Describe the basic steps in calculating estimates of the parameters of a multiplicative seasonal ...

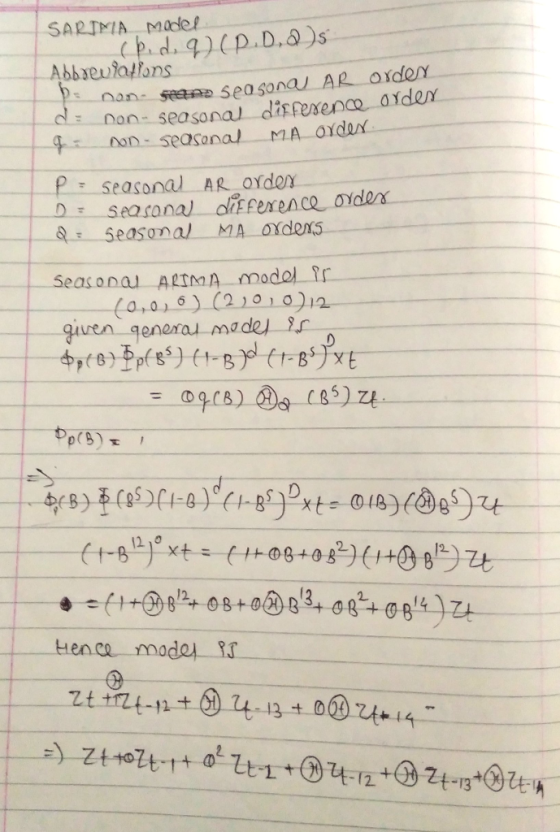

Describe the basic steps in calculating estimates of the parameters of a multiplicative seasonal ARIMA(0 , 0 , 0)(2 0, 0)12model. (write down the model, explain the terms in the model and write down the equations to estimate the parameters in terms of sample moments)

Homework Answers

Add Answer to:

Describe the basic steps in calculating estimates of the parameters of a multiplicative seasonal ...

explain how you would solve a typical equilibrium problem. List the steps, and describe the equations/mathematics...

explain how you would solve a typical equilibrium problem. List the steps, and describe the equations/mathematics you would use, but do not actually write down the equations.

Let X have a Weibull distribution with parameters a and B, So Е(X) 3 В ....

Let X have a Weibull distribution with parameters a and B, So Е(X) 3 В . Г(1 VX) %3D в2{г(1 1/a) + [r(1/a)2 2/a) (a) Based on a random sample X1, . . . , Xn, write equations for the method of moments estimators of B and a. Show that, once the estimate of a has been obtained, the estimate of B can be found from a table of the gamma function and that the estimate of a is the...

Let X have a Weibull distribution with parameters a and B, So Е(X) 3 В . Г(1 VX) %3D в2{г(1 1/a) + [r(1/a)2 2/a) (a) Based on a random sample X1, . . . , Xn, write equations for the method of moments estimators of B and a. Show that, once the estimate of a has been obtained, the estimate of B can be found from a table of the gamma function and that the estimate of a is the...

Problem 2: Valuation on a Multiplicative Binomial Lattice This problem reviews some of the main i...

Problem 2: Valuation on a Multiplicative Binomial Lattice This problem reviews some of the main ideas of valuation on a binomial lattice and the properties of put and call options. You may wish to review the relevant lecture material and readings. Suppose that the price of a share of KAF stock is S(0) = £120 in period 0. At the beginning of period 1, the price of a share can either move upward to S(1) = u S(0) or downward...

QUESTION 2 (a) For each of the ARIMA models below, give the values for E(VY) and...

QUESTION 2 (a) For each of the ARIMA models below, give the values for E(VY) and Var(VY) 0.Tet-1 (ii) Yt = 10 + 1.25%-1-0.25Yt-2 et-0.14-i (b) Show that the function Z, a t-1 not stationary, but the first difference of Z, is stationary QUESTION 5 (a) From a series Y, of length 100, the sample autocorrelations at lags 1-3 are 0.8, 0.5 and 0.4, respectively. Furthermore, the respective sample mean and sample variance of the series are 2 and s-5....

QUESTION 2 (a) For each of the ARIMA models below, give the values for E(VY) and Var(VY) 0.Tet-1 (ii) Yt = 10 + 1.25%-1-0.25Yt-2 et-0.14-i (b) Show that the function Z, a t-1 not stationary, but the first difference of Z, is stationary QUESTION 5 (a) From a series Y, of length 100, the sample autocorrelations at lags 1-3 are 0.8, 0.5 and 0.4, respectively. Furthermore, the respective sample mean and sample variance of the series are 2 and s-5....

Two-step model of constitutive unregulated gene expression. a) Write down the corresponding system of coupled ordinary...

Two-step model of constitutive unregulated gene expression.

a) Write down the corresponding system of coupled ordinary

differential equations (ODEs) based on mass action kinetics.

Identify and explain which biological/biochemical process the

“source” and “sink” terms in each equation describe.

b) State the parameters for steady-state mRNA and protein

levels.

OM promoter (A) mRNA (M) protein (P) Figure 1. Two-step model of constitutive (unregulated) gene expression. Here the promoter (A) is a constant and represents a gene.

Two-step model of constitutive unregulated gene expression.

a) Write down the corresponding system of coupled ordinary

differential equations (ODEs) based on mass action kinetics.

Identify and explain which biological/biochemical process the

“source” and “sink” terms in each equation describe.

b) State the parameters for steady-state mRNA and protein

levels.

OM promoter (A) mRNA (M) protein (P) Figure 1. Two-step model of constitutive (unregulated) gene expression. Here the promoter (A) is a constant and represents a gene.

Neglect body effect in the calculation for this problem. The device/circuit parameters are Part (a) and (b) refer to th...

Neglect body effect in the calculation for this problem. The device/circuit parameters are Part (a) and (b) refer to the following equalizer circuit: VE СВ св 2.5V (a)If VB 0-VB 0) = 0 capacitor initially uncharged Find the steady state values for VB and VB for the clock signal ф t as shown below. (10 pts) 6 c 4 E 2E 10 4 t (ns) (b) Estimate the 'rise time' for VB(t) to reach the steady-state values you have calculated...

Neglect body effect in the calculation for this problem. The device/circuit parameters are Part (a) and (b) refer to the following equalizer circuit: VE СВ св 2.5V (a)If VB 0-VB 0) = 0 capacitor initially uncharged Find the steady state values for VB and VB for the clock signal ф t as shown below. (10 pts) 6 c 4 E 2E 10 4 t (ns) (b) Estimate the 'rise time' for VB(t) to reach the steady-state values you have calculated...

1) 2) A structural model is given as: yixB, i = 1,.. , n. Assume availability...

1)

2)

A structural model is given as: yixB, i = 1,.. , n. Assume availability of a set of instruments, zi, of the same dimension as the number of regres- sors Under which conditions is the set of instruments valid and relevant? Explain Write down the two sets of GMM moments conditions needed to estimate B under the assumption E[x;e4] 0 and Eziei 0 respectively

1)

2)

A structural model is given as: yixB, i = 1,.. , n. Assume availability of a set of instruments, zi, of the same dimension as the number of regres- sors Under which conditions is the set of instruments valid and relevant? Explain Write down the two sets of GMM moments conditions needed to estimate B under the assumption E[x;e4] 0 and Eziei 0 respectively

please write all steps and calculations neatly to help with my understanding. when calculating the ratio...

please write all steps and calculations neatly to help

with my understanding. when calculating the ratio please explain

how to do so

here's how they solve it but I don't understand the

ratio portion

19. Describe how to prepare a buffer solution from NaH2PO4 and Na2HPO4 to have a pH of 7.5. Chapter 17, Problem 19PS [] Bookmark ام Show all steps: Step 1 of 2 A 389-18-17Pc K = 6.2 x 10 pK =7.2 Since pH = pK, +log:...

please write all steps and calculations neatly to help

with my understanding. when calculating the ratio please explain

how to do so

here's how they solve it but I don't understand the

ratio portion

19. Describe how to prepare a buffer solution from NaH2PO4 and Na2HPO4 to have a pH of 7.5. Chapter 17, Problem 19PS [] Bookmark ام Show all steps: Step 1 of 2 A 389-18-17Pc K = 6.2 x 10 pK =7.2 Since pH = pK, +log:...

I only need Question 4 (Image above) answered. I am providing you with the rest of the questions and other information...

I only need Question 4 (Image above) answered. I am

providing you with the rest of the questions and other information

for background information since it is necessary to answer Question

4. I do not need answers to Q1, 2 and 3 - only for Q4

Background information for the question:

The dataset weightloss.dta contains information on 77 patients

randomised to undertake one of three diets (referred to as diet A,

B and C). Some background information is also available,...

I only need Question 4 (Image above) answered. I am

providing you with the rest of the questions and other information

for background information since it is necessary to answer Question

4. I do not need answers to Q1, 2 and 3 - only for Q4

Background information for the question:

The dataset weightloss.dta contains information on 77 patients

randomised to undertake one of three diets (referred to as diet A,

B and C). Some background information is also available,...

(a) Write down the population regression model, being as specific as possible. (5 points) (b) What...

(a) Write down the population regression model, being as

specific as possible. (5 points)

(b) What is the meaning of the error term u in this regression?

Provide an example of what u represents. (5 points)

(c) What are the estimates of the intercept and slope

parameters? Interpret what these estimates mean, being as specific

as possible. (15 points)

(d) Why might the estimate of the slope from the simple linear

regression above be a biased estimate of the true...

(a) Write down the population regression model, being as

specific as possible. (5 points)

(b) What is the meaning of the error term u in this regression?

Provide an example of what u represents. (5 points)

(c) What are the estimates of the intercept and slope

parameters? Interpret what these estimates mean, being as specific

as possible. (15 points)

(d) Why might the estimate of the slope from the simple linear

regression above be a biased estimate of the true...

Let X have a Weibull distribution with parameters a and B, So Е(X) 3 В . Г(1 VX) %3D в2{г(1 1/a) + [r(1/a)2 2/a) (a) Based on a random sample X1, . . . , Xn, write equations for the method of moments estimators of B and a. Show that, once the estimate of a has been obtained, the estimate of B can be found from a table of the gamma function and that the estimate of a is the...

Let X have a Weibull distribution with parameters a and B, So Е(X) 3 В . Г(1 VX) %3D в2{г(1 1/a) + [r(1/a)2 2/a) (a) Based on a random sample X1, . . . , Xn, write equations for the method of moments estimators of B and a. Show that, once the estimate of a has been obtained, the estimate of B can be found from a table of the gamma function and that the estimate of a is the...

QUESTION 2 (a) For each of the ARIMA models below, give the values for E(VY) and Var(VY) 0.Tet-1 (ii) Yt = 10 + 1.25%-1-0.25Yt-2 et-0.14-i (b) Show that the function Z, a t-1 not stationary, but the first difference of Z, is stationary QUESTION 5 (a) From a series Y, of length 100, the sample autocorrelations at lags 1-3 are 0.8, 0.5 and 0.4, respectively. Furthermore, the respective sample mean and sample variance of the series are 2 and s-5....

QUESTION 2 (a) For each of the ARIMA models below, give the values for E(VY) and Var(VY) 0.Tet-1 (ii) Yt = 10 + 1.25%-1-0.25Yt-2 et-0.14-i (b) Show that the function Z, a t-1 not stationary, but the first difference of Z, is stationary QUESTION 5 (a) From a series Y, of length 100, the sample autocorrelations at lags 1-3 are 0.8, 0.5 and 0.4, respectively. Furthermore, the respective sample mean and sample variance of the series are 2 and s-5....

Two-step model of constitutive unregulated gene expression.

a) Write down the corresponding system of coupled ordinary

differential equations (ODEs) based on mass action kinetics.

Identify and explain which biological/biochemical process the

“source” and “sink” terms in each equation describe.

b) State the parameters for steady-state mRNA and protein

levels.

OM promoter (A) mRNA (M) protein (P) Figure 1. Two-step model of constitutive (unregulated) gene expression. Here the promoter (A) is a constant and represents a gene.

Two-step model of constitutive unregulated gene expression.

a) Write down the corresponding system of coupled ordinary

differential equations (ODEs) based on mass action kinetics.

Identify and explain which biological/biochemical process the

“source” and “sink” terms in each equation describe.

b) State the parameters for steady-state mRNA and protein

levels.

OM promoter (A) mRNA (M) protein (P) Figure 1. Two-step model of constitutive (unregulated) gene expression. Here the promoter (A) is a constant and represents a gene.

Neglect body effect in the calculation for this problem. The device/circuit parameters are Part (a) and (b) refer to the following equalizer circuit: VE СВ св 2.5V (a)If VB 0-VB 0) = 0 capacitor initially uncharged Find the steady state values for VB and VB for the clock signal ф t as shown below. (10 pts) 6 c 4 E 2E 10 4 t (ns) (b) Estimate the 'rise time' for VB(t) to reach the steady-state values you have calculated...

Neglect body effect in the calculation for this problem. The device/circuit parameters are Part (a) and (b) refer to the following equalizer circuit: VE СВ св 2.5V (a)If VB 0-VB 0) = 0 capacitor initially uncharged Find the steady state values for VB and VB for the clock signal ф t as shown below. (10 pts) 6 c 4 E 2E 10 4 t (ns) (b) Estimate the 'rise time' for VB(t) to reach the steady-state values you have calculated...

1)

2)

A structural model is given as: yixB, i = 1,.. , n. Assume availability of a set of instruments, zi, of the same dimension as the number of regres- sors Under which conditions is the set of instruments valid and relevant? Explain Write down the two sets of GMM moments conditions needed to estimate B under the assumption E[x;e4] 0 and Eziei 0 respectively

1)

2)

A structural model is given as: yixB, i = 1,.. , n. Assume availability of a set of instruments, zi, of the same dimension as the number of regres- sors Under which conditions is the set of instruments valid and relevant? Explain Write down the two sets of GMM moments conditions needed to estimate B under the assumption E[x;e4] 0 and Eziei 0 respectively

please write all steps and calculations neatly to help

with my understanding. when calculating the ratio please explain

how to do so

here's how they solve it but I don't understand the

ratio portion

19. Describe how to prepare a buffer solution from NaH2PO4 and Na2HPO4 to have a pH of 7.5. Chapter 17, Problem 19PS [] Bookmark ام Show all steps: Step 1 of 2 A 389-18-17Pc K = 6.2 x 10 pK =7.2 Since pH = pK, +log:...

please write all steps and calculations neatly to help

with my understanding. when calculating the ratio please explain

how to do so

here's how they solve it but I don't understand the

ratio portion

19. Describe how to prepare a buffer solution from NaH2PO4 and Na2HPO4 to have a pH of 7.5. Chapter 17, Problem 19PS [] Bookmark ام Show all steps: Step 1 of 2 A 389-18-17Pc K = 6.2 x 10 pK =7.2 Since pH = pK, +log:...

I only need Question 4 (Image above) answered. I am

providing you with the rest of the questions and other information

for background information since it is necessary to answer Question

4. I do not need answers to Q1, 2 and 3 - only for Q4

Background information for the question:

The dataset weightloss.dta contains information on 77 patients

randomised to undertake one of three diets (referred to as diet A,

B and C). Some background information is also available,...

I only need Question 4 (Image above) answered. I am

providing you with the rest of the questions and other information

for background information since it is necessary to answer Question

4. I do not need answers to Q1, 2 and 3 - only for Q4

Background information for the question:

The dataset weightloss.dta contains information on 77 patients

randomised to undertake one of three diets (referred to as diet A,

B and C). Some background information is also available,...

(a) Write down the population regression model, being as

specific as possible. (5 points)

(b) What is the meaning of the error term u in this regression?

Provide an example of what u represents. (5 points)

(c) What are the estimates of the intercept and slope

parameters? Interpret what these estimates mean, being as specific

as possible. (15 points)

(d) Why might the estimate of the slope from the simple linear

regression above be a biased estimate of the true...

(a) Write down the population regression model, being as

specific as possible. (5 points)

(b) What is the meaning of the error term u in this regression?

Provide an example of what u represents. (5 points)

(c) What are the estimates of the intercept and slope

parameters? Interpret what these estimates mean, being as specific

as possible. (15 points)

(d) Why might the estimate of the slope from the simple linear

regression above be a biased estimate of the true...

Most questions answered within 3 hours.

-

List the six general types of information management systems,

and give one logistics application to each...

asked 14 seconds from now -

XYZ corporation uses statistical quality control to monitor the

quality of their product. They have determined...

asked 3 minutes ago -

If a liquid

contains 60% sugar and 40% water through out its composition then

what is...

asked 11 minutes ago -

In testing a new drug, researchers found that 5% of all patients

using it will have...

asked 8 minutes ago -

The data in set A represents prices (with tax included) of a

large cup of regular...

asked 20 minutes ago -

How do neuropsychological assessments provide information about

impairment? How could this information be misused?

asked 13 minutes ago -

Define SNP and elaborate various type of SNPs and their

importance in pharmacogenetics?

asked 17 minutes ago -

Description

There are 4 classes, Figure is the base class,both Triangle,

Rectangle and Circle are all...

asked 18 minutes ago -

What will the standard deviation of these exam grades be? A

square bracket means inclusive, so...

asked 27 minutes ago -

Beginning Retained Earnings are $ 79 comma 000 $79,000; sales

are $ 31 comma 700 $31,700;...

asked 30 minutes ago -

Please explain/demonstrate how to use NLTK to test unigram,

bigram, and trigram character models on guessing...

asked 36 minutes ago -

what you feel is most important to you and why regarding your

typing skills?

asked 37 minutes ago