. b. Is the stock of Firm A correctly priced according to the capital-asset-pricing model (CAPM)? What about the stock ofFirm B? Firm C? If these securities are not correctly priced, what is your investment recommendation for someone with a well-diversified portfolio?You have been provided the following data on the securities of three firms, the market portfolio, and the risk-free asset:Security Expected Return Standard Deviation Correlation BetaFirm A 0.13 0.12 ? 0.9Firm...

A portfolio that combines the risk-free asset and the market portfolio has an expected return of...

A portfolio that combines the risk-free asset and the market portfolio has an expected return of 9 percent and a standard deviation of 16 percent. The risk-free rate is 4.1 percent and the expected return on the market portfolio is 11 percent. Assume the capital asset pricing model holds. What expected rate of return would a security earn if it had a .38 correlation with the market portfolio and a standard deviation of 60 percent?

A portfolio that combines the risk-free asset and the market portfolio has an expected return of 9 percent and a standard deviation of 16 percent. The risk-free rate is 4.1 percent and the expected return on the market portfolio is 11 percent. Assume the capital asset pricing model holds. What expected rate of return would a security earn if it had a .38 correlation with the market portfolio and a standard deviation of 60 percent?

You have been provided the following data about the securities of three firms, the market portfolio, and the risk-free asset: a. Fill in the missing values in the table. (Leave no cells blank - be certain to enter o wherever required. Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Expected Return Standard Deviation Security Correlation* Beta Firm A 0.120 0.21 0.96 Firm B 0.40 0.130 1.51 Firm C The market portfolio 0.111 0.76...

You have been provided the following data about the securities of three firms, the market portfolio, and the risk-free asset: a. Fill in the missing values in the table. (Leave no cells blank - be certain to enter o wherever required. Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Expected Return Standard Deviation Security Correlation* Beta Firm A 0.120 0.21 0.96 Firm B 0.40 0.130 1.51 Firm C The market portfolio 0.111 0.76...

You have been provided the following data about the securities

of three firms, the market portfolio, and the risk-free asset:

a. Fill in the missing values in the table. (Leave no cells

blank - be certain to enter 0 wherever required. Do not round

intermediate calculations and round your answers to 2 decimal

places, e.g., 32.16.)

b-1. What is the expected return of Firm A? (Do not round

intermediate calculations and enter your answer as a percent

rounded to 2...

You have been provided the following data about the securities

of three firms, the market portfolio, and the risk-free asset:

a. Fill in the missing values in the table. (Leave no cells

blank - be certain to enter 0 wherever required. Do not round

intermediate calculations and round your answers to 2 decimal

places, e.g., 32.16.)

b-1. What is the expected return of Firm A? (Do not round

intermediate calculations and enter your answer as a percent

rounded to 2...

You have been provided the following data about the securities of three firms, the market portfolio, and the risk-free asset a. Fill in the missing values in the table. (Leave no cells blank.be certain to enter 0 wherever required. Do not round Intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Correlation Security FA Expected Return Standard Deviation 0.102 033 0.1421 0.162 0.63 0.12 .191 0.08 0.37 Firm The market portfolio The risk tree ass * With...

You have been provided the following data about the securities of three firms, the market portfolio, and the risk-free asset a. Fill in the missing values in the table. (Leave no cells blank.be certain to enter 0 wherever required. Do not round Intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Correlation Security FA Expected Return Standard Deviation 0.102 033 0.1421 0.162 0.63 0.12 .191 0.08 0.37 Firm The market portfolio The risk tree ass * With...

6. You have been provided the following data on the securities of three firms and the market: Et Security BI P/m Firm A 0.13 0.12 0.9 Firm B 0.16 0.40 1.10 Firm C 0.25 0.24 0.75 ? Market Risk-free 0.15 0.10 0.05 Assume the CAPM holds true. Fill in the missing values in the table. a. What is your investment recommendation on each asset? Buy or sell? b. Suppose that you are currently holding a portfolio consisting of Firm B...

6. You have been provided the following data on the securities of three firms and the market: Et Security BI P/m Firm A 0.13 0.12 0.9 Firm B 0.16 0.40 1.10 Firm C 0.25 0.24 0.75 ? Market Risk-free 0.15 0.10 0.05 Assume the CAPM holds true. Fill in the missing values in the table. a. What is your investment recommendation on each asset? Buy or sell? b. Suppose that you are currently holding a portfolio consisting of Firm B...

ci. You have been provided the following data on three securities and the market portfolio. Beta 1.5 Observed (Realized) Return 15.0% 12.0% 10.0% 10.0% 5.0% Security/Portfolio Security 1 Security 2 Security 3 Market portfolio Riskfree security Standard Deviation 01 18.0% 2.0% 4.0% 0.0% Correlation 1.0 0.4 P3, m B2 0.5 Pin, m Bm Pem BE Note that the return in the above table is the average realized return on security j. Assume the CAPM is correct and that the market...

ci. You have been provided the following data on three securities and the market portfolio. Beta 1.5 Observed (Realized) Return 15.0% 12.0% 10.0% 10.0% 5.0% Security/Portfolio Security 1 Security 2 Security 3 Market portfolio Riskfree security Standard Deviation 01 18.0% 2.0% 4.0% 0.0% Correlation 1.0 0.4 P3, m B2 0.5 Pin, m Bm Pem BE Note that the return in the above table is the average realized return on security j. Assume the CAPM is correct and that the market...

6. You have been provided with the following data on three firms and the market: Security σι Pi.M 0.90 1.10 0.12 Firm A ii] 0.24 0.4 Firm B iii] 0.75 Firm C [iv] 0 0.10 The Market The risk-free asset vi] 0.01 Fill in the missing values (i-vi) in the table.

6. You have been provided with the following data on three firms and the market: Security σι Pi.M 0.90 1.10 0.12 Firm A ii] 0.24 0.4 Firm B iii] 0.75 Firm C [iv] 0 0.10 The Market The risk-free asset vi] 0.01 Fill in the missing values (i-vi) in the table.

A portfolio that combines the risk-free asset and the market portfolio has an expected return of 9 percent and a standard deviation of 16 percent. The risk-free rate is 4.1 percent and the expected return on the market portfolio is 11 percent. Assume the capital asset pricing model holds. What expected rate of return would a security earn if it had a .38 correlation with the market portfolio and a standard deviation of 60 percent?

A portfolio that combines the risk-free asset and the market portfolio has an expected return of 9 percent and a standard deviation of 16 percent. The risk-free rate is 4.1 percent and the expected return on the market portfolio is 11 percent. Assume the capital asset pricing model holds. What expected rate of return would a security earn if it had a .38 correlation with the market portfolio and a standard deviation of 60 percent?

Most questions answered within 3 hours.

-

True or False: Spinal nerves emerging from the vertebral column

are ONLY motor OR sensory.

Select...

asked 15 seconds ago -

Thanks so much for the help! Please show all work.

A uniform solid disk with radius...

asked 1 second from now -

Please use Logicly!

Create a 4 bit sequential counter that is capable of counting up

or...

asked 8 minutes ago -

I1(t) and I2(t) describe the intensity of two

light waves.

I1(t)= 10sin(30t+π/4)

I2(t)=

10sin(30.4t+π)

Assume that...

asked 13 minutes ago -

A sample of steam with a mass of 0.501 g at a temperature of 100

∘C...

asked 18 minutes ago -

A block sits on the floor. (a) What is the magnitude of the

frictional force on...

asked 19 minutes ago -

state one specific part from disability law such as ADA

(Americans with Disability Acts) or policy...

asked 20 minutes ago -

please simplify how vapor pressure lowering is related to a

rise in the boiling point solution

asked 35 minutes ago -

write a java program that does the following

Part one

Use a For loop to compute...

asked 32 minutes ago -

"A student in another class made a claim that many people are

now talking about outlawing...

asked 34 minutes ago -

Test the hypothesis using P-value approach. Be sure to verify

the requirements of the test.

H0:...

asked 1 hour ago -

For a voltaic cell based on the reaction below, which statement

is correct?

Zn(s)+2H+(aq)→Zn2+(aq)+H2(g)

Zn2+(aq) is...

asked 1 hour ago