Product Costing: Department Versus ABC for Overhead

Advertising Technologies, Inc. (ATI) specializes in providing both published and online advertising services for the business marketplace. The company monitors its costs based on the cost per column inch of published space printed in print advertising media and based on the cost per minute of telephor advertising time delivered on "The AD Line," a computer-based, online advertising service. ATI has one new competitor, Tel-a-Ad, in its local teleadvertising market; and with increased competition, ATI has seen a decline in sales of online advertising in recent years. ATI's president, Robert Beard, believes that predatory pricing by Tel-a-A has caused the problem. The following is a recent conversation between Robert and Jane Minnear, director of marketing for ATI.

Jane: I just received a call from one of our major customers concerning our advertising rates on "The AD Line" who said that a sales rep from another firm (it had to be Tel-a-Ad) had offered the same service at $1 per minute, which is $1.50 per minute less than our price.

Robert: It's costing about $1.35 per minute to produce that product. I don't see how they can afford to sell it so cheaply. I'm not convinced that we should meet the price. Perhaps the better strategy is to emphasize producing and selling more published ads, which we're more experienced with and where our margins are high and we have virtually no competition.

Jane: You may be right. Based on a recent survey of our customers, I think we can raise the price significantly for published advertising and still not lose business.

Robert: That sounds promising; however, before we make a major recommitment to publishing, let's explore other possible explanations. I want to know how our costs compare with our competitors. Maybe we could be more efficient and find a way to earn a good return on teleadvertising.

After this meeting, Robert and Jane requested an investigation of production costs and comparative efficiency of producing published versus online advertising services. The controller, Tim Gentry, indicated that ATI's efficiency was comparable to that of its competitors and prepared the following cost data:

Published Advertising Online Advertising Estimated number of production units 200,000 10,000,000 Selling price $200 $2.50 Direct product costs $21,000,000 $5,000,000 Overhead allocation* $10,780,000 $8,470,000 Overhead per unit $54 $0.85 Direct costs per unit $105 $0.50 Number of customers 180,000 25,000 Number of salesperson days 32,000 5,500 Number of art and design hours 35,000 5,000 Number of creative services subcontract hours 100,000 25,000 Number of customer service calls 72,000 8,000 *Based on direct labor costs

Upon examining the data, Robert decided that he wanted to know more about the overhead costs because they were such a high proportion of total production costs. He was provided the following list of overhead costs and told that they were currently being assigned to products in proportion to direct labor costs.

Selling costs $8,250,000 Visual and audio design costs 3,300,000 Creative services costs 5,500,000 Customer service costs 2,200,000

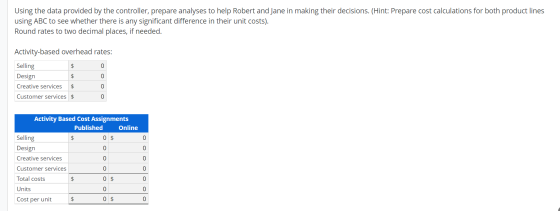

Using the data provided by the controller, prepare analyses to help Robert and Jane in making their decisions. (Hint: Prepare cost calculations for both product lines using ABC to see whether there is any significant difference in their unit costs). Round rates to two decimal places, if needed.

Homework Answers

Activity Based Overheads Rates

| Activity | Amount in $ |

| Selling ($8,250,000/37,500) | 220 |

| Design ($3,300,000/40,000) | 82.50 |

| Creative Services($5,500,000/125,000) | 44 |

| Customer Services ($2,200,000/80,000) | 27.50 |

| Activity Based Cost Assignment | ||

| Published ($) | Online($) | |

| A. Selling | 7,040,000 | 1,210,000 |

| B. Design | 2,887,500 | 4,12,500 |

| C. Creative Services | 4,400,000 | 1,100,000 |

| D. Customer Services | 1,980,000 | 220,000 |

| E. Total Cost (A+B+C+D) | 16,307,500 | 2,942,500 |

| F. Units | 200,000 | 10,000,000 |

| G. Cost per Unit (E/F) | 81.54 | 0.30 |

| Total Production Cost per Unit Comparison | ||

| Published ($) | Online ($) | |

| Cost Using ABC (Direct Cost+Overhead Per Unit) | 186.54 | 0.80 |

| Cost using Traditional(Direct Cost+Overhead Per Unit) | 159.00 | 1.35 |

| Difference | 27.54 | -0.55 |

| Solution:- | ||||||

| Determining cost of each product line using activity based costing:- | ||||||

| Overhead rate based on activity based costing | ||||||

| Particulars | Cost (A) | Driver (B) | Overhead rate (A/B) | |||

| Selling costs | $7,500,000 | Number of sales person days | 37500 | $200 | ||

| Visual and audio design costs | $3,000,000 | Number of art and design hours | 40000 | $75 | ||

| Creative services costs | $5,000,000 | Number of creative services subcontract hours | 125000 | $40 | ||

| Customer service costs | $2,000,000 | Number of customer service calls | 80000 | $25 | ||

| Cost of each product product line as per ABC method:- | ||||||

| Published advertisement | Online Advertisement | |||||

| Cost driver | Rate | Amt. | Cost driver | Rate | Amt. | |

| Direct product costs | $21,000,000 | $5,000,000 | ||||

| Overheads:- | ||||||

| Selling costs | 32000 | $200 | $6,400,000 | 5500 | $200 | $1,100,000 |

| Visual and audio design costs | 35000 | $75 | $2,625,000 | 5000 | $75 | $375,000 |

| Creative services costs | 100000 | $40 | $4,000,000 | 25000 | $40 | $1,000,000 |

| Customer service costs | 72000 | $25 | $1,800,000 | 8000 | $25 | $200,000 |

| Total costs as per ABC method | $35,825,000 | $7,675,000 | ||||

| ÷ Total units | 200000 | 10000000 | ||||

| Cost per unit | $179.13 | $0.77 | ||||

| Cost of each product product line as per traditional method:- | ||||||

| Published Advertisement | Online Advertisement | |||||

| Direct product costs | $21,000,000 | $5,000,000 | ||||

| Overhead (Traditional method) | $9,800,000 | $7,700,000 | ||||

| Total cost (Traditional method) | $30,800,000 | $12,700,000 | ||||

| ÷ Total units | 200000 | 10000000 | ||||

| Cost per unit | $154 | $1.27 | ||||

| Difference between costs of each product line as per ABC method and traditional method:- | ||||||

| Product | Cost per unit as per ABC method (A) | Cost per unit as per Traditional method (B) | Under charged/(Excess charged) | |||

| Published Advertisement | $179.13 | $154.00 | $25.13 | |||

| Online Advertisement | $0.77 | $1.27 | $(0.50) | |||

| Because of using traditional costing the cost of both the product line is not calculated properly, cost of product as per ABC is considered more appropriate and accurate. ABC method assigns cost to each product in the most reasonable manner i.e. on the basis of actual incurrance of a particular expense on each product. In the present case company is planning to discontinue online advertisement because its competitor is offering it for $1 per unit whereas they are selling it for $1.5 per unit. Now they were discontinuing this line because as per traditional method cost of this product line is $1.27 per unit whereas it is $0.77 per unit in reality. Thus ATI should not switch from fast growing online advertising market back into the well established published market and the charge of predatory pricing is not valid as per the table above and the reason why customers are demanding more of published advertisement is that it is charging less for this product as compared to what seems to be a valid charge for this service. No the result of traditional costing and ABC costing is not same. | ||||||

Add Answer to:

Product Costing: Department Versus ABC for Overhead Advertising Technologies, Inc. (ATI) specializes in providing both published...

Product Costing: Department Versus ABC for Overhead Advertising Technologies, Inc. (ATI) specializes in providing both p...

Product Costing: Department Versus ABC for Overhead Advertising Technologies, Inc. (ATI) specializes in providing both published and online advertising services for the business marketplace. The company monitors its costs based on the cost per column inch of published space printed in print advertising media and based on the cost per minute of telephone advertising time delivered on "The AD Line," a computer-based, online advertising service. ATI has one new competitor, Tel-a-Ad, in its local teleadvertising market; and with increased competition,...

Product-Costing Accuracy, Corporate Strategy, ABC Autotech Manufacturing is engaged in the production of replacement parts for...

Product-Costing Accuracy, Corporate Strategy, ABC Autotech Manufacturing is engaged in the production of replacement parts for automobiles. One plant specializes in the production of two parts: Part #127 and Part #234. Part #127 produced the highest volume of activity, and for many years it was the only part produced by the plant. Five years ago, Part #234 was added. Part #234 was more difficult to manufacture and required special tooling and setups. Profits increased for the first three years after...

E17.10 Assign overhead using traditional costing and ABC. (LO 1, 2, 3), AP Kragan Clothing Company...

E17.10 Assign overhead using traditional costing and ABC. (LO 1, 2, 3), AP Kragan Clothing Company manufactures its own designed and labeled athletic wear and sells its products through catalog sales and retail outlets. While Kragan has for years used activity-based costing in its manufacturing activities, it has always used traditional costing in assigning its selling costs to its product lines. Selling costs have traditionally been assigned to Kragan's product lines at a rate of 70% of direct materials costs....

E17.10 Assign overhead using traditional costing and ABC. (LO 1, 2, 3), AP Kragan Clothing Company manufactures its own designed and labeled athletic wear and sells its products through catalog sales and retail outlets. While Kragan has for years used activity-based costing in its manufacturing activities, it has always used traditional costing in assigning its selling costs to its product lines. Selling costs have traditionally been assigned to Kragan's product lines at a rate of 70% of direct materials costs....

overhead sing onal costing and ABC 3 AP E17.10 Kragan Clothing Company manufactures its own designed...

overhead sing onal costing and ABC 3 AP E17.10 Kragan Clothing Company manufactures its own designed and labeled athletic wear and sells its products through catalog sales and retail outlets. While Kragan has for years used activity-based costing in its manufacturing activities, it has always used traditional costing in assigning its selline costs to its product lines. Selling costs have traditionally been assigned to Kragan's product lines at a rate of 70% of direct materials costs. Its direct materials costs...

overhead sing onal costing and ABC 3 AP E17.10 Kragan Clothing Company manufactures its own designed and labeled athletic wear and sells its products through catalog sales and retail outlets. While Kragan has for years used activity-based costing in its manufacturing activities, it has always used traditional costing in assigning its selline costs to its product lines. Selling costs have traditionally been assigned to Kragan's product lines at a rate of 70% of direct materials costs. Its direct materials costs...

Traditional Product Costing versus Activity-Based Costing Ridgeland Inc. makes backpacks for large sporting goods chains that...

Traditional Product Costing versus Activity-Based Costing Ridgeland Inc. makes backpacks for large sporting goods chains that are sold under the customers' store brand names. The Accounting Department has identified the following overhead costs and cost drivers for next year: Overhead Item Expected Costs Cost Driver Maximum Quantity Setup costs $734,400 Number of setups 7,200 Ordering costs 195,000 Number of orders 65,000 Maintenance 1,380,000 Number of machine hours 80,000 Power 132,000 Number of kilowatt hours 440,000 Total predicted direct labor hours...

Traditional Product Costing Versus Activity-Based Costing High Country Outfitters, Inc., makes backpacks for large sporting goods...

Traditional Product Costing Versus Activity-Based Costing High Country Outfitters, Inc., makes backpacks for large sporting goods chains that are sold under the customers' store brand names. The accounting department has identified the following overhead costs and cost drivers for next year: Overhead Item Expected Costs Cost Driver Maximum Quantity Setup costs $1,404,000 Number of setups 7,200 Ordering costs 360,000 Number of orders 60,000 Maintenance 1,200,000 Number of machine hours 80,000 Power 120,000 Number of kilowatt hours 600,000 Total predicted direct...

Health 'R Us, Inc., uses a traditional product costing system to assign overhead costs uniformly to...

Health 'R Us, Inc., uses a traditional product costing system to assign overhead costs uniformly to all its packaged multigrain products. To meet Food and Drug Administration requirements and to assure its customers of safe, sanitary, and nutritious food, Health'R Us engages in a high level of quality control. Health 'R Us assigns its quality-control overhead costs to all products at a rate of 17% of direct labor costs. Its direct labor cost for the month of June for its...

Health 'R Us, Inc., uses a traditional product costing system to assign overhead costs uniformly to all its packaged multigrain products. To meet Food and Drug Administration requirements and to assure its customers of safe, sanitary, and nutritious food, Health'R Us engages in a high level of quality control. Health 'R Us assigns its quality-control overhead costs to all products at a rate of 17% of direct labor costs. Its direct labor cost for the month of June for its...

Activity-Based And Department Rate Product Costing and Product Cost Distortions Black and Blue Sports Inc. manufactures...

Activity-Based And Department Rate Product Costing and Product Cost Distortions Black and Blue Sports Inc. manufactures two products: snowboards and skis. The factory overhead incurred is as follows: Indirect labor Cutting Department Finishing Department $507,000 156,000 192,000 Total $855,000 The activity base associated with the two production departments is direct labor hours. The indirect labor can be assigned to two different activities as follows: Activity Activity Base Budgeted Activity Cost $237,000 270,000 Production control Number of production runs Number of...

Activity-Based And Department Rate Product Costing and Product Cost Distortions Black and Blue Sports Inc. manufactures two products: snowboards and skis. The factory overhead incurred is as follows: Indirect labor Cutting Department Finishing Department $507,000 156,000 192,000 Total $855,000 The activity base associated with the two production departments is direct labor hours. The indirect labor can be assigned to two different activities as follows: Activity Activity Base Budgeted Activity Cost $237,000 270,000 Production control Number of production runs Number of...

Health 'R Us, Inc., uses a traditional product costing system to assign overhead costs uniformly to...

Health 'R Us, Inc., uses a traditional product costing system to assign overhead costs uniformly to all its packaged multigrain products. To meet Food and Drug Administration requirements and to assure its customers of safe, sanitary, and nutritious food, Health 'R Us engages in a high level of quality control. Health R Us assigns its quality control overhead costs to all products at a rate of 17% of direct labor costs. Its direct labor cost for the month of June...

Health 'R Us, Inc., uses a traditional product costing system to assign overhead costs uniformly to all its packaged multigrain products. To meet Food and Drug Administration requirements and to assure its customers of safe, sanitary, and nutritious food, Health 'R Us engages in a high level of quality control. Health R Us assigns its quality control overhead costs to all products at a rate of 17% of direct labor costs. Its direct labor cost for the month of June...

Problem 17-1A Comparing costs using ABC with the plantwide overhead rate LO P1, P3, A1, A2...

Problem 17-1A Comparing costs using ABC with the plantwide overhead rate LO P1, P3, A1, A2 The following data are for the two products produced by Tadros Company Direct materials Direct labor hours Machine hours Batches Volu Engineering modifications Number of customers Market price Product A $15 per unit 0.4 DLH per unit 2.3 MH per unit 115 batches 10,000 units 10 modifications 500 customers $35 per unit Product B 528 per unit 1.6 DLH per unit 1.2 per unit...

Problem 17-1A Comparing costs using ABC with the plantwide overhead rate LO P1, P3, A1, A2 The following data are for the two products produced by Tadros Company Direct materials Direct labor hours Machine hours Batches Volu Engineering modifications Number of customers Market price Product A $15 per unit 0.4 DLH per unit 2.3 MH per unit 115 batches 10,000 units 10 modifications 500 customers $35 per unit Product B 528 per unit 1.6 DLH per unit 1.2 per unit...

E17.10 Assign overhead using traditional costing and ABC. (LO 1, 2, 3), AP Kragan Clothing Company manufactures its own designed and labeled athletic wear and sells its products through catalog sales and retail outlets. While Kragan has for years used activity-based costing in its manufacturing activities, it has always used traditional costing in assigning its selling costs to its product lines. Selling costs have traditionally been assigned to Kragan's product lines at a rate of 70% of direct materials costs....

E17.10 Assign overhead using traditional costing and ABC. (LO 1, 2, 3), AP Kragan Clothing Company manufactures its own designed and labeled athletic wear and sells its products through catalog sales and retail outlets. While Kragan has for years used activity-based costing in its manufacturing activities, it has always used traditional costing in assigning its selling costs to its product lines. Selling costs have traditionally been assigned to Kragan's product lines at a rate of 70% of direct materials costs....

overhead sing onal costing and ABC 3 AP E17.10 Kragan Clothing Company manufactures its own designed and labeled athletic wear and sells its products through catalog sales and retail outlets. While Kragan has for years used activity-based costing in its manufacturing activities, it has always used traditional costing in assigning its selline costs to its product lines. Selling costs have traditionally been assigned to Kragan's product lines at a rate of 70% of direct materials costs. Its direct materials costs...

overhead sing onal costing and ABC 3 AP E17.10 Kragan Clothing Company manufactures its own designed and labeled athletic wear and sells its products through catalog sales and retail outlets. While Kragan has for years used activity-based costing in its manufacturing activities, it has always used traditional costing in assigning its selline costs to its product lines. Selling costs have traditionally been assigned to Kragan's product lines at a rate of 70% of direct materials costs. Its direct materials costs...

Health 'R Us, Inc., uses a traditional product costing system to assign overhead costs uniformly to all its packaged multigrain products. To meet Food and Drug Administration requirements and to assure its customers of safe, sanitary, and nutritious food, Health'R Us engages in a high level of quality control. Health 'R Us assigns its quality-control overhead costs to all products at a rate of 17% of direct labor costs. Its direct labor cost for the month of June for its...

Health 'R Us, Inc., uses a traditional product costing system to assign overhead costs uniformly to all its packaged multigrain products. To meet Food and Drug Administration requirements and to assure its customers of safe, sanitary, and nutritious food, Health'R Us engages in a high level of quality control. Health 'R Us assigns its quality-control overhead costs to all products at a rate of 17% of direct labor costs. Its direct labor cost for the month of June for its...

Activity-Based And Department Rate Product Costing and Product Cost Distortions Black and Blue Sports Inc. manufactures two products: snowboards and skis. The factory overhead incurred is as follows: Indirect labor Cutting Department Finishing Department $507,000 156,000 192,000 Total $855,000 The activity base associated with the two production departments is direct labor hours. The indirect labor can be assigned to two different activities as follows: Activity Activity Base Budgeted Activity Cost $237,000 270,000 Production control Number of production runs Number of...

Activity-Based And Department Rate Product Costing and Product Cost Distortions Black and Blue Sports Inc. manufactures two products: snowboards and skis. The factory overhead incurred is as follows: Indirect labor Cutting Department Finishing Department $507,000 156,000 192,000 Total $855,000 The activity base associated with the two production departments is direct labor hours. The indirect labor can be assigned to two different activities as follows: Activity Activity Base Budgeted Activity Cost $237,000 270,000 Production control Number of production runs Number of...

Health 'R Us, Inc., uses a traditional product costing system to assign overhead costs uniformly to all its packaged multigrain products. To meet Food and Drug Administration requirements and to assure its customers of safe, sanitary, and nutritious food, Health 'R Us engages in a high level of quality control. Health R Us assigns its quality control overhead costs to all products at a rate of 17% of direct labor costs. Its direct labor cost for the month of June...

Health 'R Us, Inc., uses a traditional product costing system to assign overhead costs uniformly to all its packaged multigrain products. To meet Food and Drug Administration requirements and to assure its customers of safe, sanitary, and nutritious food, Health 'R Us engages in a high level of quality control. Health R Us assigns its quality control overhead costs to all products at a rate of 17% of direct labor costs. Its direct labor cost for the month of June...

Problem 17-1A Comparing costs using ABC with the plantwide overhead rate LO P1, P3, A1, A2 The following data are for the two products produced by Tadros Company Direct materials Direct labor hours Machine hours Batches Volu Engineering modifications Number of customers Market price Product A $15 per unit 0.4 DLH per unit 2.3 MH per unit 115 batches 10,000 units 10 modifications 500 customers $35 per unit Product B 528 per unit 1.6 DLH per unit 1.2 per unit...

Problem 17-1A Comparing costs using ABC with the plantwide overhead rate LO P1, P3, A1, A2 The following data are for the two products produced by Tadros Company Direct materials Direct labor hours Machine hours Batches Volu Engineering modifications Number of customers Market price Product A $15 per unit 0.4 DLH per unit 2.3 MH per unit 115 batches 10,000 units 10 modifications 500 customers $35 per unit Product B 528 per unit 1.6 DLH per unit 1.2 per unit...

Most questions answered within 3 hours.

-

Homologous Recombination Lecture

Molecular Biology

The ability for yeast and E. coli to do

homologous recombination...

asked 11 minutes ago -

A single pass heat exchanger is used to cool milk from 65 C to

20 C...

asked 11 minutes ago -

A water pistol aimed horizontally projects a stream of water

with an initial speed of 7.20...

asked 14 minutes ago -

Language: Python

Function name : findwaldo

Parameters : string

Returns: int

Description: Write a recursive function...

asked 33 minutes ago -

1) A loan of RM 10,000 at a flat rate of 10% per annum was

repaid...

asked 40 minutes ago -

Suppose you have been following a particular airline stock for

many years. You are interested in...

asked 46 minutes ago -

Describe the organic pasta: Is it a normal/inferior

good? Is it a necessity/luxury? Does it have...

asked 48 minutes ago -

Are Republicans just as likely as Democrats to display the

American flag in front of their...

asked 57 minutes ago -

Select the true statement below.

nitrogen dioxide is a stronger potential oxidizing agent than

dinitrogen monoxide...

asked 1 hour ago -

What’s the probability of getting a sequence of 1,2,3,4,5,6 if

we roll a dice six times?

asked 1 hour ago -

Ibarra Corporation uses the FIFO method in its process costing

system. The first processing department, the...

asked 1 hour ago -

Multiple Choice Question:

Jennifer Jones, a 38-year-old employee at a metal fabricating

plant, was injured in...

asked 1 hour ago