Matt has just completed his MBA and landed a new job that will pay him $50,000...

Matt has just completed his MBA and landed a new job that will pay him $50,000 this year. He expects his salary to grow at the historical inflation rate 3.5% APR, plus 1% annually until he retires in 25 years. He is estimating that he will live for 30 years after retirement. Matt will use his forecasted salary on the day he retires as a target for the annual withdraws he will make at the beginning of each year during retirement. However, he wants to increase his retirement salary by the estimated inflation rate 3.5 % APR, each year during his retirement as well. (This is called a growing annuity). Matt currently has $25,000 in a bond mutual fund retirement account and will use that money for his retirement. He is also planning to start another retirement account and contribute $250 in a high-risk stock mutual fund each month until he retires. Matt expects his bond account to earn 4% APR Semi-Annual Bond Return and his stock account to earn 16% EAR, Stock Return until he retires. After his retirement, he will take a more conservative approach to managing his retirement funds and will place all his retirement funds in a mutual fund that will earn 7% APR Annual, Return after retirement.

PART 1: Calculate if Matt will have enough for retirement given the above information, showing all work and illustrating with a timeline. If he does not, estimate how much more he should put in his stock account each month to sustain his retirement. If he does, calculate by how much he can reduce his stock account contribution.

PART 2: Discuss your concerns about any risk that might be associated with his current strategy. Recommend and explain, illustrate with your own calculations and historical data, at least one alternative investment strategy that you might recommend prior to retirement.

Homework Answers

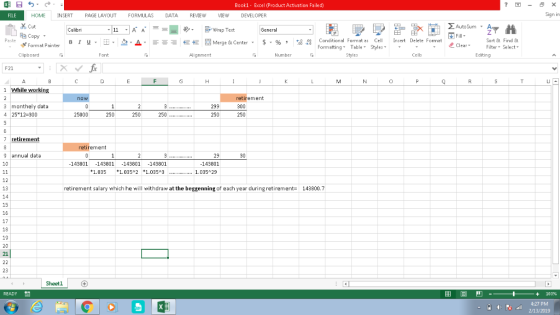

we have the following timelines

inflstion during working period =3.5+1=4.5%

inflation during retirement period =3.5%

target salary during retirement =50000(1.045)^24=143800.69

PV of this salary at the retirement@ 7%(as this salary would come from a fund which earns 7% annual)

PV of a growing annuity =C1*(1-((1+g)/(1+r))^n)/(r-g)

where

g=3.5%

r=7%

n=29(as the cashflows are at begenning)

C1=cashflow next year=C0*1.035=143800.69*1.035=153491.21

PV=153491.21*(1-(1.035/1.07)^29)/(.07-.035)+143800.69( cash flow at the beggenning of year 1 i.e. at time 0)

PV=2857572.63

now let us calulate the FV of investments at retirement (i.e. at time =25)

FV of bond investment=25000(1+.04/2)^(25*2)=67289.7

FV of equity investment= FV of first 24 inestments+ last investment=250*(1.16^24 -1)/(1.16^(1/12)-1) + 250=687996.84

total FV =687996.84+67289.7=755286.54

Shortage =2857572.63-755286.54=2102286.09

let the additional amount of stock investment be = x

hence FV of x @16% Should be =2102286.09

x*(1.16^24 -1)/(1.16^(1/12) -1)+x=2102286.09

x*2751.99=2102286.09

x=763.92

he needs to put 763.93 each month extra in stocks.

Part2:

since all the investments have been made in mutual funds , overall risk is minimised the only risk that remains is systematic risk which impact every one simultaneously and he can't do anything with this however bond portfolio doesn't have even that kind of risk that is it offers a lower interest rate now as we can see stock fund provides better returns then he should transfer this dollar from bond fund to stock fund it will have the following implications

EXtra FV = 25000*1.16^25 - 25000*1.02^50

= 1021856.09-67289.7=954566.39

because of this extra money contribution in stock would only b( 2102286.09-954566.39)/2751.99 =417.05

Add Answer to:

Matt has just completed his MBA and landed a new job that will

pay him $50,000...

Takashi plans to save $30,000 per year until he retires. his first savings contribution to his...

Takashi plans to save $30,000 per year until he retires. his first savings contribution to his retirement account is expected in 1 year from today. Takashi plans to retire in 6 years from today, immediately after making his last $30,000 contribution to his retirement account. he then plans to be retired for 6 years. Takashi expects to earn 8.0% per year in his retirement account. both before and during his retirement. If takashi receives equal annual payments from his retirement...

Wealth Management

Anupam is currently 38 years old and plans to retire when he is 65. He earns Rs25,00,000 a year as a wedding planner and gets a 5% increase every year . He currently has Rs 3,80,000 saved for his retirement in an equity fund that earns 20%. Anupam will leave the money in this mutual fund until he retires, the time when he will place all his savings into a money market mutual fund that earns 6%. He contributes 10%...

Assume that your father is now 50 years old, plans to retire in 10 years, and...

Assume that your father is now 50 years old, plans to retire in 10 years, and expects to live for 25 years after he retires - that is, until age 85. He wants his first retirement payment to have the same purchasing power at the time he retires as $50,000 has today. He wants all of his subsequent retirement payments to be equal to his first retirement payment. (Do not let the retirement payments grow with inflation: Your father realizes...

QUESTION 10 Takashi plans to save $25,000 per year until he retires. His first savings contribution...

QUESTION 10 Takashi plans to save $25,000 per year until he retires. His first savings contribution to his retirement account is expected in 1 year from today. Takashi plans to retire in 6 years from today, immediately after making his last $25,000 contribution to his retirenlent account. He then plans to be retired for 6 years. Takashi expects to earn 7.0 percent per year in his retirement account, both before and during his retirement. If Takashi receives equal annual payments...

QUESTION 10 Takashi plans to save $25,000 per year until he retires. His first savings contribution to his retirement account is expected in 1 year from today. Takashi plans to retire in 6 years from today, immediately after making his last $25,000 contribution to his retirenlent account. He then plans to be retired for 6 years. Takashi expects to earn 7.0 percent per year in his retirement account, both before and during his retirement. If Takashi receives equal annual payments...

Assume that your father is now 50 years old, plans to retire in 10 years, and...

Assume that your father is now 50 years old, plans to retire in 10 years, and expects to live for 25 years after he retires - that is, until age 85. He wants his first retirement payment to have the same purchasing power at the time he retires as $40,000 has today. He wants all of his subsequent retirement payments to be equal to his first retirement payment. (Do not let the retirement payments grow with inflation: Your father realizes...

Hermes Conrad is celebrating his birthday and wants to start saving for his anticipated retirement. He...

Hermes Conrad is celebrating his birthday and wants to start saving for his anticipated retirement. He has the following years to retirement and retirement spending goals: Years until retirement = 30; Amount to withdraw each year = $90,000; Years to withdraw in retirement = 20; Investment rate = 8%. Because Hermes is planning ahead, the first withdrawal will not take place until one year after he retires. He wants to make equal annual deposits into his account for his retirement...

The Certainty Company (CC) operates in a world of certainty. It has just hired Matt (age...

The Certainty Company (CC) operates in a world of certainty. It has just hired Matt (age 20) who will retire at age 65, draw retirement benefits for 15 years, and die at age 80. Matt's salary is $20,000 per year, but wages are expected to increase at the 5% annual rate of inflation. CC has a defined benefit plan in which workers receive 1% of the final year's wage for each year employed. The retirement benefit, once started, does not...

The Certainty Company (CC) operates in a world of certainty. It has just hired Matt (age 20) who will retire at age 65, draw retirement benefits for 15 years, and die at age 80. Matt's salary is $20,000 per year, but wages are expected to increase at the 5% annual rate of inflation. CC has a defined benefit plan in which workers receive 1% of the final year's wage for each year employed. The retirement benefit, once started, does not...

20. Assume that your father is now so years old, that he plans to retire in...

20. Assume that your father is now so years old, that he plans to retire in 10 years, and that he expects to live for 25 years after he retires (that is, until he is 85). If he retired today, he could live comfortably on $50,000 per year. However, because of inflation, his target retirement income must increase by 5% per year until his retirement date (.e. inflation is 5% annually). In other words, he must receive more than $50,000...

20. Assume that your father is now so years old, that he plans to retire in 10 years, and that he expects to live for 25 years after he retires (that is, until he is 85). If he retired today, he could live comfortably on $50,000 per year. However, because of inflation, his target retirement income must increase by 5% per year until his retirement date (.e. inflation is 5% annually). In other words, he must receive more than $50,000...

Your father is 50 years old and will retire in 10 years. He expects to live...

Your father is 50 years old and will retire in 10 years. He expects to live for 25 years after he retires, until he is 85. He wants a fixed retirement income that has the same purchasing power at the time he retires as $40,000 has today. (The real value of his retirement income will decline annually after he retires.) His retirement income will begin the day he retires, 10 years from today, at which time he will receive 24...

4. (Zero Coupon Bonds) A zero coupon bond is a debt security that does not pay...

4. (Zero Coupon Bonds) A zero coupon bond is a debt security that does not pay interest but trades at a discount, and will pay its face value at maturity. Suppose a zero coupon bond matures to a value of $1000 in eight years. If the bond is yielding at 4% per annum, what is the purchase price of the bond? Suppose a 8-year coupon-paying bond is paying $40 a year, and has a face value of $1000 is selling...

QUESTION 10 Takashi plans to save $25,000 per year until he retires. His first savings contribution to his retirement account is expected in 1 year from today. Takashi plans to retire in 6 years from today, immediately after making his last $25,000 contribution to his retirenlent account. He then plans to be retired for 6 years. Takashi expects to earn 7.0 percent per year in his retirement account, both before and during his retirement. If Takashi receives equal annual payments...

QUESTION 10 Takashi plans to save $25,000 per year until he retires. His first savings contribution to his retirement account is expected in 1 year from today. Takashi plans to retire in 6 years from today, immediately after making his last $25,000 contribution to his retirenlent account. He then plans to be retired for 6 years. Takashi expects to earn 7.0 percent per year in his retirement account, both before and during his retirement. If Takashi receives equal annual payments...

The Certainty Company (CC) operates in a world of certainty. It has just hired Matt (age 20) who will retire at age 65, draw retirement benefits for 15 years, and die at age 80. Matt's salary is $20,000 per year, but wages are expected to increase at the 5% annual rate of inflation. CC has a defined benefit plan in which workers receive 1% of the final year's wage for each year employed. The retirement benefit, once started, does not...

The Certainty Company (CC) operates in a world of certainty. It has just hired Matt (age 20) who will retire at age 65, draw retirement benefits for 15 years, and die at age 80. Matt's salary is $20,000 per year, but wages are expected to increase at the 5% annual rate of inflation. CC has a defined benefit plan in which workers receive 1% of the final year's wage for each year employed. The retirement benefit, once started, does not...

20. Assume that your father is now so years old, that he plans to retire in 10 years, and that he expects to live for 25 years after he retires (that is, until he is 85). If he retired today, he could live comfortably on $50,000 per year. However, because of inflation, his target retirement income must increase by 5% per year until his retirement date (.e. inflation is 5% annually). In other words, he must receive more than $50,000...

20. Assume that your father is now so years old, that he plans to retire in 10 years, and that he expects to live for 25 years after he retires (that is, until he is 85). If he retired today, he could live comfortably on $50,000 per year. However, because of inflation, his target retirement income must increase by 5% per year until his retirement date (.e. inflation is 5% annually). In other words, he must receive more than $50,000...

Most questions answered within 3 hours.

-

you want to measure the gravitational acceleration at your

location. since g does not vary significantly...

asked 42 seconds ago -

Aside from commercial tools that are specifically geared toward

TAR/PC( Technology-Assisted Review), are there potential

alternative...

asked 2 minutes ago -

the period of a pendulum on earth is 5 seconds. what will be the

period of...

asked 18 minutes ago -

The

act of turning media against itself, such as flash mobs and

billboard is called

a....

asked 14 minutes ago -

A set of length measurements are obtained with the values 165.6

± 0.3, 165.1± 0.4,166.4± 1.0,...

asked 15 minutes ago -

Vertical Analysis

Income statement information for Einsworth Corporation

follows:

Sales

$237,000

Cost of goods sold

78,210...

asked 22 minutes ago -

A simple random sample was taken to test the claim that the

population mean is no...

asked 17 minutes ago -

Overview

JAVA LANGUAGE PROBLEM:

The owner of a restaurant wants a program to manage online

orders...

asked 22 minutes ago -

1- What is “progressive production?”

2- Where did the assembly line originate? (Name the industry)

3....

asked 20 minutes ago -

NPV

Project L costs $60,000 it’s expected cash inflows are $13,000

per year for 10 years,...

asked 25 minutes ago -

What would you expect the observed boiling point to be at 10

torrs of a liquid...

asked 33 minutes ago -

write a javascript jquery code to display calendar and let it be

sticked on the textbox...

asked 40 minutes ago