Cost Accounting

Assignment 1

Fellco Manufacturing

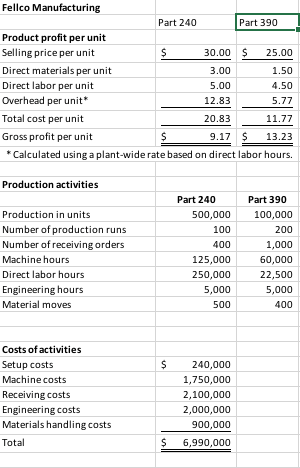

Fellco Manufacturing produces replacement parts for motorcycles. They specialize in the production of Part 240 and Part 390. Part 240 is the highest volume of the two and for many years was the only part the company produced. Four years ago, Part 390 was added. Part 390 is much more difficult to manufacture and requires special tooling and setups. Profits were on the rise for the first two years after the addition of Part 390. In the last two years the plant was under intense competition, and its sales of Part 240 dropped. The plant actually showed a small loss in the most recent reporting period. Most of the competition was from overseas, and the plant manager was sure that the foreign producers were selling the part below their own production costs. The following conversation between Kathryn Gonzales, plant manager, and Jon Jones, divisional marketing manager, reflects the concerns of the division about the future of the plant and its products.

JON: You know, Kathryn, the divisional manager is really concerned about the plant’s trend. He indicated that in this budgetary environment, we can’t afford to carry plants that don’t show a profit. We shut one down just last month because it couldn’t handle the competition.

KATHRYN: Joe, you and I both know that Part 240 has a reputation for quality and value. It has been a mainstay for years. I don’t understand what is happening.

JON: I just received a call from one of our major customers concerning Part 240. She said that a sales representative from another company offered the part at $20, $10 less than what we charge. It’s hard to compete with a price like that. Perhaps the plant is simply obsolete.

KATHRYN: No. I don’t buy that. From my sources, I know we have good technology. We are efficient. And it’s costing us around $21 to produce that part. I don’t see how these companies can afford to sell it so cheaply. I’m not convinced that we should meet the price. Perhaps a better strategy is to emphasize producing and selling more of Part 390. Our margin is high on this product, and we have virtually no competition for it.

JON: You may be right. I think we can increase the price significantly and not lose business. I called a few customers to see how they would react to a 25% increase in price, and they all said they would probably purchase the same quantity as before.

KATHRYN: It sounds promising. However, before we make a major commitment to Part 390, I think we had better explore other possible explanations. I want to know how our production costs compare to those of our competitors. Perhaps we could be more efficient and find a way to earn our normal return on Part 240. The market is so much bigger for this part. I’m not sure we can survive with only Part 390. Besides, my production people hate that part. It’s very difficult to produce.

After her meeting with Jon, Kathryn requested an investigation of the production costs and comparative efficiency. She received approval to hire a consulting group to make an independent investigation. After a 3-month assessment, the consulting group provided the costs and other information regarding the company’s two products. That information is found on the spreadsheet called “Fellco Manufacturing.”

Required:

NOTE: You should have two items to place in the dropbox:

- (8 points) Based on the information given about the company and

the information found in the spreadsheet, prepare an Excel

spreadsheet that includes:

- The activity based costing rates for each activity

- The total and per unit product cost for each product – include each cost item separately.

- The gross profit for each product using activity based costing, in total and per unit.

The numeric solution should be completed on the spreadsheet provided. I will be reviewing the spreadsheet for:

- Proper formatting. Assume that this is a report you will be providing to Kathryn, who is your direct supervisor. Information should be easy to read and fairly self-explanatory. Properly including dollar signs, commas, decimals where appropriate, and so on is necessary.

- Proper use of spreadsheet functions – copying, addition, subtraction – where appropriate. All fields should be set up so a change to the Data Sheet will flow through to all calculations. When I click on “Show Formulas” every cell should be a formula with no hard coded numbers. Set up your formulas to always reference back to numbers on the Data Sheet, a previous calculation or to previous spreadsheet pages. Add to your Data Sheet if necessary so this is possible. (loss of 3 pts)

- Correct answers (of course)

- (12 Points) Given what you have discovered, provide a memo to

Kathryn Gonzales that provides:

- An explanation as to how activity based costing is different from the current product cost method (2 points)

- A discussion of whether the company should switch its emphasis from Part 240 to Part 390 (2 points)

- A possible explanation as to why competitors are selling Part 240 below Fellco’s current cost of $21 and the willingness of customers to accept a 25% increase in the selling price of Part 390. Assume that the competitors are currently selling Part 240 for $20 and Part 390 for $45. (2 pts)

- A discussion of actions that Kathryn and Jon should take with

these products regarding:

- pricing,

- cost reductions in the cost per unit of activity

- process improvements in the usage of activity per product.

- Be specific. (6 points)

- The memo to Kathryn should be prepared in a Word document. Please use proper formatting, spelling, and grammar. I will be looking for your CLEAR, CONCISE, explanations.

- Remind why you are writing and summarize your recommendations in the opening paragraph, go on to explain your recommendations through your response to the points laid out above. Finally, restate your conclusions.

- Don’t just look at the obvious. Remember, you are in a competitive environment. Assume this memo is for your direct supervisor. You feel you have a future at this company, and you should want to do a good job.

Homework Answers

1. Computation of Cost per unit and Gross profut as per Activity Based Costing

| Cost of Activities | Amount($) | Basis | No. Of Activity | Cost per Unit |

| Setup Cost | 240000 | Production runs | (100+200=300) | 800 |

| Machine Cost | 1750000 | Machine Hour | 185000 | 9.46 |

| Receiving Cost | 2100000 | Receiving order | 1400 | 1500 |

| Engineering Cost | 2000000 | Engineering Hours | 10000 | 200 |

| Matetial Handling Cost | 900000 | material move | 900 | 1000 |

2.Overhead Cost Per Unit of each Product

| Cost of Activity | Part 240 | Part 390 |

| Setup Cost | 80000 | 160000 |

| Machine Cost | 1183000 | 567000 |

| Receiving Cost | 600000 | 1500000 |

| Engineering Cost | 1000000 | 1000000 |

| Material Handling Cost | 500000 | 400000 |

| Total. (A) | 3363000 | 3627000 |

| No. of Units. (B) | 500000 | 100000 |

| Overhead Per Unit (A/B) | 6.73 | 36.27 |

3.Computation of total and per unit cost of each product

| Product profit per unit | Part 240 | Part 390 |

| Selling Price per unit | $ 30 | $ 25 |

| Cost Per Unit | ||

| (i) Direct Material Per Unit | 3 | 1.5 |

| (ii) Direct labor Per Unit | 5 | 4.5 |

| (iii) Overhead Per Unit (W.No-2) | 6.73 | 36.27 |

| Total cost per Unit | 14.73 | 42.27 |

| Gross Profit per Unit | 15.27 | (17.27) |

Point No 1 Answer: The Activity based Costing is different from current product cost method.In Activity costing we allocate the overhaed cost usage of overhead cost per activity.

Point No 2 Answer : No company should not switch emphasis from part 240 to part 390 because gross profit per unit part 390 is less in comparison of gross profit per unit of part 240.

Add Answer to:

Cost Accounting

Assignment 1

Fellco Manufacturing

Fellco Manufacturing produces replacement parts for motorcycles.

They specialize in...

Product-Costing Accuracy, Corporate Strategy, ABC Autotech Manufacturing is engaged in the production of replacement parts for...

Product-Costing Accuracy, Corporate Strategy, ABC Autotech Manufacturing is engaged in the production of replacement parts for automobiles. One plant specializes in the production of two parts: Part #127 and Part #234. Part #127 produced the highest volume of activity, and for many years it was the only part produced by the plant. Five years ago, Part #234 was added. Part #234 was more difficult to manufacture and required special tooling and setups. Profits increased for the first three years after...

Scenario Cartech Manufacturing is engaged in the production of replacement parts for automobiles. One plant specializes...

Scenario

Cartech Manufacturing is engaged in the production of

replacement parts for automobiles. One plant specializes in the

production of two parts: Part 271 and Part 342. Part 271 produces

the highest volume of activity, and for many years it was the only

part produced by the plant. Five years ago, Part 342 was added.

Part 342 was more difficult to manufacture and required special

tooling and setups. Profits increased for the first three years

after the addition of the...

Scenario

Cartech Manufacturing is engaged in the production of

replacement parts for automobiles. One plant specializes in the

production of two parts: Part 271 and Part 342. Part 271 produces

the highest volume of activity, and for many years it was the only

part produced by the plant. Five years ago, Part 342 was added.

Part 342 was more difficult to manufacture and required special

tooling and setups. Profits increased for the first three years

after the addition of the...

There is no 1 or 2, only 3-5 Problem 4.34 Product-Costing Accuracy, Corporate Strategy, ABC Autotech...

There is no 1 or 2, only 3-5

Problem 4.34 Product-Costing Accuracy, Corporate Strategy, ABC Autotech Manufacturing is engaged in the production of replacement parts for automobiles. One plant specializes in the production of two parts: Part #127 and Part #234, Part #127 pro- duced the highest volume of activity, and for many years it was the only part produced by the plant. Five years ago, Part #234 was added. Part #234 was more difficult to manufacture and required special...

There is no 1 or 2, only 3-5

Problem 4.34 Product-Costing Accuracy, Corporate Strategy, ABC Autotech Manufacturing is engaged in the production of replacement parts for automobiles. One plant specializes in the production of two parts: Part #127 and Part #234, Part #127 pro- duced the highest volume of activity, and for many years it was the only part produced by the plant. Five years ago, Part #234 was added. Part #234 was more difficult to manufacture and required special...

Hello, If anyone can help me I will grestly appreciate it! I will also give a...

Hello, If anyone can help me I will grestly appreciate it! I will

also give a thumbs up!

Autotech Manufacturing is engaged in the production of replacement parts for automobiles. One plant specializes in the production of two parts: Part 127 and Part 234. Part 127 produces the highest volume of activity, and for many years it was the only part produced by the plant. Five years ago, Part 234 was added. Part 234 was more difficult to manufacture and...

Hello, If anyone can help me I will grestly appreciate it! I will

also give a thumbs up!

Autotech Manufacturing is engaged in the production of replacement parts for automobiles. One plant specializes in the production of two parts: Part 127 and Part 234. Part 127 produces the highest volume of activity, and for many years it was the only part produced by the plant. Five years ago, Part 234 was added. Part 234 was more difficult to manufacture and...

Barnes Boards produces skateboard parts for six different major US skateboard manufacturers. Barnes specializes in the...

Barnes Boards produces skateboard parts for six different major US skateboard manufacturers. Barnes specializes in the production of trucks, which attach the skateboard wheels to the skateboard deck and allow the rider to turn the skateboard. Barnes Boards' trucks are made primarily of molded aluminum. Currently, Barnes Boards produces two different types of trucks: The 700 and the 775. The 700 has the highest sales and for many years was the only truck produced by Barnes Boards. As a result of the...

Brunswick Parts is a small manufacturing firm located in eastern Canada. The company, founded in 1947,...

Brunswick Parts is a small manufacturing firm located in eastern

Canada. The company, founded in 1947, produces metal parts for many

of the larger manufacturing firms located in both Canada and the

United States. It prides itself on high quality and customer

service, and many of its customers have been buying at least some

of their parts from Brunswick since the 1950s.

Production of the parts takes place in one of two plants. The

older plant, located in Fredericton, was...

Brunswick Parts is a small manufacturing firm located in eastern

Canada. The company, founded in 1947, produces metal parts for many

of the larger manufacturing firms located in both Canada and the

United States. It prides itself on high quality and customer

service, and many of its customers have been buying at least some

of their parts from Brunswick since the 1950s.

Production of the parts takes place in one of two plants. The

older plant, located in Fredericton, was...

Brunswick Parts is a small manufacturing firm located in eastern Canada. The company, founded in 1947,...

Brunswick Parts is a small manufacturing firm located in eastern

Canada. The company, founded in 1947, produces metal parts for many

of the larger manufacturing firms located in both Canada and the

United States. It prides itself on high quality and customer

service, and many of its customers have been buying at least some

of their parts from Brunswick since the 1950s.

Production of the parts takes place in one of two plants. The

older plant, located in Fredericton, was...

Brunswick Parts is a small manufacturing firm located in eastern

Canada. The company, founded in 1947, produces metal parts for many

of the larger manufacturing firms located in both Canada and the

United States. It prides itself on high quality and customer

service, and many of its customers have been buying at least some

of their parts from Brunswick since the 1950s.

Production of the parts takes place in one of two plants. The

older plant, located in Fredericton, was...

MANAGERIAL ACCOUNTING CASE STUDY.CASE ASSIGNMENT #1: Cortland Manufacturing, Inc.

MANAGERIAL ACCOUNTING CASE STUDY.CASE ASSIGNMENT #1: Cortland Manufacturing, Inc.We constantly seem to be pricing ourselves out of some markets and not charging enough in others. Our pricing policy is pretty simple: we mark up our full manufacturing cost by 50%. That means a computer that costs us $2,000 to manufacture will sell for $3,000. Until now I thought this was a workable approach, but now I’m not so sure.Steve Works, CEO, Cortland Manufacturing, Inc. (CMI)Steve’s Controller, Sally Nomer, had just...

Brunswick Parts is a small manufacturing firm located in eastern Canada. The company, founded in 1947,...

Brunswick Parts is a small manufacturing firm located in eastern Canada. The company, founded in 1947, produces metal parts for many of the larger manufacturing firms located in both Canada and the United States. It prides itself on high quality and customer service, and many of its customers have been buying at least some of their parts from Brunswick since the 1950s. Production of the parts takes place in one of two plants. The older plant, located in Fredericton, was...

Brunswick Parts is a small manufacturing firm located in eastern Canada. The company, founded in 1947,...

Brunswick Parts is a small manufacturing firm located in eastern Canada. The company, founded in 1947, produces metal parts for many of the larger manufacturing firms located in both Canada and the United States. It prides itself on high quality and customer service, and many of its customers have been buying at least some of their parts from Brunswick since the 1950s. Production of the parts takes place in one of two plants. The older plant, located in Fredericton, was...

Scenario

Cartech Manufacturing is engaged in the production of

replacement parts for automobiles. One plant specializes in the

production of two parts: Part 271 and Part 342. Part 271 produces

the highest volume of activity, and for many years it was the only

part produced by the plant. Five years ago, Part 342 was added.

Part 342 was more difficult to manufacture and required special

tooling and setups. Profits increased for the first three years

after the addition of the...

Scenario

Cartech Manufacturing is engaged in the production of

replacement parts for automobiles. One plant specializes in the

production of two parts: Part 271 and Part 342. Part 271 produces

the highest volume of activity, and for many years it was the only

part produced by the plant. Five years ago, Part 342 was added.

Part 342 was more difficult to manufacture and required special

tooling and setups. Profits increased for the first three years

after the addition of the...

There is no 1 or 2, only 3-5

Problem 4.34 Product-Costing Accuracy, Corporate Strategy, ABC Autotech Manufacturing is engaged in the production of replacement parts for automobiles. One plant specializes in the production of two parts: Part #127 and Part #234, Part #127 pro- duced the highest volume of activity, and for many years it was the only part produced by the plant. Five years ago, Part #234 was added. Part #234 was more difficult to manufacture and required special...

There is no 1 or 2, only 3-5

Problem 4.34 Product-Costing Accuracy, Corporate Strategy, ABC Autotech Manufacturing is engaged in the production of replacement parts for automobiles. One plant specializes in the production of two parts: Part #127 and Part #234, Part #127 pro- duced the highest volume of activity, and for many years it was the only part produced by the plant. Five years ago, Part #234 was added. Part #234 was more difficult to manufacture and required special...

Hello, If anyone can help me I will grestly appreciate it! I will

also give a thumbs up!

Autotech Manufacturing is engaged in the production of replacement parts for automobiles. One plant specializes in the production of two parts: Part 127 and Part 234. Part 127 produces the highest volume of activity, and for many years it was the only part produced by the plant. Five years ago, Part 234 was added. Part 234 was more difficult to manufacture and...

Hello, If anyone can help me I will grestly appreciate it! I will

also give a thumbs up!

Autotech Manufacturing is engaged in the production of replacement parts for automobiles. One plant specializes in the production of two parts: Part 127 and Part 234. Part 127 produces the highest volume of activity, and for many years it was the only part produced by the plant. Five years ago, Part 234 was added. Part 234 was more difficult to manufacture and...

Brunswick Parts is a small manufacturing firm located in eastern

Canada. The company, founded in 1947, produces metal parts for many

of the larger manufacturing firms located in both Canada and the

United States. It prides itself on high quality and customer

service, and many of its customers have been buying at least some

of their parts from Brunswick since the 1950s.

Production of the parts takes place in one of two plants. The

older plant, located in Fredericton, was...

Brunswick Parts is a small manufacturing firm located in eastern

Canada. The company, founded in 1947, produces metal parts for many

of the larger manufacturing firms located in both Canada and the

United States. It prides itself on high quality and customer

service, and many of its customers have been buying at least some

of their parts from Brunswick since the 1950s.

Production of the parts takes place in one of two plants. The

older plant, located in Fredericton, was...

Brunswick Parts is a small manufacturing firm located in eastern

Canada. The company, founded in 1947, produces metal parts for many

of the larger manufacturing firms located in both Canada and the

United States. It prides itself on high quality and customer

service, and many of its customers have been buying at least some

of their parts from Brunswick since the 1950s.

Production of the parts takes place in one of two plants. The

older plant, located in Fredericton, was...

Brunswick Parts is a small manufacturing firm located in eastern

Canada. The company, founded in 1947, produces metal parts for many

of the larger manufacturing firms located in both Canada and the

United States. It prides itself on high quality and customer

service, and many of its customers have been buying at least some

of their parts from Brunswick since the 1950s.

Production of the parts takes place in one of two plants. The

older plant, located in Fredericton, was...

Most questions answered within 3 hours.

-

What mass of ethylene glycol (C2H6O2) must be added to 211.0 g

of water to obtain...

asked 32 seconds from now -

Mary's employer has a defined benefits retirement plan, which

pay 3.2% of her last year's salary...

asked 2 minutes ago -

What are the characteristics and behavior of an ethical

manager?

Explain, in your words, what ethics...

asked 19 minutes ago -

1. Which of the following is NOT an argument that McMahan uses

to show that jus...

asked 40 minutes ago -

A crate slides up a frictionless slope. At the end of 3 seconds

its velocity is...

asked 57 minutes ago -

Use the following information to answer the next seven

questions.

Suppose there are three potential states...

asked 53 minutes ago -

If we only have interstitial and substitutional diffusion, then

what do we consider the process of...

asked 1 hour ago -

You look at yourself in a shiny 9.6-cm-diameter Christmas tree

ball.

If your face is 21.0...

asked 1 hour ago -

If we were to measure the relaxation time of a muscle after

undergoing tetanus compared to...

asked 1 hour ago -

4CO(g) + 8H2(g) -----> 3CH4(g) +

CO2(g) + 2H2O(l)

Use the following data as needed to...

asked 1 hour ago -

without using map

1. Write a C++ program to find out the top 10 words in...

asked 1 hour ago -

1)Calculate the percent ionization of a

0.330 M solution of hypochlorous

acid.

% Ionization = %...

asked 1 hour ago