Need help on this

question!

Need help on this

question!Homework Answers

(1) Unit level cost, Batch Level cost,product-service sustaining cost,facility sustaining cost

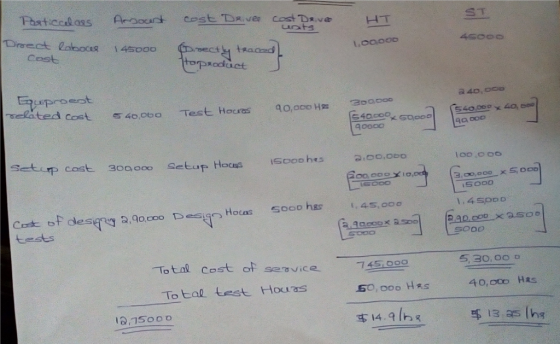

Direct Labor cost;145000: Product-service sustaining cost

This is product-service sustaining cost since its support individual services regardless of the number units or batches in which the units are produced. Here direct labor cost can be traced to individual service, not to each unit or batch of services. Hence its a product-service sustaining cost

Equipment Related cost;54000: Facility sustaining cost

This is a Facility sustaining cost since it cant be traced to individual produtcs but support the organistaions as a whole.

Set up cost; 300000: Batch level cost

Usually set up is required before production of a batch. hence its classified as batch level cost.

However if its can't be traced to batches, then it can be classified as product-service sustaining cost.

Cost of designing test; 29000: batch level cost

Its a batch level cost since the cost can be traced to each batch of similar test designed.

It cant be traced to each unit of test hour.

(2)

| Particulars | HT | ST | |

| Under new costing system | 14.9/hour | 13.25/hour | |

| Under simple costing system | 14/hour | 14/hour | |

| Difference | 0.9 increase | 0.75 decrease |

Under simple costing system, All cost are pooled together and allocated based on test hours. However under new costing system, costs are pooled to each product head on the basis on activities related to each service.This is the main reason for the difference in the rate. The new costing system gives a more accurate picture of the cost of each service.

In addition to that, in simple costing system, only $1260000 is recognised. In new costing system, $1275000 is recognised. An additional $ 15000 is recognised in new costing system. This amount might be allocated as a general overhead in the old system. This also cause a reason for the difference.

(3) In simple costing system, cost is pooled to product or services. while ABC costing system assigns cost to activities. In ABC, it tracks the flow of activities by creating internal link between activity and cost object. This helps in more accurate cost allocation.

Hence ABC is more preferable in costing if more than one service or product is provided.

In case of management, ABC is better in managing the business and cost hierarchy since the simple costing system is not rich enough to supply the information needed for thorough analysis of linkages.

ABC are mostly essential part of strategic analysis. Activities not based on production units/ sales units, based on variable activity drivers are analysed.

Add Answer to:

Need help on this

question!

Hull Test Laboratories does heat testing (HT) and stress testing (ST)...

Milton Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at...

Milton Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Milton aggregates all operating costs of $1,360,000 into a single overhead cost pool. Milton calculates a rate per test-hour of $16 ($1,360,000 / 85,000 total test-hours). HT uses 55,000 test-hours, and ST uses 30,000 test-hours. Gary Daley, Milton's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing and billing...

Milton Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Milton aggregates all operating costs of $1,360,000 into a single overhead cost pool. Milton calculates a rate per test-hour of $16 ($1,360,000 / 85,000 total test-hours). HT uses 55,000 test-hours, and ST uses 30,000 test-hours. Gary Daley, Milton's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing and billing...

Ayer Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at...

Ayer Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Ayer aggregates all operating costs of $1,360,000 i 55,000 test-hours, and ST uses 30,000 test-hours. Gary Celeste, Ayer's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing and billing mispricing of its services could cause Ayer to lose business. Celeste divides Ayer's costs into four activity-cost categories. (Click the...

Ayer Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Ayer aggregates all operating costs of $1,360,000 i 55,000 test-hours, and ST uses 30,000 test-hours. Gary Celeste, Ayer's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing and billing mispricing of its services could cause Ayer to lose business. Celeste divides Ayer's costs into four activity-cost categories. (Click the...

%E5-19 (similar Vineyard Test Laboratories does heat testing (HT) and stress testing (ST) on materials and...

%E5-19 (similar Vineyard Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Vineyard aggregates all operating costs of $1,330,000 into a single overhead cost pool. Vineyard calculates a rate per test-hour of $14 (51,330,000/ 95,000 total test hours). HT uses 63.000 test-hours, and ST uses 32,000 test-hours. Gary Celeste, Vineyard's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing...

%E5-19 (similar Vineyard Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Vineyard aggregates all operating costs of $1,330,000 into a single overhead cost pool. Vineyard calculates a rate per test-hour of $14 (51,330,000/ 95,000 total test hours). HT uses 63.000 test-hours, and ST uses 32,000 test-hours. Gary Celeste, Vineyard's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing...

Milton Test Laboratories does heat testing(HT) and stress testing (ST) on materials and operates at capacity....

Milton Test Laboratories does heat testing(HT) and stress

testing (ST) on materials and operates at capacity. Under its

current simple costingsystem, Milton aggregates all operating

costs of $1,330,000 into a single overhead cost pool. Milton

calculates a rate pertest-hour of $14 ($1,330,000 / 95,000 total

test-hours). HT uses 63,000 test-hours, and ST uses 32,000

test-hours. Gary Savarese, Milton’s controller, believes that there

is enough variation in test procedures and cost structures to

establish separate costing and billing rates for HT...

Milton Test Laboratories does heat testing(HT) and stress

testing (ST) on materials and operates at capacity. Under its

current simple costingsystem, Milton aggregates all operating

costs of $1,330,000 into a single overhead cost pool. Milton

calculates a rate pertest-hour of $14 ($1,330,000 / 95,000 total

test-hours). HT uses 63,000 test-hours, and ST uses 32,000

test-hours. Gary Savarese, Milton’s controller, believes that there

is enough variation in test procedures and cost structures to

establish separate costing and billing rates for HT...

Hopkinton Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at...

Hopkinton Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Hopkinton aggregates all operating costs of $1,200,000 into a single overhead cost pool. Hopkinton calculates a rate per test-hour of $16 ($1,200,000 / 75,000 total test-hours). HT uses 50,000 test-hours, and ST uses 25,000 test-hours. Gary Mahoney, Hopkinton's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing and billing...

Hopkinton Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Hopkinton aggregates all operating costs of $1,200,000 into a single overhead cost pool. Hopkinton calculates a rate per test-hour of $16 ($1,200,000 / 75,000 total test-hours). HT uses 50,000 test-hours, and ST uses 25,000 test-hours. Gary Mahoney, Hopkinton's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing and billing...

Vineyard Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at...

Vineyard Test Laboratories does heat testing (HT) and stress

testing (ST) on materials and operates at capacity. Under its

current simple costing system, Vineyard aggregates all operating

costs of $ 1 comma 190 comma 000 into a single overhead cost pool.

Vineyard calculates a rate per test-hour of $ 17 ($ 1 comma 190

comma 000 / 70 comma 000 total test-hours). HT uses 40 comma 000

test-hours, and ST uses 30 comma 000 test-hours. Gary Maloney,

Vineyard's controller, believes...

Vineyard Test Laboratories does heat testing (HT) and stress

testing (ST) on materials and operates at capacity. Under its

current simple costing system, Vineyard aggregates all operating

costs of $ 1 comma 190 comma 000 into a single overhead cost pool.

Vineyard calculates a rate per test-hour of $ 17 ($ 1 comma 190

comma 000 / 70 comma 000 total test-hours). HT uses 40 comma 000

test-hours, and ST uses 30 comma 000 test-hours. Gary Maloney,

Vineyard's controller, believes...

Hopkinton Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at...

Hopkinton Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Hopkinton aggregates all operating costs of $1,200,000 into a single overhead cost pool. Hopkinton calculates a rate per test-hour of $16 ($1,200,000/75,000 total test-hours). HT uses 50,000 test-hours, and ST uses 25,000 test-hours. Gary O'Loughlin, Hopkinton's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing and billing rates for...

Hopkinton Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Hopkinton aggregates all operating costs of $1,200,000 into a single overhead cost pool. Hopkinton calculates a rate per test-hour of $16 ($1,200,000/75,000 total test-hours). HT uses 50,000 test-hours, and ST uses 25,000 test-hours. Gary O'Loughlin, Hopkinton's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing and billing rates for...

Hopkinton Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at...

Hopkinton Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Hopkinton aggregates all operating costs of $1,300,000 into a single overhead cost pool. Hopkinton calculates a rate per test-hour of S13 ($1,300,000 / 100,000 total test-hours). HT uses 60,000 test-hours, and ST uses 40,000 test-hours. Gary Celeste, Hopkinton's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing and billing...

Hopkinton Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Hopkinton aggregates all operating costs of $1,300,000 into a single overhead cost pool. Hopkinton calculates a rate per test-hour of S13 ($1,300,000 / 100,000 total test-hours). HT uses 60,000 test-hours, and ST uses 40,000 test-hours. Gary Celeste, Hopkinton's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing and billing...

Hopkinton Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at...

Hopkinton Test Laboratories does heat testing (HT) and

stress testing (ST) on materials and operates at capacity. Under

its current simple frosting system. Hopkinton aggregates all

operating costs of $1,300,000 into a single overhead cost pool.

Hopkinton calculates a rate per two-hour of $13 (1,300,000/100,000

total test hours). HT uses 60,000 test hours, and ST uses 40,000

test hours. Gary O'Laughlin, Hopkinton's controller, believes that

there is enough variation in test procedures and cost structures to

establish separate costing and...

Hopkinton Test Laboratories does heat testing (HT) and

stress testing (ST) on materials and operates at capacity. Under

its current simple frosting system. Hopkinton aggregates all

operating costs of $1,300,000 into a single overhead cost pool.

Hopkinton calculates a rate per two-hour of $13 (1,300,000/100,000

total test hours). HT uses 60,000 test hours, and ST uses 40,000

test hours. Gary O'Laughlin, Hopkinton's controller, believes that

there is enough variation in test procedures and cost structures to

establish separate costing and...

Holliston Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at...

Holliston Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Holliston aggregates all operating costs of $1,275,000 into a single overhead cost pool. Holliston calculates a rate per test-hour of $15 ($1,275,000 / 85,000 total test-hours). HT uses 60,000 test-hours, and ST uses 25,000 test-hours. Gary Sarsfield, Holliston's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing and billing...

Holliston Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Holliston aggregates all operating costs of $1,275,000 into a single overhead cost pool. Holliston calculates a rate per test-hour of $15 ($1,275,000 / 85,000 total test-hours). HT uses 60,000 test-hours, and ST uses 25,000 test-hours. Gary Sarsfield, Holliston's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing and billing...

Milton Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Milton aggregates all operating costs of $1,360,000 into a single overhead cost pool. Milton calculates a rate per test-hour of $16 ($1,360,000 / 85,000 total test-hours). HT uses 55,000 test-hours, and ST uses 30,000 test-hours. Gary Daley, Milton's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing and billing...

Milton Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Milton aggregates all operating costs of $1,360,000 into a single overhead cost pool. Milton calculates a rate per test-hour of $16 ($1,360,000 / 85,000 total test-hours). HT uses 55,000 test-hours, and ST uses 30,000 test-hours. Gary Daley, Milton's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing and billing...

Ayer Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Ayer aggregates all operating costs of $1,360,000 i 55,000 test-hours, and ST uses 30,000 test-hours. Gary Celeste, Ayer's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing and billing mispricing of its services could cause Ayer to lose business. Celeste divides Ayer's costs into four activity-cost categories. (Click the...

Ayer Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Ayer aggregates all operating costs of $1,360,000 i 55,000 test-hours, and ST uses 30,000 test-hours. Gary Celeste, Ayer's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing and billing mispricing of its services could cause Ayer to lose business. Celeste divides Ayer's costs into four activity-cost categories. (Click the...

%E5-19 (similar Vineyard Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Vineyard aggregates all operating costs of $1,330,000 into a single overhead cost pool. Vineyard calculates a rate per test-hour of $14 (51,330,000/ 95,000 total test hours). HT uses 63.000 test-hours, and ST uses 32,000 test-hours. Gary Celeste, Vineyard's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing...

%E5-19 (similar Vineyard Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Vineyard aggregates all operating costs of $1,330,000 into a single overhead cost pool. Vineyard calculates a rate per test-hour of $14 (51,330,000/ 95,000 total test hours). HT uses 63.000 test-hours, and ST uses 32,000 test-hours. Gary Celeste, Vineyard's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing...

Milton Test Laboratories does heat testing(HT) and stress

testing (ST) on materials and operates at capacity. Under its

current simple costingsystem, Milton aggregates all operating

costs of $1,330,000 into a single overhead cost pool. Milton

calculates a rate pertest-hour of $14 ($1,330,000 / 95,000 total

test-hours). HT uses 63,000 test-hours, and ST uses 32,000

test-hours. Gary Savarese, Milton’s controller, believes that there

is enough variation in test procedures and cost structures to

establish separate costing and billing rates for HT...

Milton Test Laboratories does heat testing(HT) and stress

testing (ST) on materials and operates at capacity. Under its

current simple costingsystem, Milton aggregates all operating

costs of $1,330,000 into a single overhead cost pool. Milton

calculates a rate pertest-hour of $14 ($1,330,000 / 95,000 total

test-hours). HT uses 63,000 test-hours, and ST uses 32,000

test-hours. Gary Savarese, Milton’s controller, believes that there

is enough variation in test procedures and cost structures to

establish separate costing and billing rates for HT...

Hopkinton Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Hopkinton aggregates all operating costs of $1,200,000 into a single overhead cost pool. Hopkinton calculates a rate per test-hour of $16 ($1,200,000 / 75,000 total test-hours). HT uses 50,000 test-hours, and ST uses 25,000 test-hours. Gary Mahoney, Hopkinton's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing and billing...

Hopkinton Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Hopkinton aggregates all operating costs of $1,200,000 into a single overhead cost pool. Hopkinton calculates a rate per test-hour of $16 ($1,200,000 / 75,000 total test-hours). HT uses 50,000 test-hours, and ST uses 25,000 test-hours. Gary Mahoney, Hopkinton's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing and billing...

Vineyard Test Laboratories does heat testing (HT) and stress

testing (ST) on materials and operates at capacity. Under its

current simple costing system, Vineyard aggregates all operating

costs of $ 1 comma 190 comma 000 into a single overhead cost pool.

Vineyard calculates a rate per test-hour of $ 17 ($ 1 comma 190

comma 000 / 70 comma 000 total test-hours). HT uses 40 comma 000

test-hours, and ST uses 30 comma 000 test-hours. Gary Maloney,

Vineyard's controller, believes...

Vineyard Test Laboratories does heat testing (HT) and stress

testing (ST) on materials and operates at capacity. Under its

current simple costing system, Vineyard aggregates all operating

costs of $ 1 comma 190 comma 000 into a single overhead cost pool.

Vineyard calculates a rate per test-hour of $ 17 ($ 1 comma 190

comma 000 / 70 comma 000 total test-hours). HT uses 40 comma 000

test-hours, and ST uses 30 comma 000 test-hours. Gary Maloney,

Vineyard's controller, believes...

Hopkinton Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Hopkinton aggregates all operating costs of $1,200,000 into a single overhead cost pool. Hopkinton calculates a rate per test-hour of $16 ($1,200,000/75,000 total test-hours). HT uses 50,000 test-hours, and ST uses 25,000 test-hours. Gary O'Loughlin, Hopkinton's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing and billing rates for...

Hopkinton Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Hopkinton aggregates all operating costs of $1,200,000 into a single overhead cost pool. Hopkinton calculates a rate per test-hour of $16 ($1,200,000/75,000 total test-hours). HT uses 50,000 test-hours, and ST uses 25,000 test-hours. Gary O'Loughlin, Hopkinton's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing and billing rates for...

Hopkinton Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Hopkinton aggregates all operating costs of $1,300,000 into a single overhead cost pool. Hopkinton calculates a rate per test-hour of S13 ($1,300,000 / 100,000 total test-hours). HT uses 60,000 test-hours, and ST uses 40,000 test-hours. Gary Celeste, Hopkinton's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing and billing...

Hopkinton Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Hopkinton aggregates all operating costs of $1,300,000 into a single overhead cost pool. Hopkinton calculates a rate per test-hour of S13 ($1,300,000 / 100,000 total test-hours). HT uses 60,000 test-hours, and ST uses 40,000 test-hours. Gary Celeste, Hopkinton's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing and billing...

Hopkinton Test Laboratories does heat testing (HT) and

stress testing (ST) on materials and operates at capacity. Under

its current simple frosting system. Hopkinton aggregates all

operating costs of $1,300,000 into a single overhead cost pool.

Hopkinton calculates a rate per two-hour of $13 (1,300,000/100,000

total test hours). HT uses 60,000 test hours, and ST uses 40,000

test hours. Gary O'Laughlin, Hopkinton's controller, believes that

there is enough variation in test procedures and cost structures to

establish separate costing and...

Hopkinton Test Laboratories does heat testing (HT) and

stress testing (ST) on materials and operates at capacity. Under

its current simple frosting system. Hopkinton aggregates all

operating costs of $1,300,000 into a single overhead cost pool.

Hopkinton calculates a rate per two-hour of $13 (1,300,000/100,000

total test hours). HT uses 60,000 test hours, and ST uses 40,000

test hours. Gary O'Laughlin, Hopkinton's controller, believes that

there is enough variation in test procedures and cost structures to

establish separate costing and...

Holliston Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Holliston aggregates all operating costs of $1,275,000 into a single overhead cost pool. Holliston calculates a rate per test-hour of $15 ($1,275,000 / 85,000 total test-hours). HT uses 60,000 test-hours, and ST uses 25,000 test-hours. Gary Sarsfield, Holliston's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing and billing...

Holliston Test Laboratories does heat testing (HT) and stress testing (ST) on materials and operates at capacity. Under its current simple costing system, Holliston aggregates all operating costs of $1,275,000 into a single overhead cost pool. Holliston calculates a rate per test-hour of $15 ($1,275,000 / 85,000 total test-hours). HT uses 60,000 test-hours, and ST uses 25,000 test-hours. Gary Sarsfield, Holliston's controller, believes that there is enough variation in test procedures and cost structures to establish separate costing and billing...

Most questions answered within 3 hours.

-

1. Which region has taken the lead in the world of

e-waste handling?

a) European Union...

asked 46 seconds from now -

If you’re standing at the bottom of a hill and asked to evaluate

it while being...

asked 5 minutes ago -

A 8.15- g bullet from a 9-mm pistol has a velocity of 366.0 m/s.

It strikes...

asked 1 hour ago -

The outstanding bonds of Alpha Extracts have a yield to maturity

of 7.4 percent and a...

asked 1 hour ago -

The Problem: The Case of the Harmonizing Vacations

Your CEO is exploring partnering with a European...

asked 2 hours ago -

A chemical equation is balanced by adding coefficients in front

of some formulas so that the...

asked 2 hours ago -

From the literature (reference your sources): What are the

lattice parameters of calcite and aragonite? Why...

asked 3 hours ago -

Your system is rejecting the question am asking which is

preceded by a case study. It...

asked 3 hours ago -

3. On January 2, 2000, Larry creates a trust with himself as

trustee. Larry as trustee...

asked 3 hours ago -

A member of the volleyball team spikes the ball. During this

process, she changes the velocity...

asked 3 hours ago -

Are adult gamers less likely to use a gaming console (Xbox,

PlayStation, Wii, etc...) than teen...

asked 4 hours ago -

The University of

Texas recently reported that 43% of college students aged 18-24

would spend their...

asked 4 hours ago