Homework Answers

Pb 34:

Intrinsic Value = D1 / [ Ke - g ]

D1 =Expected div after 1 Year

Ke = Required Ret

g = Growth Rate

Intrinsic Value = D1 / [ Ke - g ]

= 0.75 / [ 12.5% - 8.5% ]

= 0.75 / 4%

= $ 18.75

intrinsic Value is $ 18.75

OPtion D is correct

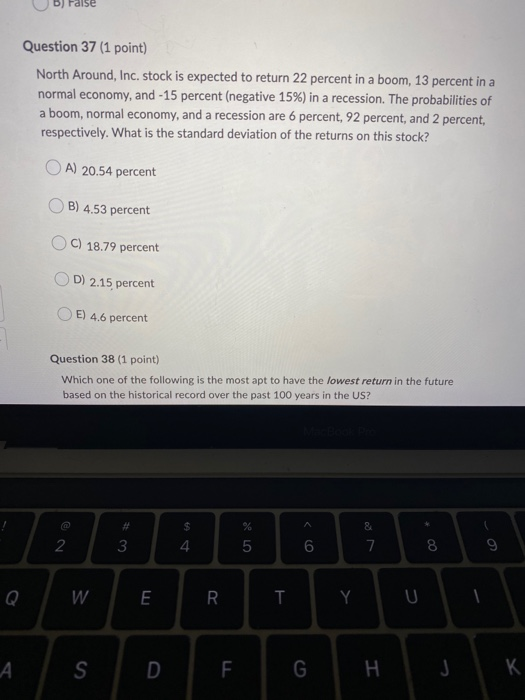

Pb 37:

SD:

It spcifies the risk of Stock.

SD = SQRT [ SUm [ Prob * (X-AVgX)^2 ] ]

Expected Ret:

| Scenario | Prob | Ret | Prob* Ret |

| Boom | 0.0600 | 22.00% | 1.32% |

| Normal | 0.9200 | 13.00% | 11.96% |

| Recision | 0.0200 | -15.00% | -0.30% |

| Expected Ret | 12.98% |

SD:

| State | Prob | Ret (X) | (X-AvgX) | (X-AvgX)^2 | Prob * (X-Avg X)^2 |

| Boom | 0.0600 | 22.00% | 9.02% | 0.008136 | 0.00049 |

| Normal | 0.9200 | 13.00% | 0.02% | 0.000000 | 0.00000 |

| Recision | 0.0200 | -15.00% | -27.98% | 0.078288 | 0.00157 |

| Sum[ Prob * ( X-AvgX)^2 ) ] | 0.00205 | ||||

| SD = SQRT [ [ Sum[ Prob * ( X-AvgX)^2 ) ] ] ] | 0.04532 | ||||

| I.e SD is 4.53 % |

OPtion B is correct

Pb 46:

Gain = Loss / Net Investment after Loss

= 35 / [ 100 - 35 ]

= 35 / 65

= 0.5385 i.e 53.85%

option C is correct.

Pls do rate, if the answer is correct and comment, if any further assistance is required.

Add Answer to:

pls answer the questions that are fully visible

Question 34 (1 point) A stock is expected...

Questions 3-5 are based on the following information. Westover stock is expected to return 36 percent...

Questions 3-5 are based on the following information. Westover stock is expected to return 36 percent in a boom, 14 percent in a normal economy, and lose 75 percent in a recession. The probabilities of a boom, normal economy, and a recession are 2 percent, 93 percent, and 5 percent, respectively 3. What is the expected return on this stock? A. 9.99 percent B. 8.99 percent C. 9.19 percent D. 10.1 percent 4. What is the variance on this stock?...

Questions 3-5 are based on the following information. Westover stock is expected to return 36 percent in a boom, 14 percent in a normal economy, and lose 75 percent in a recession. The probabilities of a boom, normal economy, and a recession are 2 percent, 93 percent, and 5 percent, respectively 3. What is the expected return on this stock? A. 9.99 percent B. 8.99 percent C. 9.19 percent D. 10.1 percent 4. What is the variance on this stock?...

1. What is the expected return on this stock given the following information? State of the...

1. What is the expected return on this stock given the following information? State of the Economy Probability E(R) Boom 0.4 14% Recession 0.6 -18% A) -8.07 percent B) -7.69 percent C) -6.80 percent D) -5.70 percent E) -5.20 percent

Please answer in detail. (calculator steps if possible) Question 5 (1 point) What is the expected return of a...

Please answer in detail. (calculator steps if possible)

Question 5 (1 point) What is the expected return of a portfolio that has 70% in Asset A and 30% in Asset B? Probability Asset A Asset B State of Rate of of State of Rate of Economy Economy Return Return Boom 0.3 0.13 0.08 Normal 0.5 0.05 0.06 Recession 0.2 -0.05 -0.01

Show transcribed image text Question 5 (1 point) What is the expected return of a portfolio that has 70%...

Please answer in detail. (calculator steps if possible)

Question 5 (1 point) What is the expected return of a portfolio that has 70% in Asset A and 30% in Asset B? Probability Asset A Asset B State of Rate of of State of Rate of Economy Economy Return Return Boom 0.3 0.13 0.08 Normal 0.5 0.05 0.06 Recession 0.2 -0.05 -0.01

Show transcribed image text Question 5 (1 point) What is the expected return of a portfolio that has 70%...

1. The stock of Blue Water Tours, Inc. is expected to return 21.50 percent in a...

1. The stock of Blue Water Tours, Inc. is expected to return 21.50 percent in a boom economy, 16.50 percent in a normal economy, and lose 15.50 percent in a recessionary economy. What is the expected rate of return on this stock if there is a 7.00 percent chance the economy booms, and an 83.00 percent chance the economy will be normal? 14.13 percent 13.65 percent 13.40 percent 12.48 percent 2. A stock is expected to earn 15 percent in...

1) ased on the following information, what is the expected return? State of Probability of State...

1) ased on the following information, what is the expected return? State of Probability of State Rate of Return if Economy of Economy State Occurs Recession .33 − 10.10% Normal .36 11.60% Boom .31 21.40% Multiple Choice a) 7.63% b) 10.81% c) 7.48% d) 7.56% e) 14.14% f) f6.85% 2) A stock has a beta of 1.17 and an expected return of 11.21 percent. If the risk-free rate is 3.2 percent, what is the stock's reward-to-risk ratio? Multiple Choice 5.99%...

Question 1: You are planning about putting some money in the stock market. There are two...

Question 1: You are planning about putting some money in the stock market. There are two stocks in your mind: stock A and stock B. The economy can either go in recession or it will boom in the coming years. Being an optimistic investor, you believe the likelihood of observing an economic boom is two times as high as observing an economic depression. You also know the following about your two stocks: State of the Economy Probability RA RB Boom...

TEST QUESTIONS: IMPORTANT: SHOW YOUR DETAILED SOLUTIONS FOR EACH QUESTION. 1) You are given the following...

TEST QUESTIONS: IMPORTANT: SHOW YOUR DETAILED SOLUTIONS FOR EACH QUESTION. 1) You are given the following information for a security State of Economy Boom Normal Recession Probability of State of Economy 0.04 0.74 0.22 Rate of Return if State Occurs 26% 2) A stock has an expected return of 10.2 percent, the risk-free rate is 3.9 percent, and the expected return on the market is 11.10 percent a. What must the beta of this stock be? (5 points) b. Is...

TEST QUESTIONS: IMPORTANT: SHOW YOUR DETAILED SOLUTIONS FOR EACH QUESTION. 1) You are given the following information for a security State of Economy Boom Normal Recession Probability of State of Economy 0.04 0.74 0.22 Rate of Return if State Occurs 26% 2) A stock has an expected return of 10.2 percent, the risk-free rate is 3.9 percent, and the expected return on the market is 11.10 percent a. What must the beta of this stock be? (5 points) b. Is...

Question 6 (1 point) A stock has a beta of 2.4, the market expected return is...

Question 6 (1 point) A stock has a beta of 2.4, the market expected return is 8% and the riskfree rate is 2%. What is the expected rate of return according to CAPM? Express your answer as a percentage, for example 3.18% should be entered as 3.18 without the percentage sign. Your Answer: Answer Question 7 (1 point) Suppose the covariance between the returns of the stock GHI and the returns to the market is 0.00064 and the standard deviation...

Question 6 (1 point) A stock has a beta of 2.4, the market expected return is 8% and the riskfree rate is 2%. What is the expected rate of return according to CAPM? Express your answer as a percentage, for example 3.18% should be entered as 3.18 without the percentage sign. Your Answer: Answer Question 7 (1 point) Suppose the covariance between the returns of the stock GHI and the returns to the market is 0.00064 and the standard deviation...

Question 9 - You have a portfolio that is comprised of 39 percent of stock A and the rest in stock B. What is the expec...

Question 9 -

You have a portfolio that is comprised of 39 percent of stock A and the rest in stock B. What is the expected return of the portfolio, given the information below? State of Economy. Probabillity of State Return of Stock A Return of Stock B Recession 0.21 -8.39 3.33 Normal 0.55 7.24 4.25 Boom 1 - (0.55+0.21) 16.89 9.22 Answer should be formatted as a percent with 2 decimal places (e.g. 99.99).

Question 9 -

You have a portfolio that is comprised of 39 percent of stock A and the rest in stock B. What is the expected return of the portfolio, given the information below? State of Economy. Probabillity of State Return of Stock A Return of Stock B Recession 0.21 -8.39 3.33 Normal 0.55 7.24 4.25 Boom 1 - (0.55+0.21) 16.89 9.22 Answer should be formatted as a percent with 2 decimal places (e.g. 99.99).

Question 19 (1 point) Calculate the expected return on a stock with a beta of 1.19....

Question 19 (1 point) Calculate the expected return on a stock with a beta of 1.19. The risk-free rate of return is 2% and the market portfolio has an expected return of 9%. (Enter your answer as a decimal rounded to 4 decimal places, not a percentage. For example, enter .0153 instead of 1.53%) Your Answer Answer

Question 19 (1 point) Calculate the expected return on a stock with a beta of 1.19. The risk-free rate of return is 2% and the market portfolio has an expected return of 9%. (Enter your answer as a decimal rounded to 4 decimal places, not a percentage. For example, enter .0153 instead of 1.53%) Your Answer Answer

Questions 3-5 are based on the following information. Westover stock is expected to return 36 percent in a boom, 14 percent in a normal economy, and lose 75 percent in a recession. The probabilities of a boom, normal economy, and a recession are 2 percent, 93 percent, and 5 percent, respectively 3. What is the expected return on this stock? A. 9.99 percent B. 8.99 percent C. 9.19 percent D. 10.1 percent 4. What is the variance on this stock?...

Questions 3-5 are based on the following information. Westover stock is expected to return 36 percent in a boom, 14 percent in a normal economy, and lose 75 percent in a recession. The probabilities of a boom, normal economy, and a recession are 2 percent, 93 percent, and 5 percent, respectively 3. What is the expected return on this stock? A. 9.99 percent B. 8.99 percent C. 9.19 percent D. 10.1 percent 4. What is the variance on this stock?...

Please answer in detail. (calculator steps if possible)

Question 5 (1 point) What is the expected return of a portfolio that has 70% in Asset A and 30% in Asset B? Probability Asset A Asset B State of Rate of of State of Rate of Economy Economy Return Return Boom 0.3 0.13 0.08 Normal 0.5 0.05 0.06 Recession 0.2 -0.05 -0.01

Show transcribed image text Question 5 (1 point) What is the expected return of a portfolio that has 70%...

Please answer in detail. (calculator steps if possible)

Question 5 (1 point) What is the expected return of a portfolio that has 70% in Asset A and 30% in Asset B? Probability Asset A Asset B State of Rate of of State of Rate of Economy Economy Return Return Boom 0.3 0.13 0.08 Normal 0.5 0.05 0.06 Recession 0.2 -0.05 -0.01

Show transcribed image text Question 5 (1 point) What is the expected return of a portfolio that has 70%...

TEST QUESTIONS: IMPORTANT: SHOW YOUR DETAILED SOLUTIONS FOR EACH QUESTION. 1) You are given the following information for a security State of Economy Boom Normal Recession Probability of State of Economy 0.04 0.74 0.22 Rate of Return if State Occurs 26% 2) A stock has an expected return of 10.2 percent, the risk-free rate is 3.9 percent, and the expected return on the market is 11.10 percent a. What must the beta of this stock be? (5 points) b. Is...

TEST QUESTIONS: IMPORTANT: SHOW YOUR DETAILED SOLUTIONS FOR EACH QUESTION. 1) You are given the following information for a security State of Economy Boom Normal Recession Probability of State of Economy 0.04 0.74 0.22 Rate of Return if State Occurs 26% 2) A stock has an expected return of 10.2 percent, the risk-free rate is 3.9 percent, and the expected return on the market is 11.10 percent a. What must the beta of this stock be? (5 points) b. Is...

Question 6 (1 point) A stock has a beta of 2.4, the market expected return is 8% and the riskfree rate is 2%. What is the expected rate of return according to CAPM? Express your answer as a percentage, for example 3.18% should be entered as 3.18 without the percentage sign. Your Answer: Answer Question 7 (1 point) Suppose the covariance between the returns of the stock GHI and the returns to the market is 0.00064 and the standard deviation...

Question 6 (1 point) A stock has a beta of 2.4, the market expected return is 8% and the riskfree rate is 2%. What is the expected rate of return according to CAPM? Express your answer as a percentage, for example 3.18% should be entered as 3.18 without the percentage sign. Your Answer: Answer Question 7 (1 point) Suppose the covariance between the returns of the stock GHI and the returns to the market is 0.00064 and the standard deviation...

Question 9 -

You have a portfolio that is comprised of 39 percent of stock A and the rest in stock B. What is the expected return of the portfolio, given the information below? State of Economy. Probabillity of State Return of Stock A Return of Stock B Recession 0.21 -8.39 3.33 Normal 0.55 7.24 4.25 Boom 1 - (0.55+0.21) 16.89 9.22 Answer should be formatted as a percent with 2 decimal places (e.g. 99.99).

Question 9 -

You have a portfolio that is comprised of 39 percent of stock A and the rest in stock B. What is the expected return of the portfolio, given the information below? State of Economy. Probabillity of State Return of Stock A Return of Stock B Recession 0.21 -8.39 3.33 Normal 0.55 7.24 4.25 Boom 1 - (0.55+0.21) 16.89 9.22 Answer should be formatted as a percent with 2 decimal places (e.g. 99.99).

Question 19 (1 point) Calculate the expected return on a stock with a beta of 1.19. The risk-free rate of return is 2% and the market portfolio has an expected return of 9%. (Enter your answer as a decimal rounded to 4 decimal places, not a percentage. For example, enter .0153 instead of 1.53%) Your Answer Answer

Question 19 (1 point) Calculate the expected return on a stock with a beta of 1.19. The risk-free rate of return is 2% and the market portfolio has an expected return of 9%. (Enter your answer as a decimal rounded to 4 decimal places, not a percentage. For example, enter .0153 instead of 1.53%) Your Answer Answer

Most questions answered within 3 hours.

-

Calculate the entropy change for the hypothetical process in

which 0.5 g of ice at 0°C...

asked 57 seconds from now -

Consider the economy of Freeland, whose overall actual price

index and actual output are P and...

asked 17 seconds ago -

Suppose that the production function takes the form Q=L-0.7L^2.

In addition, marginal revenue is $10 and...

asked 7 minutes ago -

If you were in charge of the selection and purchase of a display

system for the...

asked 7 minutes ago -

I just took a final for chemistry 2. There were alot of

questions on cell potential....

asked 11 minutes ago -

In which region of the country did Methodists and

Baptists have the largest following?

a. The...

asked 12 minutes ago -

A man is standing on a ledge when he throws a ball. The speed of

the...

asked 19 minutes ago -

Facebook Marketing benefit: How is this tool useful for

marketing purposes? Identify and explain at least...

asked 31 minutes ago -

What are the five considerations relevant to the

substantive fairness of a dismissal for permanent incapacity?...

asked 31 minutes ago -

Prince Electronics, a manufacturer of consumer electronic

goods, has five distribution centers in different regions of...

asked 33 minutes ago -

1.) For the following general reaction, rate = k[A]2 and k = 1.3

× 10−2 M−1...

asked 37 minutes ago -

In the Enron documentary(Netflix) What ethical issues did you

observe and who was responsible for them?

asked 37 minutes ago