Homework Answers

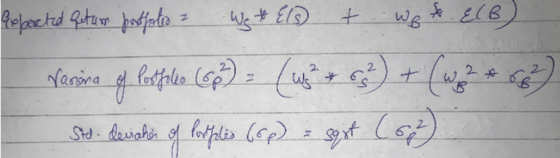

Given:

Expected return(Bonds), E(B) = 6%

Expected return(Stocks), E(S) = 15%

Standard deviation of bonds, (B) = 29%

Standard deviation of stocks, (S) = 35%

, Correlation =

0.0517

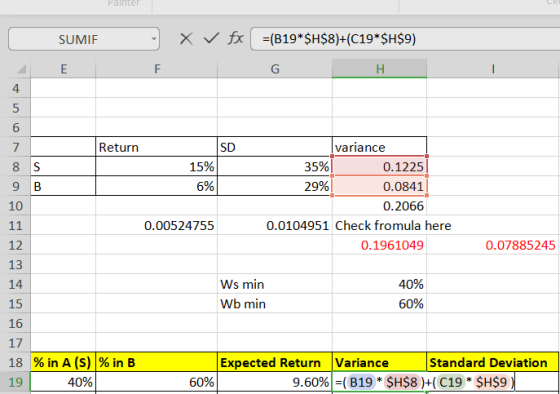

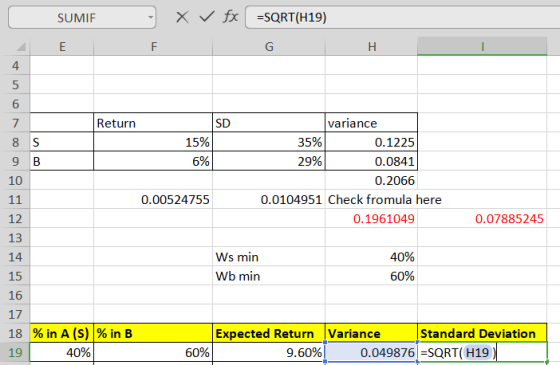

| Return | SD | variance | |

| S | 15% | 35% | 0.1225 |

| B | 6% | 29% | 0.0841 |

Min Risk Portfolio is given by:

also, Cov (B,S) = *

(S)

*

(B)

Putting in values,

Wmin(S) = [ (0.29)^2 - ( 0.0517 * 0.29 * 0.35) ] / [ (0.12)^2 + (0.08)^2 - 2 * ( 0.0517 * 0.29 * 0.35) ]

Wmin(S) = 0.07885245 / 0.1961049

Wmin(S) = 40%

Hence

Wmin(B) = 60%

Formula to be used

Add Answer to:

Check my work A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Standard Deviation Stock fund (5) Bond fund (B) Expected Return 15% 9% The correlation between the fund returns is 15. What is the expected return and standard deviation for the minimum...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Standard Deviation Stock fund (5) Bond fund (B) Expected Return 15% 9% The correlation between the fund returns is 15. What is the expected return and standard deviation for the minimum...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Stock fund (S) Bond fund (B) Expected Return 15% 9% Standard Deviation 32% 23% The correlation between the fund returns is .15. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Stock fund (S) Bond fund (B) Expected Return 15% 9% Standard Deviation 32% 23% The correlation between the fund returns is .15. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 47%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund 373 (5) Bond fund (8) 31% The correlation between the fund returns is 0.1065. What is the expected return and standard deviation for the minimum...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 47%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund 373 (5) Bond fund (8) 31% The correlation between the fund returns is 0.1065. What is the expected return and standard deviation for the minimum...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.2%. The probability distributions of the risky funds are: Expected Return 13% 6% Standard Deviation 42% 36% Stock fund (S) Bond fund (B) The correlation between the fund returns is .0222. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.2%. The probability distributions of the risky funds are: Expected Return 13% 6% Standard Deviation 42% 36% Stock fund (S) Bond fund (B) The correlation between the fund returns is .0222. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.6%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund (S) 17% 46% Bond fund (B) 8% 40% The correlation between the fund returns is 0.0600. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.7%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund (S) 17% 37% Bond fund (B) 8% 31% The correlation between the fund returns is 0.1065. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.4%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund (S) 14% 34% Bond fund (B) 5% 28% The correlation between the fund returns is 0.0214. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 3.0%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund (S) 12% 41% Bond fund (B) 5% 30% The correlation between the fund returns is 0.0667. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.4%. The probability distributions of the risky funds are: Expected Return Std. Deviation Stock fund (S) 15% 44% Bond fund (B) 8% 38% The correlation between the fund returns is .0684. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.4%. The probability distributions of the risky funds are: Standard Deviation Expected Return 14% - 5% Stock fund (S) Bond fund (B) 34% 28% The correlation between the fund returns is 0.0214. What is the expected return and standard deviation...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.4%. The probability distributions of the risky funds are: Standard Deviation Expected Return 14% - 5% Stock fund (S) Bond fund (B) 34% 28% The correlation between the fund returns is 0.0214. What is the expected return and standard deviation...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Standard Deviation Stock fund (5) Bond fund (B) Expected Return 15% 9% The correlation between the fund returns is 15. What is the expected return and standard deviation for the minimum...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Standard Deviation Stock fund (5) Bond fund (B) Expected Return 15% 9% The correlation between the fund returns is 15. What is the expected return and standard deviation for the minimum...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Stock fund (S) Bond fund (B) Expected Return 15% 9% Standard Deviation 32% 23% The correlation between the fund returns is .15. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Stock fund (S) Bond fund (B) Expected Return 15% 9% Standard Deviation 32% 23% The correlation between the fund returns is .15. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 47%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund 373 (5) Bond fund (8) 31% The correlation between the fund returns is 0.1065. What is the expected return and standard deviation for the minimum...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 47%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund 373 (5) Bond fund (8) 31% The correlation between the fund returns is 0.1065. What is the expected return and standard deviation for the minimum...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.2%. The probability distributions of the risky funds are: Expected Return 13% 6% Standard Deviation 42% 36% Stock fund (S) Bond fund (B) The correlation between the fund returns is .0222. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.2%. The probability distributions of the risky funds are: Expected Return 13% 6% Standard Deviation 42% 36% Stock fund (S) Bond fund (B) The correlation between the fund returns is .0222. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.4%. The probability distributions of the risky funds are: Standard Deviation Expected Return 14% - 5% Stock fund (S) Bond fund (B) 34% 28% The correlation between the fund returns is 0.0214. What is the expected return and standard deviation...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.4%. The probability distributions of the risky funds are: Standard Deviation Expected Return 14% - 5% Stock fund (S) Bond fund (B) 34% 28% The correlation between the fund returns is 0.0214. What is the expected return and standard deviation...

Most questions answered within 3 hours.

-

How is an organization's culture learned? How are the

mores and folkways of the organization passed...

asked 5 minutes ago -

If someone could solve this and explain how they did so that

would be great.

I...

asked 5 minutes ago -

What would be the formal charge on the nitrogen atom in a

compound that had a...

asked 6 minutes ago -

Please, i need Unique answer, Use your own words (don't copy and

paste). *Please, don't use...

asked 7 minutes ago -

Two wave pulses travel on a string toward each other. The wave

pulses can be described...

asked 23 minutes ago -

1.A solution has a pH of 5.5. What would be the color of the

solution if...

asked 37 minutes ago -

Over time, hydrogen peroxide, H2O2,

degrades into water and oxygen gas. A bottle of hydrogen

peroxide is...

asked 31 minutes ago -

2. Consider the following data table for a hypothetical

economy.

Aggregate

Consumption

Personal

&n

asked 36 minutes ago -

Adidas Runs Into Supply-Chain Problems in Crucial North

American Market

Shares fall amid concern the sporting-goods...

asked 37 minutes ago -

The physical plant at the main campus of a large state

university recieves daily requests to...

asked 1 hour ago -

Determine the probability p(2) for a binomial

experiment with n=12 trials and the success probability

p=0.1....

asked 48 minutes ago -

What is the vapor pressure at 20 degrees C of an ideal solution

prepared by the...

asked 46 minutes ago