LOL (the “Company”), an SEC registrant with a calendar year-end, is a manufacturer and distributor of sports equipment. The Company was created in 1989 and is headquartered in Southern California. The Company has manufacturing operations and numerous sales and administrative locations in the United States. LOL files a consolidated U.S. federal tax return. (This case will not consider the evaluation of the state jurisdictions; it will only consider the federal jurisdiction.)

As LOL’s auditors, you are now performing the Company’s year-end audit for the fiscal year ended December 31, 2010, and have the following information available to you:

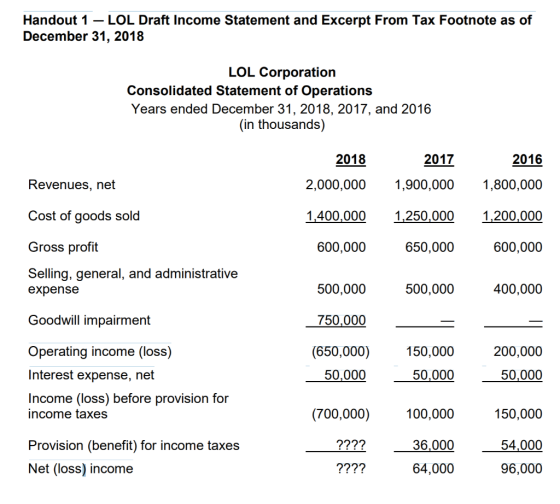

• LOL draft income statement and excerpt from tax footnote as of December 31, 2010 (Handout 1).

• A deferred tax asset realization analysis showing pre-tax book income projections (Handout 2).

• The projected income schedule (realization analysis above) projects organic growth beginning in 2012 after stemming the decrease in pre-tax book income.

• LOL does not have the ability to carry back any losses to prior periods. • A significant customer declared bankruptcy in 2010; therefore, the Company wrote off all accounts receivable from this customer. The Company is considering the exclusion of such expense when evaluating whether future income is objectively verifiable.

• The Company does not have a history of operating losses or tax credit carryforwards expiring unused.

• The Company has identified the following possible tax-planning strategies: o Selling and leasing back manufacturing equipment that would result in a taxable gain of $20 million. o Selling the primary manufacturing facility at a gain to offset existing capital loss carryforwards.

Required:

• Question 2 — How much of the reversing taxable temporary differences may be considered in estimating future taxable income?

LOL Corporation Inventory of Deferred Tax Balances The components of net deferred income taxes are as follows: 2018 2017 Year ended December 31 (in thousands) Deferred income tax assets: Allowance for doubtful accounts 30,000 25,000 Tax loss carryforwards (pre-2018) 100,000 100,000 20,000 Accruals and other 25,000 150,000 150,000 Deferred income tax liabilities: (15,000) (20,000) Depreciation Indefinite lived intangible assets (trademark) (50,000) (50,000) (35,000 (20,000) (100,000) (90,000) Prepaid expenses Net deferred income taxes 60,000 50,000 Valuation allowance Net deferred tax asset (liability) 2??260,000 As of December 31, 2018, LOL had $475 million of net operating loss carryforwards. Of these, $25 million are capital losses and will expire in 2019, and the remaining $450 million are operating losses and will expire in 2033

Handout 2- LOL Deferred Tax Asset Realization Analysis Showing Pretax Book Income Projections LOL Corporation Deferred Tax Asset Realization Analysis in thousands) The documentation below was provided to auditors as part of their audit. Adjusted Pretax Book Goodwill Pretax Book Year Income (Loss) Impairment*Income (Loss Actual Results 2016 150,000 150,000 2017 100,000 100,000 2018 700,000 750,000 50,000 Projections 2019 2020 40,000 2021 80,000 85,000 90,000 2022 2023 2024 2025 95,000 100,000 2026 105,000 110,000 2027 2028 115,000 2029 120,000 The goodwill impaired is nondeductible. There was no basis in the goodwill for tax purposes, therefore, the impairment had no direct impact on the tax provision. In other words, the impairment of the goodwill for book purposes does not result in a corresponding deduction for tax purposes in any period. The book expense, therefore, does not affect the resulting taxes payable, and it results in an effective tax rate that differs (unfavorably) from the statutory tax rate

Homework Answers

Add Answer to:

LOL (the “Company”), an SEC registrant with a calendar year-end, is a manufacturer and distributor of sports equipment....

year. mone lax expense for the year assumi or the year assuming that the tax rate...

year. mone lax expense for the year assumi or the year assuming that the tax rate is 40% this year and 50% starting next (3) Prepare the income tax expense section of the income statement, beginning with "Income before income taxes. (4) Indicate how deferred income taxes should be presented on the balance sheet. Problem 3. Walsh Services computed pretax financial income of $220,000 for 2017 and $288,000 for 2018. In preparing the income tax return for the year, the...

year. mone lax expense for the year assumi or the year assuming that the tax rate is 40% this year and 50% starting next (3) Prepare the income tax expense section of the income statement, beginning with "Income before income taxes. (4) Indicate how deferred income taxes should be presented on the balance sheet. Problem 3. Walsh Services computed pretax financial income of $220,000 for 2017 and $288,000 for 2018. In preparing the income tax return for the year, the...

Your answer is partially correct. The pretax financial income (or loss) figures for Jenny Spangler Company...

Your answer is partially correct. The pretax financial income (or loss) figures for Jenny Spangler Company are as follows. 2015 2016 2017 2018 2019 2020 2021 $160,000 250,000 80,000 (160,000) (380,000) 120,000 100,000 Pretax financial income (or loss) and taxable income (loss) were the same for all years involved. Assume a 25% tax rate for 2015 and 2016 and a 20% tax rate for the remaining years. Prepare the journal entries for the years 2017 to 2021 to record income...

Your answer is partially correct. The pretax financial income (or loss) figures for Jenny Spangler Company are as follows. 2015 2016 2017 2018 2019 2020 2021 $160,000 250,000 80,000 (160,000) (380,000) 120,000 100,000 Pretax financial income (or loss) and taxable income (loss) were the same for all years involved. Assume a 25% tax rate for 2015 and 2016 and a 20% tax rate for the remaining years. Prepare the journal entries for the years 2017 to 2021 to record income...

Exercise 19-8 Sunland Company has the following two temporary differences between its income tax expense and...

Exercise 19-8 Sunland Company has the following two temporary differences between its income tax expense and income taxes payable. 2017 2018 2019 Pretax financial income $811,000 $932,000 $992,000 Excess depreciation expense on tax return (31,500 ) (39,100 ) (9,900 ) Excess warranty expense in financial income 19,900 9,800 8,300 Taxable income $799,400 $902,700 $990,400 The income tax rate for all years is 40%. Assuming there were no temporary differences prior to 2017, prepare the journal entry to record income tax...

Question 12 --/1 View Policies Current Attempt in Progress Novak Co. establishes a $136,000,000 liability at the end of...

Question 12 --/1 View Policies Current Attempt in Progress Novak Co. establishes a $136,000,000 liability at the end of 2017 for the estimated site-cleanup costs at two of its manufacturing facilities. All related closing costs will be paid and deducted on the tax return in 2018. Also, at the end of 2017, the company has $68,000,000 of temporary differences due to excess depreciation for tax purposes, $9,520,000 of which will reverse in 2018. The enacted tax rate for all years...

Question 12 --/1 View Policies Current Attempt in Progress Novak Co. establishes a $136,000,000 liability at the end of 2017 for the estimated site-cleanup costs at two of its manufacturing facilities. All related closing costs will be paid and deducted on the tax return in 2018. Also, at the end of 2017, the company has $68,000,000 of temporary differences due to excess depreciation for tax purposes, $9,520,000 of which will reverse in 2018. The enacted tax rate for all years...

Crane Co. establishes a $142,000,000 liability at the end of 2017 for the estimated site-cleanup costs at tw...

Crane Co. establishes a $142,000,000 liability at the end of

2017 for the estimated site-cleanup costs at two of its

manufacturing facilities. All related closing costs will be paid

and deducted on the tax return in 2018. Also, at the end of 2017,

the company has $71,000,000 of temporary differences due to excess

depreciation for tax purposes, $9,940,000 of which will reverse in

2018.

The enacted tax rate for all years is 40%, and the company pays

taxes of $90,880,000...

Crane Co. establishes a $142,000,000 liability at the end of

2017 for the estimated site-cleanup costs at two of its

manufacturing facilities. All related closing costs will be paid

and deducted on the tax return in 2018. Also, at the end of 2017,

the company has $71,000,000 of temporary differences due to excess

depreciation for tax purposes, $9,940,000 of which will reverse in

2018.

The enacted tax rate for all years is 40%, and the company pays

taxes of $90,880,000...

please explain this in proper english. i can't undestand the answers that is up for this...

please explain this in proper english. i can't undestand the

answers that is up for this question on here

Financial Statement Analysis Case Homestake Mining Company Homestake Mining Company is a 120-year-old international gold mining company with substantial gold mining operations and exploration in the United States, Canada, and Australia. At year-end, Homestake reported the following items related to income taxes (thousands of dollars). Total current taxes Total deferred taxes Total income and mining taxes (the provision for taxes per...

please explain this in proper english. i can't undestand the

answers that is up for this question on here

Financial Statement Analysis Case Homestake Mining Company Homestake Mining Company is a 120-year-old international gold mining company with substantial gold mining operations and exploration in the United States, Canada, and Australia. At year-end, Homestake reported the following items related to income taxes (thousands of dollars). Total current taxes Total deferred taxes Total income and mining taxes (the provision for taxes per...

Assignment 5 USE GAAP CODIFICATIONS At December 31, 2017, Acme Inc. had the following deferred tax...

Assignment 5

USE GAAP CODIFICATIONS

At December 31, 2017, Acme Inc. had the following deferred tax

balances:

Deferred tax

liability

$ 62,500

Deferred tax

asset

100,000

Valuation

allowance

40,000

These deferred tax balances relate to two items. First, Acme has

recorded excess tax deductions related to its plant assets. At

December 31, 2017, plant assets had a book value of $1,000,000 and

a tax basis of $750,000. Second, Acme had a NOL carryforward in the...

Assignment 5

USE GAAP CODIFICATIONS

At December 31, 2017, Acme Inc. had the following deferred tax

balances:

Deferred tax

liability

$ 62,500

Deferred tax

asset

100,000

Valuation

allowance

40,000

These deferred tax balances relate to two items. First, Acme has

recorded excess tax deductions related to its plant assets. At

December 31, 2017, plant assets had a book value of $1,000,000 and

a tax basis of $750,000. Second, Acme had a NOL carryforward in the...

2) At the end of 2017, Hoover company had reported a deferred tax asset of $72...

2) At the end of 2017, Hoover company had reported a deferred tax asset of $72 million with no valuation allowance. At December 31, 2018, the account balances of Hoover showed a deferred tax asset of $80 million before assessing the need for a valuation allowance and income taxes payable of $56 million. Hoover determined that it was more likely than not that 20% of the deferred tax asset ultimately would not be realized. Hoover made no estimated tax payuments...

2) At the end of 2017, Hoover company had reported a deferred tax asset of $72 million with no valuation allowance. At December 31, 2018, the account balances of Hoover showed a deferred tax asset of $80 million before assessing the need for a valuation allowance and income taxes payable of $56 million. Hoover determined that it was more likely than not that 20% of the deferred tax asset ultimately would not be realized. Hoover made no estimated tax payuments...

Able purchased a machine for $150,000 on March 1, 2017. The asset has a 5 year life and a $30,000 salvage value. Th...

Able purchased a machine for $150,000 on March 1, 2017. The asset has a 5 year life and a $30,000 salvage value. The half year assumption will be used for financial and tax depreciation. Financial reporting will use straight-line depreciation, DDBX (double declining with a switch to straight) will be used for tax purposes. Calculate depreciation for 2017 and 2018 in the space provided below: 2020 2018 2017 Straight line DDBX Assume that income prior to considering tax and depreciation...

Able purchased a machine for $150,000 on March 1, 2017. The asset has a 5 year life and a $30,000 salvage value. The half year assumption will be used for financial and tax depreciation. Financial reporting will use straight-line depreciation, DDBX (double declining with a switch to straight) will be used for tax purposes. Calculate depreciation for 2017 and 2018 in the space provided below: 2020 2018 2017 Straight line DDBX Assume that income prior to considering tax and depreciation...

Yarman Inc. began business on January 1, 2017. Its pretax financial income for the first 2...

Yarman Inc. began business on January 1, 2017. Its pretax financial income for the first 2 years was as follows: 2007 240,000 2008 560,000 The following items caused the only differences between pretax financial income and taxable income. 1. In 2017, the company collected 180,000 of rent; of this amount, 60,000 was earned in 2017; the other 120,000 will be earned equally over the 2018-2019 period. The full 180,000 was included in taxable income in 2017. 2. The company pays...

year. mone lax expense for the year assumi or the year assuming that the tax rate is 40% this year and 50% starting next (3) Prepare the income tax expense section of the income statement, beginning with "Income before income taxes. (4) Indicate how deferred income taxes should be presented on the balance sheet. Problem 3. Walsh Services computed pretax financial income of $220,000 for 2017 and $288,000 for 2018. In preparing the income tax return for the year, the...

year. mone lax expense for the year assumi or the year assuming that the tax rate is 40% this year and 50% starting next (3) Prepare the income tax expense section of the income statement, beginning with "Income before income taxes. (4) Indicate how deferred income taxes should be presented on the balance sheet. Problem 3. Walsh Services computed pretax financial income of $220,000 for 2017 and $288,000 for 2018. In preparing the income tax return for the year, the...

Your answer is partially correct. The pretax financial income (or loss) figures for Jenny Spangler Company are as follows. 2015 2016 2017 2018 2019 2020 2021 $160,000 250,000 80,000 (160,000) (380,000) 120,000 100,000 Pretax financial income (or loss) and taxable income (loss) were the same for all years involved. Assume a 25% tax rate for 2015 and 2016 and a 20% tax rate for the remaining years. Prepare the journal entries for the years 2017 to 2021 to record income...

Your answer is partially correct. The pretax financial income (or loss) figures for Jenny Spangler Company are as follows. 2015 2016 2017 2018 2019 2020 2021 $160,000 250,000 80,000 (160,000) (380,000) 120,000 100,000 Pretax financial income (or loss) and taxable income (loss) were the same for all years involved. Assume a 25% tax rate for 2015 and 2016 and a 20% tax rate for the remaining years. Prepare the journal entries for the years 2017 to 2021 to record income...

Question 12 --/1 View Policies Current Attempt in Progress Novak Co. establishes a $136,000,000 liability at the end of 2017 for the estimated site-cleanup costs at two of its manufacturing facilities. All related closing costs will be paid and deducted on the tax return in 2018. Also, at the end of 2017, the company has $68,000,000 of temporary differences due to excess depreciation for tax purposes, $9,520,000 of which will reverse in 2018. The enacted tax rate for all years...

Question 12 --/1 View Policies Current Attempt in Progress Novak Co. establishes a $136,000,000 liability at the end of 2017 for the estimated site-cleanup costs at two of its manufacturing facilities. All related closing costs will be paid and deducted on the tax return in 2018. Also, at the end of 2017, the company has $68,000,000 of temporary differences due to excess depreciation for tax purposes, $9,520,000 of which will reverse in 2018. The enacted tax rate for all years...

Crane Co. establishes a $142,000,000 liability at the end of

2017 for the estimated site-cleanup costs at two of its

manufacturing facilities. All related closing costs will be paid

and deducted on the tax return in 2018. Also, at the end of 2017,

the company has $71,000,000 of temporary differences due to excess

depreciation for tax purposes, $9,940,000 of which will reverse in

2018.

The enacted tax rate for all years is 40%, and the company pays

taxes of $90,880,000...

Crane Co. establishes a $142,000,000 liability at the end of

2017 for the estimated site-cleanup costs at two of its

manufacturing facilities. All related closing costs will be paid

and deducted on the tax return in 2018. Also, at the end of 2017,

the company has $71,000,000 of temporary differences due to excess

depreciation for tax purposes, $9,940,000 of which will reverse in

2018.

The enacted tax rate for all years is 40%, and the company pays

taxes of $90,880,000...

please explain this in proper english. i can't undestand the

answers that is up for this question on here

Financial Statement Analysis Case Homestake Mining Company Homestake Mining Company is a 120-year-old international gold mining company with substantial gold mining operations and exploration in the United States, Canada, and Australia. At year-end, Homestake reported the following items related to income taxes (thousands of dollars). Total current taxes Total deferred taxes Total income and mining taxes (the provision for taxes per...

please explain this in proper english. i can't undestand the

answers that is up for this question on here

Financial Statement Analysis Case Homestake Mining Company Homestake Mining Company is a 120-year-old international gold mining company with substantial gold mining operations and exploration in the United States, Canada, and Australia. At year-end, Homestake reported the following items related to income taxes (thousands of dollars). Total current taxes Total deferred taxes Total income and mining taxes (the provision for taxes per...

Assignment 5

USE GAAP CODIFICATIONS

At December 31, 2017, Acme Inc. had the following deferred tax

balances:

Deferred tax

liability

$ 62,500

Deferred tax

asset

100,000

Valuation

allowance

40,000

These deferred tax balances relate to two items. First, Acme has

recorded excess tax deductions related to its plant assets. At

December 31, 2017, plant assets had a book value of $1,000,000 and

a tax basis of $750,000. Second, Acme had a NOL carryforward in the...

Assignment 5

USE GAAP CODIFICATIONS

At December 31, 2017, Acme Inc. had the following deferred tax

balances:

Deferred tax

liability

$ 62,500

Deferred tax

asset

100,000

Valuation

allowance

40,000

These deferred tax balances relate to two items. First, Acme has

recorded excess tax deductions related to its plant assets. At

December 31, 2017, plant assets had a book value of $1,000,000 and

a tax basis of $750,000. Second, Acme had a NOL carryforward in the...

2) At the end of 2017, Hoover company had reported a deferred tax asset of $72 million with no valuation allowance. At December 31, 2018, the account balances of Hoover showed a deferred tax asset of $80 million before assessing the need for a valuation allowance and income taxes payable of $56 million. Hoover determined that it was more likely than not that 20% of the deferred tax asset ultimately would not be realized. Hoover made no estimated tax payuments...

2) At the end of 2017, Hoover company had reported a deferred tax asset of $72 million with no valuation allowance. At December 31, 2018, the account balances of Hoover showed a deferred tax asset of $80 million before assessing the need for a valuation allowance and income taxes payable of $56 million. Hoover determined that it was more likely than not that 20% of the deferred tax asset ultimately would not be realized. Hoover made no estimated tax payuments...

Able purchased a machine for $150,000 on March 1, 2017. The asset has a 5 year life and a $30,000 salvage value. The half year assumption will be used for financial and tax depreciation. Financial reporting will use straight-line depreciation, DDBX (double declining with a switch to straight) will be used for tax purposes. Calculate depreciation for 2017 and 2018 in the space provided below: 2020 2018 2017 Straight line DDBX Assume that income prior to considering tax and depreciation...

Able purchased a machine for $150,000 on March 1, 2017. The asset has a 5 year life and a $30,000 salvage value. The half year assumption will be used for financial and tax depreciation. Financial reporting will use straight-line depreciation, DDBX (double declining with a switch to straight) will be used for tax purposes. Calculate depreciation for 2017 and 2018 in the space provided below: 2020 2018 2017 Straight line DDBX Assume that income prior to considering tax and depreciation...

Most questions answered within 3 hours.

-

Find the force, in N, required to tow a plate (0.5 m x 2 m) at...

asked 1 second from now -

Eagle Industries feels that a lockbox system can shorten its

accounts receivable collection period by 2...

asked 16 minutes ago -

A block measures 5.5 cm on each side. What is the volume of the

block in...

asked 15 minutes ago -

what are the differences between these?

a. shear force.

b. shear stress.

c. Bending Moment.

d....

asked 25 minutes ago -

The proportion of adult women in a certain geographical region

is approximately 51%. A marketing survey...

asked 32 minutes ago -

I am trying to answer a question that is asking why there was no

evidence of...

asked 43 minutes ago -

Power elecrtonics: buck converter?

Calculate and plot (via excel/MATLAB) the average V(out) of a

buck converter...

asked 44 minutes ago -

PLEASE USE PYTHON

training error should strictly decrease as the degree of the

hypothesis polynomials increases....

asked 49 minutes ago -

Using the Table and data below, create a procedure that accepts

product ID as a parameter...

asked 51 minutes ago -

Suppose X follows an exponential distribution with mean 7.5.

Determine the conditional probability P(x > 2.5...

asked 1 hour ago -

Young softball batters are often instructed to “choke-up on the

bat” by their coach. In terms...

asked 1 hour ago -

Suppose that you are an official with Mexico's economic

development agency. Write a one-page memo detailing...

asked 1 hour ago